Tag: Retirement Planning

Top 3 Vital Documents Every Senior Needs to Organize Today

April 1, 2026

Every single year, thousands of older homeowners throw away hundreds, even thousands, of dollars. Why? They simply didn’t file the right piece of paper. Meanwhile, families are out there making agonizing medical choices in crowded hospital hallways because nobody knows where mom or dad put their living will. And don’t even get started on Medicare benefits lost to the void of a messy filing cabinet.

These aren’t freak accidents. This stuff happens constantly to otherwise prepared families who just didn’t get their paperwork sorted in time.

If you’re a senior, or helping one manage their affairs, three specific types of documents need your attention right now: property tax exemptions, Medicare files, and advance directives. Getting a handle on these and actually keeping them where people can find them protects your money, honors your medical choices, and cuts out the panic when things go sideways.

Why Property Tax Exemption Documents Are More Important Than Ever

Sure, most older homeowners know property tax breaks exist. But hardly anyone realizes exactly how much cash they’re leaving on the table by not claiming them or by forgetting to renew them.

Fast forward to 2026, and a bunch of states have seriously beefed up their senior tax relief. Take New York: qualifying homeowners 65 and up can now shield up to 65% of their home’s assessed value from taxes (up from the old 50% cap). In New Jersey, the Stay NJ program is knocking up to $6,500 a year off tax bills for households making under $500,000. Over in Texas, they’ve expanded the over-65 school district exemption so much that plenty of folks aren’t paying school taxes at all anymore.

Here’s the catch, though. They don’t just hand this money to you automatically. In Texas alone, roughly 15% of eligible folks never file for their homestead exemption. That’s about $1,500 a year just evaporating. You see the same thing happening nationwide.

And then there’s the renewal trap. A lot of these tax breaks force you to refile every single year. Miss a random deadline in March or April? You lose the discount for the whole year. If your proof of age, income, and residency isn’t sitting somewhere obvious, blowing past that deadline is incredibly easy.

Here is what you actually need to keep handy:

- Proof of age (like a birth certificate or government ID)

- Proof you actually live there (mortgage statements, recent utility bills)

- Your latest income info (Social Security award letters, tax returns)

- The actual exemption application and those annoying annual renewal notices

- Any random letters the county assessor mails you

When you finally get this stuff organized ideally in a secure digital spot that your kids or trusted contacts can reach claiming your tax break turns into a quick annual chore instead of a frantic scavenger hunt.

The Medicare Documents That Too Many Families Cannot Find

Medicare is arguably the most crucial benefit you’ll ever get. Yet, the paperwork usually ends up shoved in a jammed desk drawer nobody else can open. Or worse, sitting in a messy pile on the kitchen counter.

For seniors and the people taking care of them, there’s a core stack of Medicare records you absolutely must keep safe and share with at least one person you trust.

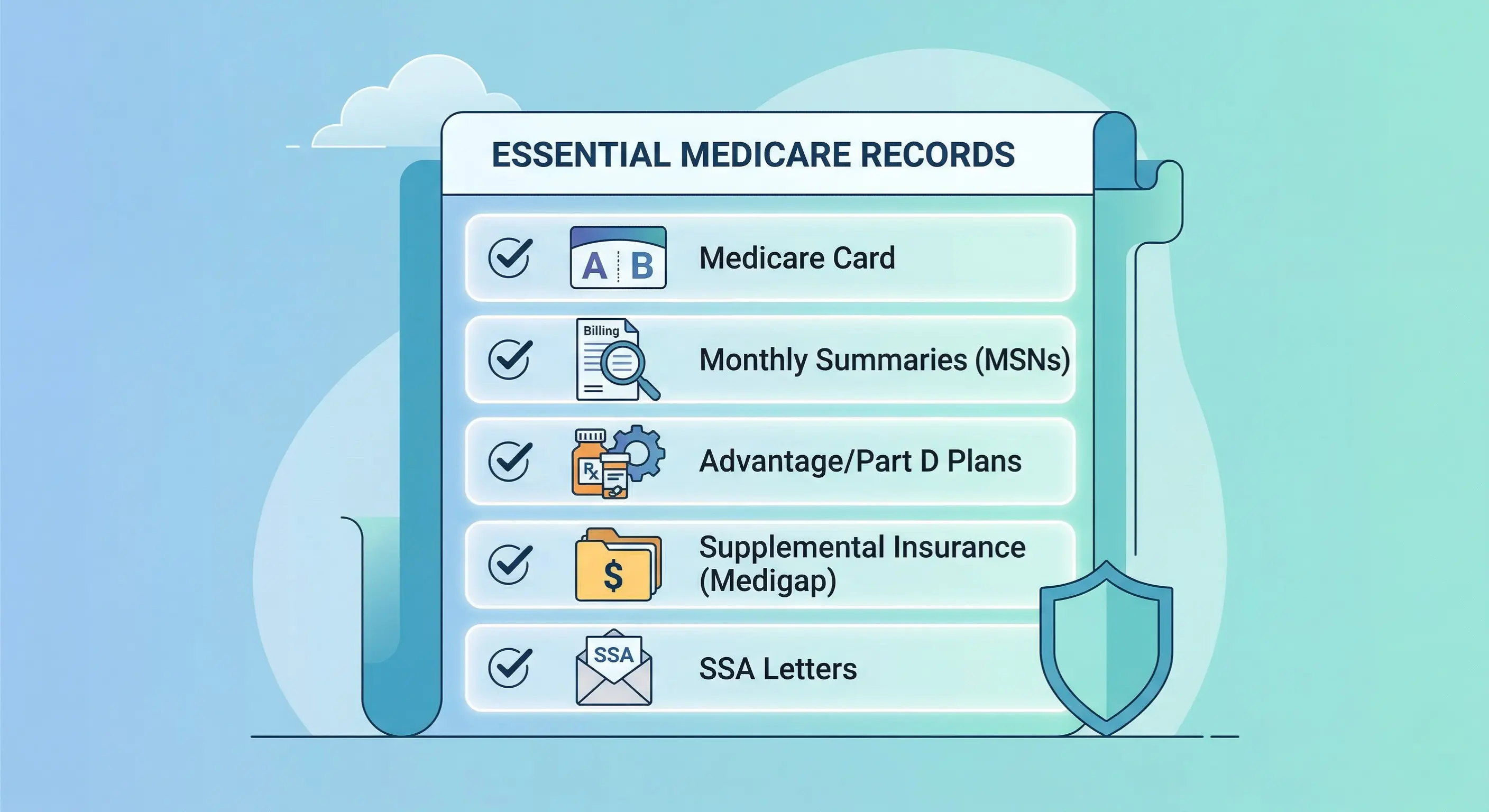

Keep these essential Medicare records organized:

