Category: Monthly expenses

2026 Student Loan Defaults: Secure Your Financial Records

March 6, 2026

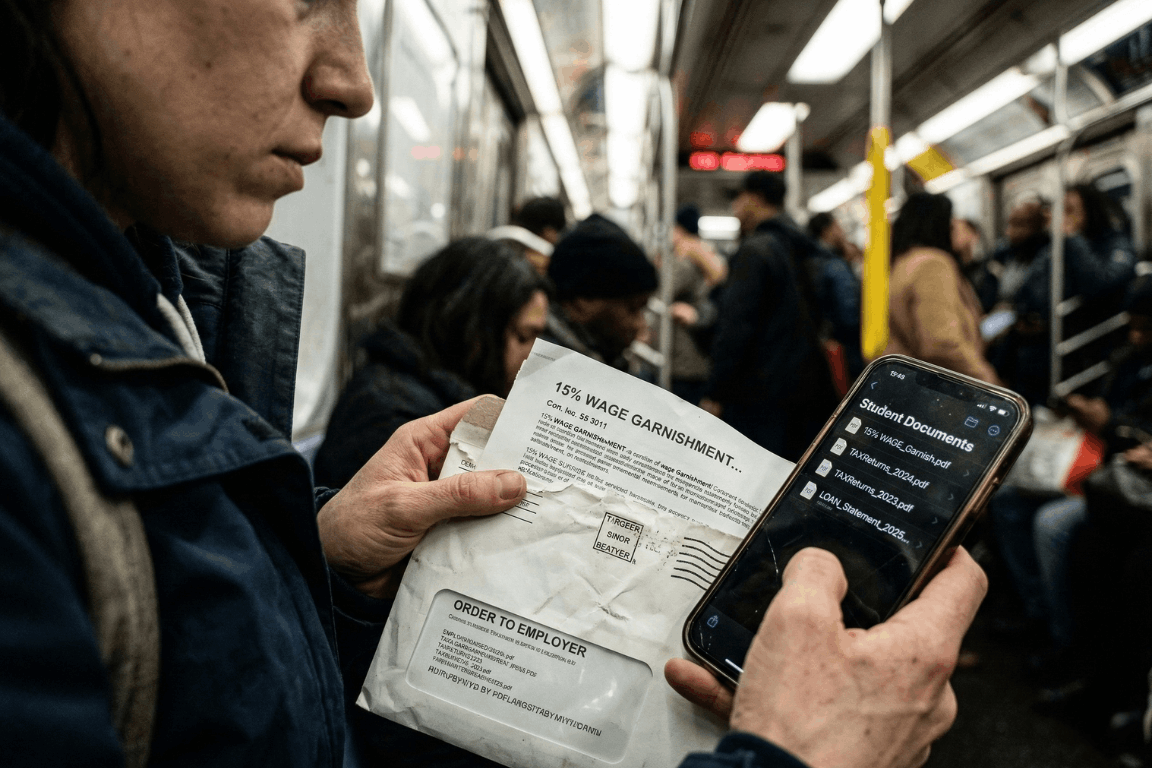

A massive financial wall hit millions of Americans earlier this year. Pandemic payment pauses are officially ancient history. The temporary relief programs dried up entirely. After months of messy court battles regarding income-driven repayment plans, the federal government decided to bring back its heaviest collection tools. Starting in early 2026, the U.S. Department of Education began sending administrative wage garnishment letters to defaulted borrowers. The numbers from major credit bureaus, like Experian, look pretty grim. The entire country is watching a massive wave of loan delinquencies happen in real time. People are suddenly staring down severe financial penalties. Getting through this economic squeeze requires a lot more than just reading news updates. It demands immediate, highly organized access to specific financial paperwork.

The 2026 Student Loan Landscape: A Shocking New Data Trend

So, who is actually defaulting right now? Historically, student loan defaults mostly hammered sub-prime borrowers. That whole narrative flipped completely upside down in 2026. Recent reports from credit bureaus reveal something entirely unexpected. Nearly a quarter of newly defaulted borrowers belong in the “prime” credit tier or even higher. These are the exact demographics the financial industry usually views as incredibly stable.

With over 5 million borrowers currently sitting in default status, and millions more falling behind every month, the economic pain is obvious. Borrowers are stuck navigating a bizarre maze of constantly changing payment plans. Making things worse, millions of accounts got bounced around between different private servicing companies over the last two years. Monthly payments got lost in the mail. Crucial paperwork simply vanished. Hold times to speak with basic customer service stretched into hours. Once a federal student loan reaches 270 days past due, it hits official default status. At that specific moment, the government gets to use an administrative superpower that regular credit card companies cannot even touch. They can literally take wages without ever stepping foot inside a courtroom.