- Your actual Medicare card (Part A and Part B)

- Medicare Summary Notices (MSNs) these are the monthly statements showing what they billed and what Medicare actually covered

- Enrollment docs for your Medicare Advantage or Part D plan

- Explanation of Benefits (EOB) from any Medigap or supplemental policies

- Letters from Social Security about your eligibility or premiums

- Paperwork for the Medicare Savings Program, if you use it

- Any records of fights or appeals with Medicare

Look, this isn’t just busywork. These papers prove you have coverage during an emergency. They help you spot billing fraud. They are totally necessary when you’re trying to coordinate care between three different doctors. If you end up in the hospital and your daughter needs to argue with the billing department, handing her these records will save her hours on hold and prevent massive bills.

Also, remember that Medicare Part B pays for a voluntary chat with your doctor about advance care planning. If you do this during your annual wellness visit, it shouldn’t cost you a dime out of pocket. Keep the notes from that conversation on file, too.

Living Wills and Advance Directives: The Documents That Speak When a Senior Cannot

Out of everything you could possibly organize, the living will is probably the most personal. It’s also the one document guaranteed to go missing right when everyone desperately needs it.

The University of Michigan’s National Poll on Healthy Aging found something pretty alarming: 54% of adults between 50 and 80 haven’t bothered with an advance directive or living will. So what happens? A medical crisis hits, and total strangers (doctors who just met the patient) or terrified family members have to make gut-wrenching decisions under crazy pressure.

A living will is just a legal paper that outlines what medical treatments you want if you can’t speak for yourself. A healthcare proxy (sometimes called a durable power of attorney for healthcare) officially names the person you trust to make those choices for you. The living will itself gets into the weeds about things like dialysis, ventilators, resuscitation, and feeding tubes.

And please don’t think this is only for the very old or the terminally ill. Car accidents and strokes don’t check your calendar. It is so much better to write a living will at 65 while you’re healthy than to try scraping one together at 85 in the ICU.

Make sure you store and share these key advance directive documents:

- The living will itself

- Durable power of attorney for healthcare

- Your POLST or MOLST form (Physician Orders for Life-Sustaining Treatment), if you have one

- The actual healthcare proxy paperwork

- Your written wishes regarding organ donation

- Copies of all this given to your primary doctor and any major specialists

Quick tip: if you’re a snowbird splitting time between two states, do yourself a favor and create an advance directive for both. Keep copies of both documents together in both houses.

The Common Thread: These Documents Are Useless If No One Can Find Them

A tax exemption that lapsed. A Medicare card buried in a shoebox under the bed. A living will locked tight in a safe that only grandpa knew the combination to. This exact nightmare plays out in living rooms across the country every single day.

The real goal here isn’t just printing out forms. It’s about locking them down somewhere secure, actually keeping them up to date, and making sure your trusted point person knows exactly where to look when the time comes.

That is exactly why platforms like InsureYouKnow.org exist. It’s a secure, encrypted digital safe deposit box. You can stash your vital records there, give access to the people you trust, and even set up nudges to review everything once in a while. Nobody wants to do paperwork just for fun. You do it for the peace of mind.

You do it so that when life throws a curveball, the right papers are in the right hands immediately.

Seniors and their families already have enough stress to deal with. Getting your records straight today basically guarantees you one less crisis tomorrow.

InsureYouKnow.org is a secure electronic safe deposit box for life’s most important information. The platform does not provide legal, financial, or insurance advice it helps ensure that the right people have access to the right documents when they need them most.

Updating Insurance and Documents During Major Life Changes

October 30, 2025

Life Keeps Moving

A new job, a move overseas, or the day someone finally retires all sound exciting. In the middle of packing boxes or filling out onboarding forms, it’s easy to forget the quieter side of change: the policies, records, and bits of paperwork that keep daily life running smoothly.

Missing an update here can cause small but annoying problems later. A wrong address on an insurance file, an expired policy, or a forgotten beneficiary can slow down a claim when it’s really needed

When Work Life Shifts

A new role often means new benefits, different coverage, and sometimes a short gap between plans. People tend to assume everything carries over automatically, but that’s rarely the case.

- Before leaving a company, check the exact date the old health plan ends.

- Ask the new employer when coverage begins; if there’s a gap, arrange a temporary plan.

- Look at personal policies to be sure the coverage amount still fits current income and family needs.

- Update names, addresses, and phone numbers across all accounts.

- Keep the older paperwork since it’s proof if a claim from that period ever comes up.

It’s a small chore during a busy week, but it prevents confusion later.

When a Move Crosses Borders

Relocating brings excitement, but every country plays by its own rules when it comes to insurance and legal documents. A policy that worked perfectly at home might be useless once abroad.

Before boarding the plane:

- Ask the insurer about international coverage and buy a global or expat plan if necessary.

- Re-draft wills or powers of attorney so they follow local laws.

- Tell banks and pension providers the new address since some freeze accounts if mail bounces back.

- Store digital copies of important papers in a secure online vault and let one trusted person know how to reach them in an emergency.

It takes a few emails and signatures, but it can save a lot of time and stress once the move is complete.

When Retirement Begins

Retirement changes how income and coverage work. Employer insurance usually ends, and new health options need to be arranged.

- Compare health plans designed for retirees or seniors.

- Review life insurance since sometimes a smaller policy makes more sense now.

- Gather pension statements and investment reports in one folder.

- Make sure wills and executors’ details are up to date.

- Keep digital and printed copies in one clearly labeled place.

A tidy file today makes life much easier tomorrow for both the retiree and their family.

Quick Review Checklist

A few questions worth asking after any big change:

- Does current insurance still cover what’s needed?

- Are beneficiaries correct and easy to contact?

- Are legal and financial papers current?

- Is everything backed up securely?

- Has someone trustworthy been told how to access it?

If each answer is yes, everything is already in good shape.

Keeping It All Together

Loose papers and forgotten folders can turn into a real headache. A secure digital vault, such as InsureYouKnow, keeps all records in one encrypted space that can be opened from anywhere. It’s simple, private, and designed for moments exactly like these: job changes, relocations, and retirements.