Understanding Administrative Wage Garnishment: The 15% Reality

The fallout from a federal default happens fast. Through a process called Administrative Wage Garnishment (AWG), the Department of Education can legally force an employer to pull up to 15% of a borrower’s disposable pay. Disposable pay simply means the cash remaining after legally required deductions, like federal and state taxes, come out of the check.

Federal law does leave a very small safety net in place. Borrowers get to keep a weekly take-home amount equal to at least 30 times the federal minimum wage. But for anyone living from one paycheck to the next, suddenly losing 15% of their income is pure disaster. It usually means missing the rent, skipping the grocery store, or defaulting on other credit cards. Before the garnishment actually kicks in, the government must send a 30-day advance written warning. That specific 30-day window is basically everything. It acts as the only real timeframe a borrower gets to object or set up a different payment plan before their paycheck actually shrinks.

How to Stop Garnishment: The Heavy Burden of Proof

Borrowers holding a garnishment notice still carry some legal rights. During those 30 days, individuals can officially demand a hearing to stop the withholding order. They might attempt to prove extreme financial hardship. Or, they could try applying for federal loan rehabilitation. Rehabilitation usually involves agreeing to make nine on-time payments over a 10-month window to get the loan back on track.

Another route involves submitting a formal financial hardship appeal. Winning this appeal means legally proving that a 15% pay cut makes buying basic survival items impossible. The government looks at documented living expenses and compares them against very strict IRS Allowable Living Expense guidelines. If a family spends more on food or housing than the IRS thinks is necessary for that specific family size, the extra amount gets totally ignored. Proving hardship is notoriously difficult. Using these rights is never a walk in the park. It requires gathering highly specific legal and financial records immediately. In these types of administrative hearings, the burden of proof lands squarely on the borrower.

The Critical Role of Organized Financial Documents

Sloppy paperwork turns a bad money situation into an absolute nightmare. When the garnishment letter shows up, the clock ticks fast. Spending hours digging through cluttered email inboxes for old messages from loan servicers wastes valuable time. Tearing up the living room looking for utility bills to prove basic living expenses just fuels the anxiety. If a borrower fails to hand over the correct evidence within 30 days, their employer receives the order. The garnishment starts.

This explains exactly why relying on a secure, independent electronic safe deposit box changes the playing field. Keeping a dedicated digital vault for vital life information ensures nobody gets blindsided by aggressive debt collectors. Storing all important financial, legal, and contractual documents in one simple location gives borrowers a huge advantage. They can instantly grab the exact proof they need to protect their paychecks and negotiate with default resolution teams.

Essential Documents to Secure in a Digital Vault

To build a strong defense against a default warning, individuals should make sure the following documents are digitized, safely uploaded, and ready for action:

- Original Loan Agreements and Master Promissory Notes: Finding original contracts immediately helps verify the true debt amount. It also spots accounting errors and confirms which company actually owns the loan today.

- Complete Tax Returns: Proving financial hardship or enrolling in an income-driven repayment plan means submitting paperwork. The Department of Education demands recent federal and state tax returns before they even start talking.

- Official Pay Stubs: Current pay stubs are absolutely required to figure out actual disposable income. They also help verify that any proposed wage garnishment does not illegally drop below the minimum wage protection limit.

- Household Expense Records: Tracking basic living costs is a strict requirement for hardship appeals. Think about rent agreements, mortgage papers, utility bills, health insurance premiums, and pharmacy receipts. These papers help prove that living expenses are reasonable and fit within tight IRS standards.

- Correspondence with Loan Servicers: A strong paper trail of older payments, approved forbearances, and emails with the loan servicers can literally save the day. This proof is extremely important if someone needs to show a loan was wrongfully thrown into default in the first place.

The Absolute Security of Zero-Knowledge Storage

Privacy is absolutely non-negotiable when dealing with highly sensitive financial details. Relying on physical metal filing cabinets leaves people wide open to lost papers, house fires, or basic theft. Depending on regular, unencrypted email folders or a messy computer desktop basically hands sensitive financial data directly to hackers. Cybercriminals routinely target email servers specifically to find W-2 forms and tax returns. Once they grab those files, identity theft is pretty much guaranteed.

Using a specialized platform built with heavy-duty cloud encryption makes sure financial data stays completely private. The absolute best platforms run on Amazon cloud encryption mixed with a “zero-knowledge” setup. In a zero-knowledge system, only the actual account owner knows the password. The site administrators never get to see it. That means absolutely nobody else can ever gain access, view the files, or mine the stored documents to sell the data.

Strategic Document Sharing with Trusted Partners

Fixing a defaulted student loan is almost never a solo job. Borrowers usually need to bring in certified financial planners, tax accountants, or specialized student loan lawyers to help decode the messy federal rules.

Advanced secure portals allow individuals to selectively share specific document folders with these exact trusted partners. Sending unencrypted PDFs of tax returns and pay stubs back and forth through regular email is a massive cybersecurity hazard. Instead, account holders can simply give a legal advisor temporary, secure access to the required files right inside the encrypted vault. This targeted sharing feature speeds up the whole default resolution process, keeps communication secure, and leaves the rest of the vault totally locked down. Setting up automatic monthly reminders inside the portal also helps users routinely update their financial snapshots, keeping their defense strategy completely fresh.

Facing economic uncertainty requires a solid game plan. The return of federal student loan wage garnishments in 2026 creates a massive hurdle. Credit bureau data clearly shows that financial distress is hitting borrowers across every single demographic right now. Surviving this wave of defaults demands aggressive, proactive money management and flawless record-keeping. Centralizing vital financial documents into a secure, encrypted digital safe deposit box lets individuals tackle economic chaos with total confidence. Being prepared is simply the ultimate defense. It ensures that when critical financial information is needed the most, it stays protected, perfectly private, and instantly ready to use.

Cost of Tuition Shouldn’t Deter Students

July 15, 2025

According to the Education Data Initiative, the cost of tuition at a four-year college has increased by 141% over the last twenty years. The average yearly cost for classes ranges from $9,750 at a public school and $35,248 at a private school.

Even with the rising cost of college, a degree still gives many graduates a higher earning potential. In 2023, workers with a bachelor’s degree earned 61% more than those with a high school diploma.

A 2024 Third Way survey found that 29% of high school students don’t plan on attending college because of the price, but the cost of tuition doesn’t have to be a barrier.

Here’s everything parents and prospective students need to know about saving for college.

Earn a Two-Year Degree for Less

One of the easiest ways to save money on tuition is to remain where you are. When you attend an in-state school and can prove your residency, you avoid the much higher out-of-state tuition rate. You can save a lot of money on tuition if you earn the first two years of your degree at a public community college before transferring.

A year at a community college can cost as little as $3,500, while attending an out-of-state public university can cost $35,000 per year. Plus, if you weren’t accepted into your first-choice university after high school, earning your two-year degree improves your odds of being accepted into another four-year university as a transfer student.

Most states also offer dual enrollment during high school. This means that students can attend both their high school and a local community college simultaneously, earning college credits or even a two-year degree by the time they graduate from high school. Not only do graduates get a head start, but they also shave two years’ worth of tuition off their bottom line, since the state funds these programs.

“A lot of people don’t go to college because it’s just so expensive,” says Ahmad Shehadeh, a Roxbury Community College student who’s attending through a Massachusetts state-funded program. “So by tuition being free, it’s benefiting the community in a way, and I’m glad that other people like me will have the opportunity to go to college and pursue what they need to pursue: their dream.”

For more information on your state’s dual enrollment opportunities, you may check the Education Commission of the States.

Meet With Your Counselors

To find out if your high school offers programs like dual enrollment, you’ll need to meet with your school’s guidance counselor, and the sooner you start high school, the better. Guidance counselors can help students devise their post-graduation plans and assist with the college admissions process, financial planning for tuition, and even scholarship applications.

The same rule applies to college. Financial aid counselors can help prospective students determine how to pay for their classes. Contact a counselor at each of your potential schools. For instance, they will know if their college offers work programs, such as the Federal Work Study program, where students can work on campus part-time while enrolled in classes.

All high school and college counselors will likely encourage every potential student, regardless of age, to complete a FAFSA form to determine if they qualify for any government aid.

Saving With a 529 Plan

Parents who want to begin saving for their children at birth will yield the most savings if they start earlier. The longer you wait to begin saving for your child’s tuition, the more you’ll have to save up each month to have enough for four years of tuition by the time they graduate from high school.