Final Thoughts

Big life transitions come with excitement and responsibility. Updating insurance and personal documents may not feel urgent, but it protects the plans built over years of effort. With organized records and the right digital tools, the next chapter, wherever it leads, starts off clear and worry-free.

ACA Marketplace: Understanding the Upcoming Insurance Hikes

October 28, 2025

Imagine logging in to renew your health-insurance plan this November and discovering your monthly premium has nearly doubled — all because Congress couldn’t agree to fund the tax credits that have quietly kept your coverage affordable. That’s the stark reality for millions of Americans enrolled in the health insurance marketplaces under the Affordable Care Act (ACA).

Under the ACA, individuals and families who do not get health insurance from an employer or through a public program can shop at a federal or state-based “Marketplace.” Insurers offer plans in metal tiers (Bronze, Silver, Gold)—with varying premiums, deductibles, and out-of-pocket costs. What keeps many of these plans affordable is the federal premium tax credit. If you qualify (mainly based on income as a share of the federal poverty level), you receive a subsidy that reduces the monthly premium you pay.

Because of this subsidy, many enrollees pay only a modest portion of what might otherwise cost thousands of dollars. The Kaiser Family Foundation (KFF) found that thanks to the enhanced tax credits, an individual making $28,000 “will pay no more than around 1 % ($325) of their annual income towards a benchmark plan.” The system ties a person’s share of premium costs to their income, and the subsidy covers the rest. This critical safeguard has kept coverage within reach for millions of lower-income Americans.

Why Subsidies Are in Danger of Expiring

The wrinkle: the enhanced subsidies many people now rely on are temporary unless Congress renews them. These enhancements were introduced by the American Rescue Plan Act in 2021 and extended under the Inflation Reduction Act of 2022. They expanded eligibility (including households earning more than 400% of the poverty level) and reduced out-of-pocket costs for individuals. But unless renewed by year’s end, they sunset at the end of 2025.

Even more urgent: insurers are already filing their proposed 2026 premiums, assuming no renewal of the enhanced tax credits. KFF reported that enrollee net premium payments could increase by 114 % on average—from about $888 in 2025 to about $1,904 in 2026—if the enhanced credits expire.

What People with Low Income Will Face

For low- and moderate-income Americans who depend on the marketplaces, the expiration of enhanced subsidies is more than theoretical—it’s a budget-breaker.

If subsidies are eliminated, many enrollees will see their monthly premium contributions skyrocket. KFF’s analysis shows that without the enhanced tax credits, average annual premium payments for subsidized enrollees would more than double. Some households will lose eligibility altogether. For people earning above 400 % of the poverty level, that subsidy cliff means they go from some assistance to none. KFF explains that “people with incomes over four times the poverty level will no longer be eligible for any financial assistance” if the enhanced credits expire.

The rate increases compound the effect: insurers are proposing median premium hikes of around 18 % for 2026. Those who are already barely making ends meet may find the new premiums impossible. One enrollee in Florida told Health News Florida that she’s already struggling to cover other rising costs. “The rent is going up. The water bill is going up,” said the Florida resident. “I cannot afford a premium hike.”

A missing subsidy cushion means not just higher premiums but a greater risk of losing coverage altogether. As Jason Levitis, Senior Fellow at the Urban Institute, explained, “If you have fewer subsidies, you’re going to have less health coverage and less health care.”

Why Enrollment Has Grown Recently

Enrollment in the marketplaces has surged in recent years, and the subsidy enhancements are a significant reason. Before the enhancement period, around 11 million people used the marketplace; now more than 24 million are enrolled.

Several factors have driven the growth. The enhanced tax credits increased eligibility and lowered what many paid, making coverage far more accessible. Improved outreach and usability—especially as state-based marketplaces matured—helped consumers find and keep plans more easily. At the same time, rising costs in employer-based coverage pushed more people to shop for plans individually. According to KFF, the enhancements cut annual premium payments by an estimated 44 % (about $705) for many subsidized enrollees. “The enhancements made it easier for millions of people to afford health coverage,” said Larry Levitt, Executive Vice President for Health Policy at KFF. “If they expire, we could see those gains wiped out almost overnight.”

In short, more help meant more people using the marketplace. The flip side is that less help could mean fewer people—and higher premiums for those who stay.

What’s at Stake

At the core of the current federal budget impasse (which led to the shutdown beginning October 1, 2025) is a fight over whether to extend the enhanced subsidies. Democrats insist that any funding deal must include the subsidy extension, arguing that letting them expire would cause a major affordability crisis. Republicans are pushing for reopening the government without tying the subsidy question directly to the budget deal, saying the issue should be negotiated separately.

From a consumer standpoint, the stakes are enormous. Without subsidy extensions, millions may lose assistance, face steep premium increases, or drop coverage altogether. KFF’s district-level data show that premiums would at least double in many parts of the country if the enhancements are not renewed. Rising premiums could also cause healthier enrollees to opt out, worsening the insurance risk pool and pushing rates even higher in subsequent years.

For families already squeezed by inflation and rising living costs, this would trigger an affordability crisis. “The cost of health insurance is never going to be low enough for a person who makes just above poverty to be able to afford it,” said Cynthia Cox, Director of KFF’s Program on the Affordable Care Act. “If you want that person to have health insurance, then there needs to be financial assistance.”

If Congress doesn’t act, many Americans will pay far more—or lose coverage altogether. As open enrollment begins, millions will face difficult choices about whether they can keep the coverage that has protected them for years, and whether Washington will act before the bills come due.

Insure You Know

Before you finalize your renewal or new plan selection, it may help to check out Insure You Know — a secure, central place where you can store and manage the critical information your family will need (insurance details, plan documents, contact numbers, and more). Taking a few minutes now to upload your coverage information ensures you’re ready for whatever changes lie ahead, and helps keep everything organized so you’re not scrambling when the numbers on your bill jump or the policy rules shift.

Term vs Whole Life Insurance: Simple Guide for Smart Choices

October 15, 2025

Why Life Insurance Matters

Life insurance is really about looking after the people who depend on you. It is not just a form to fill out or another bill to pay. Imagine suddenly not being there. The bills do not stop, school fees still need paying, loans keep coming. Life insurance helps make sure your family is not left scrambling.

Choosing the right type can feel confusing at first. Term life, whole life. The names almost sound the same, right? But they work very differently. Understanding each one can save a lot of money and prevent unnecessary stress later.

Many young people think, “I’m fine for now, I’ll deal with it later.” It makes sense to think that way, but starting early usually keeps premiums lower and makes managing everything much simpler. It might not be exciting to think about, but it is practical and that is what counts in the long run.