Using a savings account that yields interest for as long as possible is also beneficial. A 529 plan is a high-yield savings account designed for educational expenses. If you can save $100 a month in a 529 plan for 18 years, the total amount contributed will be $21,600. If the average annual return is 5%, your total savings with interest would be $35,400.

A 529 also comes with tax incentives. The money you earn as interest is tax-free, as well as any funds you withdraw for the beneficiary’s educational expenses. Additionally, these accounts are designed for anyone who wants to attend college. Adults who wish to return to school can open these accounts, name themselves as the beneficiary, and use the interest-bearing funds for their tuition.

Budget As You Go

College learning tracks vary for each individual. There’s always the option of taking one to two classes per semester instead of a full load of four or more. Students may opt to complete their degrees over a more extended period for various reasons, such as needing to work full-time or having children. Saving up for classes as you take them comes with some upsides, such as being able to focus more intently on coursework.

“If you’re working during college, you’re gaining important work skills that will be valued by future employers,” says Daniel Douglas, director of social science research at Trinity College in Connecticut. “You know about showing up on time, following directions given by a supervisor, and being generally diligent in your duties.”

Whether you’re a high school student or an adult who wants to attend college, begin to calculate how much money and time coursework will cost you. For example, if you still have to juggle a full-time job, then you need to be realistic about when you’ll attend classes and study. Time needs to be part of your budget, too.

When to Consider a Loan

There is no shame in considering a student loan once you’ve exhausted every other payment option. This is especially true if you have a high return on investment, meaning you’re earning a degree that will help you obtain a high-earning career. If you’re considering a loan, start with Federal Student Loans, which offer several built-in protections.

The cost of tuition shouldn’t deter anyone from pursuing their dreams. By doing research and conferring with counselors, you can come up with a plan to pay for college, even if that means getting creative. With Insureyouknow.org, you may store all of your research, financial planning, and school records in one place, making it easier for you to review and stay focused on your goals.

How to Prepare for College Living: A Survival Guide for Incoming Students

February 15, 2025

Congratulations! You’ve been accepted into college, and soon, you’ll embark on one of the most exciting adventures of your life, along with 16 million others. But before you start dreaming about campus life, late-night study sessions, and newfound independence, there are some practical steps to ensure a smooth transition. From dorm essentials to financial planning, this guide will help you prepare for college living.

1. Master the Art of Budgeting

Living on your own means managing your finances wisely. Here’s how to stay on top of your budget:

- Create a Budget: Track your expenses, including tuition, rent, food, transportation, and entertainment.

- Use Budgeting Apps: Apps like Mint, YNAB, or PocketGuard can help you stay organized.

- Open a Student Bank Account: Many banks offer students accounts with low or no fees.

- Look for Discounts: Your student ID is your best friend—use it for travel, entertainment, and shopping discounts.

2. Pack Smart: The College Essentials Checklist

You don’t want to arrive at college and realize you forgot something crucial. Here’s what to bring:

- Dorm Room Must-Haves:

- Bedding (twin XL sheets, comforter, pillows)

- Storage bins and organizers

- Desk lamp and power strips

- Laundry hamper and detergent

- Shower caddy and flip-flops

- Tech Gear:

- Laptop and chargers

- Noise-canceling headphones

- Portable hard drive or cloud storage subscription

- Kitchen Supplies:

- Mini fridge (if allowed)

- Microwave or coffee maker

- Reusable water bottles and utensils

- Emergency Kit:

- First aid supplies

- Medications

- Flashlight and extra batteries

3. Set Up Your Health & Insurance Plan

Make sure you have a solid plan in place for medical needs:

- Health Insurance: Check if you’re covered under your parent’s plan or if your college offers coverage.

- Locate Healthcare Providers: Know where the nearest doctor, dentist, and urgent care clinic are.

- Stock Up on Essentials: Pack prescription medications, vitamins, and a basic first-aid kit.

4. Learn Basic Life Skills

College is a time to gain independence, so mastering basic skills will help you thrive:

- Cooking Basics: Learn how to make simple meals to save money and eat healthier.

- Laundry 101: Know how to separate colors, use detergent, and read washing machine settings.

- Time Management: College life is busy—use planners or apps to manage assignments and social activities.

5. Prepare for Roommate Life

Sharing a living space can be a challenge, but good communication helps:

- Set Boundaries Early: Discuss sleep schedules, cleaning duties, and guest policies.

- Be Respectful: Small gestures, like cleaning up after yourself, go a long way.