Term Life Insurance: Affordable and Straightforward

Term life insurance is actually pretty simple once you get the hang of it. It covers someone for a set number of years, maybe 10, 20, or 30. During that time, premiums are paid. If something happens to the insured, the family gets the payout. If nothing happens, the policy just ends. That’s really it, nothing more complicated than that.

You can kind of think of it like renting protection. It’s really useful when life gets busy and responsibilities are piling up, paying off a home, taking care of kids, or managing loans.

For instance, imagine a 30-year-old buying a 25-year term policy worth ₹1 crore. The annual premium could be around ₹10,000. If something happens during that time, the family gets ₹1 crore. If nothing happens, the coverage stops. No frills, no fuss. Simple, affordable, and gives peace of mind exactly when it’s needed.

Whole Life Insurance: Protection That Lasts

Whole life insurance is actually a bit different from term insurance. So, it covers someone for their whole life, usually up to age 99 or 100, as long as the premiums are being paid. Part of what you pay goes into a cash value account, and over time, that grows slowly. And here’s the thing, you can borrow from it, take some money out if you need to, or even use it to pay future premiums.

This kind of policy is really good for people who want coverage that lasts their entire life or are thinking about leaving some money for their family later on.

For example, imagine a 30-year-old picking a whole life policy worth ₹1 crore. The annual premium could be about ₹60,000. Over the years, the cash value grows little by little, and whenever the insured passes away, the payout is guaranteed. Yeah, it costs more than term insurance, but it gives security for life and a bit of extra flexibility if something comes up.

Understanding the Key Differences

Here’s the thing, term insurance and whole life insurance aren’t exactly the same, even though people often mix them up. Term insurance is temporary and usually cheaper, kind of like renting a flat. Whole life insurance lasts your whole life and costs more, a bit like buying a house that also builds value over time.

The big difference is in how they work. Term insurance mostly just gives protection. Whole life insurance gives protection plus a bit of savings. Term is good for short-term stuff, like paying off a home loan or taking care of kids until they’re grown. Whole life insurance makes more sense if someone wants coverage for life or wants to leave some money for their family later on.

Why Term Insurance Appeals

Term insurance is attractive because it’s cheap, straightforward, and offers high coverage. Some policies allow conversion to permanent insurance if circumstances change.

The downside is obvious: coverage ends after the term, renewals can be costly, and there is no cash value to access.

Why Whole Life Insurance Appeals

Well, whole life insurance is something people usually pick if they want coverage that lasts their whole life. You get a guaranteed payout, and part of what you pay slowly builds cash value. It can also help with long-term stuff, like leaving money for your family or passing on wealth.

Here’s the thing though, it’s not all simple. The premiums are higher, and the cash value doesn’t grow very fast compared to other ways of investing. And some of these policies can get a little tricky, so it really helps to read the fine print and make sure it works for you.

How to Choose the Right Option

So here’s the thing, picking between term and whole life insurance really depends on your own situation. Term insurance is usually good for young families, people with temporary money responsibilities, or anyone who wants higher coverage without spending too much. Whole life insurance makes more sense if you can handle higher premiums and want protection for your whole life, along with a little savings built in.

Basically, term insurance is all about protection. Whole life insurance is protection plus a small financial cushion. It’s not complicated, but it helps to think about what actually fits your life, your budget, and your family’s needs.

A Practical Strategy

Here’s the thing, some families like to mix things up a bit. They go for term insurance to get the protection and then put the extra money they would have spent on a whole life policy into other investments. Over time, those investments can grow quite a bit while still keeping the family covered.

For example, if someone saves about ₹50,000 every year by choosing term insurance and invests it wisely, that could turn into a decent fund in 25 years. This way, the family gets immediate protection and some long-term growth too. It’s kind of a smart balance if you can plan it right.

Conclusion

Well, term life and whole life insurance do kind of different things, you know. Term insurance works if someone just wants coverage for a certain time and doesn’t want to spend too much. Whole life insurance is more for people who want coverage for their whole life and maybe a little savings along the way.

Here’s the thing, it really helps to think about your family, your money, and what your long-term goals are. Picking the right policy can give some peace of mind and make sure your loved ones are taken care of when it really matters.

QLAC 101

August 15, 2024

If you’ve saved well for retirement, then you may find you can cover your living expenses without needing to withdraw from your retirement accounts. But if you think that by age 73, you won’t need your full required minimum distributions or RMDs, then you might want to consider getting a qualified longevity annuity contract, or QLAC.

Anyone between the age of 18 and 75 can purchase a QLAC, but there may be some people that this annuity makes more sense for. If you’re looking to avoid the market risk on some retirement accounts and ensure a steady, guaranteed income in retirement, a QLAC is probably a good fit for you. If you also have concerns about the longevity of your savings and having enough money later in life, then you may benefit from a QLAC.

Here’s everything you need to know about a QLAC before deciding if it’s right for you.

How a QVAC Could Lower Your RMDs

A QLAC is a deferred fixed annuity contract sold by insurance and financial companies that you purchase with money from a retirement account, like a 401(k) or an individual retirement account (IRA).It’s important to know that Roth IRAs cannot be used to purchase QLACs as they do not come with RMDs to begin with.

RMDs are mandated starting at the age of 73 as of this year, but that will rise to age 75 in 2033. One appeal of the QLAC is that it can reduce the balance in your retirement accounts used to calculate those RMDs. “People tend to spend their RMDs,” says Steven Kaye, a financial planner in Warren, New Jersey. “So a QLAC forces people—in a good way—to leave more money in their IRAs,” he says.

One way to avoid using your RMDs is to use the funds from one of your retirement accounts to purchase a QLAC, which will guarantee that you receive regular payments for as long as you live. “So, if you used 25% of a $400,000 qualified account, your $100,000 purchase of a QLAC would immediately reduce your RMDs by 25%,” says Jerry Golden, investment advisor. “And the income from a QLAC could be deferred until as late as age 85,” he says.

When you choose a QLAC, you’ll be able to set your payout date, which is when you’ll begin receiving payments. Just like with Social Security, the longer you wait to receive payments, the higher the payments will be. Once you have a QLAC, you’ll be able to delay RMDs until the payout date of your QLAC, which can be no later than age 85.

The Tax Benefits of Having a QLAC

Once you withdraw money from your QLAC, you’ll need to pay income taxes on it. However, a QLAC can be an efficient tax planning strategy. For example, by using $100,000 of a traditional IRA to purchase a QLAC, you’ll reduce the balance of your IRA by $100,000, which will lower the amount you’ll need to take out for RMDs. The lower your RMD, the lower your income will be on that, which could significantly reduce the income tax you’ll owe.

QLAC Contribution Limits and Inflation Riders

You are now permitted to buy a QLAC for up to $200,000 from an eligible retirement plan. Previously, you were limited to whichever was lesser of $145,000 or 25% of your account balance. The current $200,000 upper limit is a combined cap that applies to all of your eligible retirement accounts, even if you take money from different accounts or purchase more than one QLAC. But if you and your spouse have your own eligible retirement accounts, then you can each spend up to the $200,000 limit on your own QLACs.

Since a QLAC locks in future payments, you are protecting your retirement money from market dips later in life. But unless you purchase an inflation rider with your QLAC, which will lower the initial amounts you receive from an annuity, your monthly payment may lose value over time.If you’re considering acquiring a QLAC, then you’ll want to work with a financial advisor to make sure you’re picking the right one.

Considering Your Spouse When Purchasing a QLAC

Some QLACs offer a survivor payout, also referred to as contingent annuity payments. These would continue your annuity payments to your designated beneficiary, which is usually a spouse, after your death. Other QLACs offer death benefits that would return any unused premiums to your beneficiaries through a lump sum or series of payments. If you have a spouse or individuals who will depend on your annuity after your passing, then you need to make sure any QLAC you choose has one of these features. Without these features in your annuity, your survivors would get nothing.

In addition to making sure your QLAC comes with a survivor payout or death benefit, you may also consider getting a joint QLAC with your spouse. If you’re married, a joint QLAC would provide income payments that continue for as long as one of you is alive. The only downside to choosing a joint contract is that it decreases your income payments, compared to a single life contract.

When a QLAC Isn’t For You

If you’re 65 and in poor health, you probably don’t want to wait until age 85 to start receiving income payments, so a QLAC may not benefit you at all. “If the probabilities are that you have a longer than average life expectancy, QLACs can be a windfall,” says Artie Green, a financial planner. “But if you have a shorter than expected longevity, of course, that works against you with any annuitization.” QLAC recipients can use their funds on whatever they want, but often they spend it on late-in-life health care or housing costs. The purpose of a QLAC is longevity protection that could minimize or even eliminate the risks of running out of money.

There are really only two scenarios in which a QLAC is a good fit. The first is if you have reached age 73 and do not need your RMDs to cover expenses. The second is if you think you’ll reach 73 and not have enough funds to pull from. QLACs can be a safeguard that guarantees you an income late in life, while also reducing your need for RMDs and even lowering your income taxes on them. At Insureyouknow.org, you may keep all of your financial and retirement planning in one place, making it easy for you to forecast and plan for your future.

Five Things Happy Retirees Have in Common

June 15, 2024

The transition into retirement can be difficult, when work no longer provides a sense of identity and accomplishment. The change can be startling, especially when most people don’t switch to part-time schedules on the way out of their full-time careers. “We don’t really shift our focus to, how do we live well in this extra time,” says M.T. Connolly, author of The Measure of Our Age. “A lot of people get happier as they age because they start to focus more on the meaningful parts of existence and emotional meaning and positive experience as finitude gets more real.”

While most people account for how much money they’ll need when it’s time to retire, there are many other factors to consider when planning for a fulfilling retirement. Here are five things that happy retirees have in common.

Feeling a Sense of Purpose

There are several approaches to staying active and finding purpose after leaving a career. “Your retirement schedule should be less stressful and demanding than your previous one, but we don’t need to avoid all forms of work or service,” says Kevin Coleman, a family therapist. “Find some work that you take pride in and find intrinsically meaningful.”

Many retirees, for example, choose encore careers, where instead of working for the money, they are working for the enjoyment of the job. Besides finding a new job, there are other simple ways to feel purposeful during retirement. Purpose can be found by making oneself useful, such as by volunteering in the community, joining a community board, or participating in an enjoyable activity with a group, like a gardening club. Many retirees enjoy volunteering to take care of their grandchildren or helping their older friends with caregiving duties. Finding purpose doesn’t need to be complicated and can be achieved through simple acts of showing up for others and being open to new connections.

Finding Ways to Connect

As nearly 25% of those who are 65 and older feel socially isolated, finding ways to connect are important for mental and physical well-being during retirement. One way to connect is through storytelling. Sharing our stories with the people we care about strengthens our social bonds and helps us feel less lonely. Storytelling also helps people pass down their family memories, especially when we share stories with younger relatives, such as with grandchildren. It’s a nice feeling to think that your memories will live on through your loved ones. “The models we have for aging are largely either isolation or age segregation,” says Connolly. “There’s a loss when we don’t have intergenerational contact. It impoverishes our social environment.” Perhaps the best thing to do as you age is to cherish and foster these relationships with younger relatives.

Making Plans for the Retirement Years

Budgeting for your retirement is crucial to happiness during the retirement years. Successful retirement planning includes paying off debts prior to retiring and saving for unexpected expenses or emergency funds in addition to a standard monthly budget. According to a survey conducted by Wes Moss, author of You Can Retire Sooner Than You Think, the happiest retirees are those who have between $700,000 and $1.25 million in liquid retirement savings, such as stocks, bonds, mutual funds, and cash. His research also found that retirees within five years or less of paying off their mortgages are four times more likely to be happy in retirement. This is because the mortgage payment is typically the most significant expense, so those retirees who own their homes feel safer and more at peace once they no longer have that bill. Plus, not having a mortgage payment due every month dramatically lowers their monthly expenses and can help retirement savings last longer.

Many retirees overlook retirement planning beyond their finances. New research from the Stanford Center on Longevity shows that where someone lives in retirement can affect their longevity. Researchers found that people over the age of 60 who lived in upper-income areas lived longer due to having more access to health and social services. They also credited strong social networks and a sense of community to living longer. So perhaps there’s a city or area that you’ve always dreamed of living in or you’d like to live closer to family. Think about where you want to live when you’re done working and then plan for it before you retire.

Beyond saving up and thinking about where you want to spend your retirement years, setting goals for once you’re in retirement is equally as important. “Research suggests that those who think about and plan for what they will do in retirement in advance are far happier and fulfilled once they actually retire and begin living this phase of life,” says financial planner Chris Urban. “Sometimes it is helpful for people to write down what they plan to do every day of the week, what goals they have, who they want to spend time with and what they want to do with them.”

While your goals before retirement were likely centered around career and finances, it will be important to set different kinds of goals once you’re retired. Having goals doesn’t become less important just because you’re no longer working. “If you really want something, maybe a new romance, then take a concrete step in that direction,” says psychiatry professor Ahron Friedberg. “Don’t ever tell yourself that it’s too late.”

Prioritizing Both Physical and Mental Health

With a full-time career no longer on the schedule, cooking healthy meals at home, getting enough sleep, and finding ways to be more physically active everyday will be easier. It will also be important to keep up on medical appointments and preventive therapies. A study conducted by Harvard shows that even people who become more physically active and adopt better diets later in their lives still lower their risks of cardiovascular illnesses and mortality more than their peers who do not. “Not all core pursuits include physical activity or exercise, but many of the top ones do. I refer to them as the ‘ings’—walking, running, biking, hiking, jogging, swimming, dancing, etc.,” says Moss. “These all involve some sort of motion and exercise.” The most sustainable form of physical activity will be doing more of those activities that you enjoy and that move your body.

In addition to caring for your physical health, focusing on your mental health is just as important, especially as you age. According to Harvard’s Medical newsletter, challenging your brain with mental exercise activates processes that help maintain individual brain cells and stimulate communication between them. So choose something new or that you’ve always wanted to learn. Take a course at a community college or learn how to play an instrument or speak a language. If you enjoy reading, visit the library every week for a new book. If you enjoy helping others learn, then looking into a part-time tutoring job or volunteering to tutor is a way to challenge yourself mentally, connect socially, and feel a sense of purpose.

Prioritizing your overall health includes asking for help when you need it. If you reach a point where you need assistance with daily tasks and activities, then you shouldn’t hesitate to ask for help early. Whether it’s family members or caregiving services, finding help with the things that are becoming difficult for you is the best way to maintain your independence for as long as you can so that you may continue to thrive during your retirement years.

It’s important to think about how you want to spend your retirement before it’s here. While many people only consider their finances when they begin to plan for the future, there are other factors, including how you’ll spend your time, where you’ll live, and your overall health that will impact the quality of your retirement years. With Insureyouknow.org, storing all of your financial information, medical records, and planning documents in one easy-to-review place will help you plan for what can be the best years of your life.

Six Things to Know about SIMPLE IRA

April 30, 2024

Offering a SIMPLE IRA (Savings Incentive Match Plan for Employees) to employees is an effective way for small businesses to offer their employees a retirement plan. At a glance, this plan allows both the employer and employee to make contributions, and there are less reporting requirements and paperwork involved for the small business owner. Besides the ease in which these plans can be established for employees, the main perks are tax incentives for both the employer and the employee. “They are fairly inexpensive to set up and maintain when compared to a conventional retirement plan,” says client advisor at First American Bank Karina Valido. “For employers, contributions are tax-deductible. For participants, contributions and earnings are not taxed until withdrawn.”

Even though the SIMPLE IRA is a straightforward retirement option, here are six things to know about this plan, whether you’re an employer or an employee.

- Employee Contribution Limits in 2024

With a SIMPLE IRA, an employee can, but isn’t obligated to, make salary reduction contributions. In 2024, the maximum amount an employee under the age of 50 can contribute is $16,000. With a SIMPLE IRA, you may also contribute to another retirement plan as long as both contributions don’t exceed the yearly limit. The annual limit for combined SIMPLE IRA and 401(k) contributions in 2024 cannot be more than $23,000 or $30,500 for people who are 50 or older. Since an employer cannot offer both plans, this would only apply to those employees who held a previous account elsewhere.

- Employer Contribution Requirements

Employers must do one of two things: match employee contributions or make nonelective contributions. If an employer chooses to match each employee’s salary reduction contribution, they must do so by up to 3% of their employee’s compensation. While an employer may choose to match less than 3%, they must at least match 1% for no more than two out of five years. If an employer chooses to make nonelective contributions of 2% of the employee’s compensation, they must do so for every employee, regardless of having some employees who are making their own contributions. So if an employer chooses to make nonelective contributions, then they must also match the contributions of those employees who choose to contribute to their own plans.

- SIMPLE IRA Tax Advantages

For employees, salary reduction contributions to their SIMPLE IRA reduces their taxable income and their investments will grow tax-deferred over time. Because it’s a tax-deferred account, you won’t need to pay capital gains taxes when you buy and sell investments within the account. Plus, unlike many other retirement plans, such as a 401(k), employer contributions to a SIMPLE IRA are immediately vested and belong to the employee.

Employers also benefit from tax incentives with the SIMPLE IRA. They can get a tax credit equal to 50% of the startup costs, or up to a maximum of $500 per year, for three years. This credit is in addition to the other tax benefits they will receive from contributing to employee retirement plans.

- All About Withdrawals

During retirement, withdrawals will be taxed as regular income. Before the age of 59 ½, there’s a 10% penalty on withdrawals in addition to the income taxes you would owe. With the SIMPLE IRA, the withdrawal penalty rises to 25% if the money is taken out within two years of the plan being contributed to. Under qualified exemptions, like higher education costs or first home purchases, then you may avoid an early withdrawal fee, but you would still have to pay the taxes.

- Eligibility for SIMPLE IRAs

The Small Business Job Protection Act of 1996 created the SIMPLE IRA. It was designed with small businesses and self-employed individuals in mind and meant to be simple, accessible, and inexpensive. “A SIMPLE IRA is a small-business-sponsored retirement plan that, as the name indicates, is simple to establish and maintain,” explains financial advisor at Marsh McLennan Agency Craig Reid. “Available to U.S. companies with 100 or fewer employees, SIMPLE IRAs are a cost-effective alternative to the mainstream 401(k) plan.”

In order to be eligible for a SIMPLE IRA, an employer must have fewer than 100 employees and have no other retirement plan in place. They must also make contributions each year. For an employee to be eligible, they must receive at least $5,000 in compensation during any two prior years and expect to receive the same during the current year.

- The Difference Between SIMPLE IRA and SEP-IRA

Both a Simplified Employee Pension (SEP-IRA) and a SIMPLE IRA are employer-sponsored retirement plans that offer employees a tax-advantaged way to save for their retirement. Contributions in each grow tax-deferred until they are withdrawn during retirement. They are each designed to be easily established in small businesses, especially when compared to a 401(k).

One key difference between the two plans is that while a SIMPLE IRA allows both the employer and employee to make contributions, the SEP-IRA only allows the employer to contribute. The SEP-IRA, though, does allow higher contributions, which will be limited to $69,000 in 2024, compared to $16,000 in 2024 for the SIMPLE IRA. The other main difference between the two plans is that any employer can offer a SEP-IRA, while only businesses with less than 100 employees qualify for offering the SIMPLE IRA.

If you’re a self-employed individual, a small business owner, or you have recently begun working for a small business that offers you a SIMPLE IRA, it will benefit you to know the upsides of having one and understand the rules around the plan. With Insureyouknow.org, you can store all of your financial information and records in one place so that you may stay organized and allow yourself the best decision-making process in your retirement planning.

2024 Changes that Would Impact Your Retirement Finances

April 1, 2024

Changes to retirement regulations are making 2024 out to be the perfect time to reexamine your retirement planning and make sure you’re getting the most out of your savings.

“The rules are constantly changing,” says director of Personal Retirement Product Management at Bank of America Debra Greenberg. “It’s always a good idea to familiarize yourself with what’s new to see whether it makes sense to take advantage of it.”

Here’s what you should know about several changes to retirement regulations in 2024.

It Pays to Plan for Retirement

While the changes to retirement regulations may seem small, Americans need all the help they can get right now. According to the National Council on Aging, up to 80% of older adults are at risk of dealing with economic insecurity as they age, while half of all Americans report being behind on their retirement savings goals.

“The IRS adjusts many things each year to reflect cost of living and inflation,” says Jackson Hewitt’s chief tax information officer Mark Steber. “It happens each year and taxpayers shouldn’t be alarmed — they might even have a bigger benefit.” Since retirement contributions are pre-tax, saving for retirement actually lowers your taxable income, which may even place you into a lower tax bracket. Plus, you may even be eligible for a tax credit of up to 50% of what you put into your retirement accounts.

Contribution Limits Will Increase

The contribution limits for a traditional or Roth IRA are increasing in 2024. The limit on annual contributions to an IRA will go up to $7,000, up from $6,500 last year.

Individuals will be able to contribute more to their 401(k) and employer-based plans as well. For those who have a 401(k), 403(b), most 457 plans, or the federal government’s Thrift Savings Plan, the contribution limit is increasing to $23,000 in 2024, which is $500 more than last year. Those who are 50 and older, can contribute up to $30,500 into the same accounts.

Starter 401k Plans are Possible

In 2024, employers who don’t sponsor a retirement plan may offer a Starter 401(k) deferral-only arrangement. A starter 401(k) is a simplified employer-sponsored retirement plan with lower saving limits than a standard 401(k). Employers are not allowed to make contributions, and employee auto-enrollment is required. In 2024, the annual contribution limit to this plan will be $6,000. Beginning this year, employees with certain qualifiable emergencies may also make penalty-free withdrawals from their 401(k) of up to $1,000, though they would still have to pay the income tax on those withdrawals.

529 Plans Can Now be Converted Into Roths

For parents who will no longer need their 529 funds for their children, the Secure 2.0 Act will allow for a portion of the 529 to be rolled into a Roth IRA. Beginning January 1st, the funds can either be used for educational expenses or put toward retirement, as a Roth IRA rollover. You may rollover up to $35,000, free of income tax or any tax penalties. The only limitations are that the 529 must have been in place for at least 15 years, and certain states may not allow the rollover.

Changes to Social Security and RMDs

In January, Social Security checks will increase by 3.2% due to the latest COLA, or cost-of-living adjustment. On average, Social Security monthly benefits will increase by $59 a month, from $1,848 to $1,907. Those who receive survivors or spousal benefits will receive even more.

For 2024, the maximum benefit for a worker who claims Social Security at FRA (Full Retirement Age)is $3,822 a month, which is up from $3,627 in 2023. For 2024, the FRA is 66 years and 6 months for those born in 1957 and 66 years and 8 months for those born in 1958. That means that anyone born between July 2, 1957 through May 1, 1958 will reach FRA in 2024.

The IRS uses a calculation based on the amount in your retirement account and your life expectancy to determine the minimum amount you are required to take out each year, known as RMDs (required minimum distributions). Secure 2.0 increased the age for starting RMDs from 72 to 73, effective in 2023. If you are subject to RMDs, then you must make your withdrawal by the end of this year or by April 1st next year if it’s your first year being eligible. So if you turn 73 in 2024, you’ll have until April 1, 2025 to make your first RMD.

Anyone receiving more Social Security but paying Medicare premiums may not feel much of a difference in their increased Social Security benefits since standard Medicare Part B premiums are rising by 6%. As many participants have their Medicare premium deducted right from their Social Security payment, the $9.80 increase will take a portion of the average $59 benefit increase. The annual deductible will also increase this year from $226 to $240.

Insureyouknow.org It will always be important to review your retirement savings every year, but this is becoming even more important to do in the face of rising costs and changing regulations. With Insureyouknow.org, storing all of your financial information in one easy-to-review place can help you ensure that you are still on track to meet your retirement goals at the start of each annual review.

How ChatGPT is Shaping Retirement

October 15, 2023

Chat GPT is an artificial intelligence program that can answer human questions. This chatbot is able to understand human language that is spoken or written and then uses algorithms to process and analyze this information in order to produce answers. For instance, you may ask ChatGPT informative questions such as how climate change is affecting endangered species, but Chat GPT can even be directed to write a poem. When it comes to finances, ChatGPT may even be able to help someone begin their retirement planning.

ChatGPT Provides Content, Not Human Advice

Anyone can ask ChatGPT anything, and they will receive a remarkably well-rounded response. If someone were to ask what their retirement plan should include, the chatbot will provide an outline of the basic elements of a common retirement plan. The problem with this is that ChatGPT won’t know the person asking the question and be able to understand the individual details of their life that would make a difference in their retirement planning.

While Chat GPT may not completely replace the value of a human financial advisor, that doesn’t mean that financial advisors won’t need to change the way in which they advise clients to plan for their retirement. If anyone can get a basic plan through ChatGPT, then the services provided by an advisor need to become more about the one thing ChatGPT can’t provide: the human understanding and emotional side of advice. Despite having spent decades taking the emotion out of financial decisions, financial professionals will have to pivot to provide more humanity than ever.

How AI Can Improve an Advisor’s Abilities

Once upon a time, the internet threatened travel agents everywhere, as people could suddenly book their own plane tickets, hotel rooms, and rental cars themselves, from the comfort of their home computers. But travel agents are alive and well, and that’s because the internet still couldn’t do one thing that an agent could: understand a client’s needs and provide personal advice. Instead of mere transactional planning, personalized insight is the new premiere service that a travel agent can provide, and financial planners can grow to do the same.

While ChatGPT can provide concrete information, it cannot begin to factor in the unique preferences of an individual. True conversation is more than the exchange of information. It involves feelings and the confirmation that the person you’re speaking with understands you. A good financial advisor already understands this. Their job is about more than just offering retirement plans; people need empathy. Financial advisor Patti Brennan says her clients “are looking for someone who isn’t just focused on managing their money; that’s just table stakes. What they really want is to know they’ve got someone they can count on during times of crisis; someone who will be a trusted advocate for their future and quality of life.”

Mitchell Morrison, CEO and founder of Eyeballs Financial, says, “ChatGPT is like building a chassis for the financial plan. Its chief weakness is that the answers you get are only as good as the questions you ask.”

While a machine can provide the building blocks of a good plan, an advisor has the capability to understand the complexities of financial planning and the nuances of a person’s life. Together, ChatGPT and the advice from a professional can be used to formulate a plan that is more well-rounded than if someone just relied on one or the other. Rob Leiphart, a certified financial planner at RB Capital Management, adds that, “ChatGPT lacks one crucial step needed in financial planning and investment management: KYC,” or know your client. “It doesn’t begin by asking questions of its own in order to hone its responses. Instead, it provides generic or basic advice,” he says.

While AI ‘s abilities will evolve, financial advisors will be required to as well. Professionals should view ChatGPT as a tool and reevaluate their role in retirement planning. While clients can be well-versed through the framework that ChatGPT can provide them, financial planners can become educators, coaches, and navigators of their retirement plans.

What AI Can Do For You Now

ChatGPT can do more than provide information on how to begin planning for retirement. It can also be used as a resource to think outside of the box in terms of finances. Here are five ways anyone can use ChatGPT to improve their finances now.

Whether you’re interested in supplementing your income now or during retirement, you can ask ChatGPT, “What are the best side gigs for retirees, in my area, or in my field of work?” AI will provide a list of options ranging from consulting, house sitting, or personal errands.

2. Build a better resume

Perhaps you’d like to make more money in your working years or there are a handful of positions you’ve always wished you could land. ChatGPT can help make your resume stand out by suggesting which skills recruiters are looking for in certain positions.

3. Get your business off the ground

ChatGPT could tell you how much you’ll need to start that business you’ve always dreamed of starting, including what resources you’ll need to get going, projected earnings, and even help with sales copy. Whether you’re selling goods or services, you’ll need good advertising to attract potential clients. ChatGPT can provide you with a better idea of what your business idea will entail and help you to create a detailed plan of action.

4. Get tips for writing a better house listing

Planning to make money for retirement by selling your house or planning to move when you can retire are both common goals. An attractive house listing can help you get the best offer on your current property. Paired with gorgeous pictures of your home, ChatGPT can help you write the listing that will get you the most interest. You could even use ChatGPT to help you buy your home elsewhere by researching the most cost effective places to retire.

5. Find financial planners in your area

Once you’ve decided it’s time to start thinking about your retirement, ChatGPT can provide you with a list of qualified and highly-rated financial advisors in your area. Plus, educating yourself through ChatGPT on common retirement plans before you meet with your advisor will give you an idea of what to discuss at your meeting.

Retirement planning can be overwhelming, but you’ll benefit from using every resource available to you, including ChatGPT. For now ChatGPT is an excellent starting point but shouldn’t be the main resource of your final plan. Insureyouknow.org can help you compile your research, store your financial records, and serve as a valuable place to regularly revisit and fine tune your retirement plan.

What Constitutes a True “Emergency”?

May 28, 2018

You’re a responsible person. You’re saving for retirement. You have a 529 plan set up to help pay for your daughter’s college education. Your car is paid off. You have an adequate amount of life insurance. You’re using InsureYouKnow to make sure your loved ones know how to access your important documents and financial information if needed. And you have six months of living expenses set aside in an emergency fund.

Then the unexpected happens: The alternator goes out in your car. It’s going to cost $400 to replace it.

Where do you find the money to pay for it?

If you answered, “My emergency fund,” you may want to take another look at your definition of “emergency.”

Your emergency fund is money you have socked away in case of a major life event, such as a job loss, divorce, or medical issue. This money would be used to cover your day-to-day expenses and bills if needed.

Washington Post columnist Michelle Singletary advocates the use of a separate fund—the “life happens” fund—for those pesky but somewhat predictable expenses that crop up.

“You’ll withdraw money from this fund to pay for unexpected or major expenses that don’t quite fit the dire straits definition,” Singletary wrote. “Car repairs would come out of this account. Start with trying to save $500, ideally increasing to a few thousand.”

Whether you call it the “life happens” fund, the “just in case” fund, or some other term, this fund is for those immediate expenses that aren’t quite catastrophic. These are expenses that result from situations that people often treat as emergencies but that in reality are expected, if irregular, like a broken appliance.

In an ideal world, you’d never touch your emergency fund. You wouldn’t lose your job. You wouldn’t get diagnosed with a major medical condition. You would have a regular, steady income with no major disruptive events in your life. For many people, this is indeed the case. That money sits in an easily accessible savings account where it earns minimal interest but supplies maximum peace of mind.

But even in an ideal world, you’re probably going to tap into your life happens fund fairly regularly. Even the most budget-obsessed person can’t predict every expense that may appear, such as the following:

- A storm blows through, knocking large tree branches onto the roof of your house that have to be sawed apart and hauled away.

- Your dog swallows a tennis ball and needs emergency surgery to remove it.

- Your toddler climbs onto the dishwasher door one too many times and it finally breaks.

- Your aunt dies and you need to fly out for the funeral.

In many of these situations, life is already stressful enough without you needing to scramble to come up with money for the resulting expenses. And you don’t want to tap into your emergency fund because that’s money you never want to touch. The life happens fund is the perfect compromise. Like an emergency fund, it’s kept in a savings account where it’s accessible on a moment’s notice. But unlike an emergency fund, taking money out of it won’t potentially result in your water getting shut off when you suddenly find yourself without an income.

Keep in mind that because you do need to access this fund somewhat regularly, it’s important to replace any money you take out as soon as possible. After all, life happens—and you never know when the next storm is going to pass through town.