- Resolve Conflicts Maturely: Address issues directly and respectfully to maintain a positive environment.

6. Get to Know Campus Resources

Colleges offer plenty of support services—take advantage of them!

- Academic Support: Visit tutoring centers and writing labs.

- Mental Health Services: Many colleges offer free or low-cost counseling.

- Career Services: Start networking and building your resume early.

- Student Organizations: Join clubs to meet new friends and enhance your college experience.

College is a time of growth, challenges, and unforgettable experiences. By planning ahead, you can make the transition smoother and set yourself up for success. Embrace the adventure, stay organized, and don’t hesitate to ask for help when needed. You’ve got this!

InsureYouKnow.org

College graduation prompts transitioning from a school-based existence to one replete with adult responsibilities. By preparing for the unforeseen future, college grads who do their homework and keep their records at insureyouknow.org, can begin living their lives to the fullest.

2024 Changes that Would Impact Your Retirement Finances

April 1, 2024

Changes to retirement regulations are making 2024 out to be the perfect time to reexamine your retirement planning and make sure you’re getting the most out of your savings.

“The rules are constantly changing,” says director of Personal Retirement Product Management at Bank of America Debra Greenberg. “It’s always a good idea to familiarize yourself with what’s new to see whether it makes sense to take advantage of it.”

Here’s what you should know about several changes to retirement regulations in 2024.

It Pays to Plan for Retirement

While the changes to retirement regulations may seem small, Americans need all the help they can get right now. According to the National Council on Aging, up to 80% of older adults are at risk of dealing with economic insecurity as they age, while half of all Americans report being behind on their retirement savings goals.

“The IRS adjusts many things each year to reflect cost of living and inflation,” says Jackson Hewitt’s chief tax information officer Mark Steber. “It happens each year and taxpayers shouldn’t be alarmed — they might even have a bigger benefit.” Since retirement contributions are pre-tax, saving for retirement actually lowers your taxable income, which may even place you into a lower tax bracket. Plus, you may even be eligible for a tax credit of up to 50% of what you put into your retirement accounts.

Contribution Limits Will Increase

The contribution limits for a traditional or Roth IRA are increasing in 2024. The limit on annual contributions to an IRA will go up to $7,000, up from $6,500 last year.

Individuals will be able to contribute more to their 401(k) and employer-based plans as well. For those who have a 401(k), 403(b), most 457 plans, or the federal government’s Thrift Savings Plan, the contribution limit is increasing to $23,000 in 2024, which is $500 more than last year. Those who are 50 and older, can contribute up to $30,500 into the same accounts.

Starter 401k Plans are Possible

In 2024, employers who don’t sponsor a retirement plan may offer a Starter 401(k) deferral-only arrangement. A starter 401(k) is a simplified employer-sponsored retirement plan with lower saving limits than a standard 401(k). Employers are not allowed to make contributions, and employee auto-enrollment is required. In 2024, the annual contribution limit to this plan will be $6,000. Beginning this year, employees with certain qualifiable emergencies may also make penalty-free withdrawals from their 401(k) of up to $1,000, though they would still have to pay the income tax on those withdrawals.

529 Plans Can Now be Converted Into Roths

For parents who will no longer need their 529 funds for their children, the Secure 2.0 Act will allow for a portion of the 529 to be rolled into a Roth IRA. Beginning January 1st, the funds can either be used for educational expenses or put toward retirement, as a Roth IRA rollover. You may rollover up to $35,000, free of income tax or any tax penalties. The only limitations are that the 529 must have been in place for at least 15 years, and certain states may not allow the rollover.

Changes to Social Security and RMDs

In January, Social Security checks will increase by 3.2% due to the latest COLA, or cost-of-living adjustment. On average, Social Security monthly benefits will increase by $59 a month, from $1,848 to $1,907. Those who receive survivors or spousal benefits will receive even more.

For 2024, the maximum benefit for a worker who claims Social Security at FRA (Full Retirement Age)is $3,822 a month, which is up from $3,627 in 2023. For 2024, the FRA is 66 years and 6 months for those born in 1957 and 66 years and 8 months for those born in 1958. That means that anyone born between July 2, 1957 through May 1, 1958 will reach FRA in 2024.

The IRS uses a calculation based on the amount in your retirement account and your life expectancy to determine the minimum amount you are required to take out each year, known as RMDs (required minimum distributions). Secure 2.0 increased the age for starting RMDs from 72 to 73, effective in 2023. If you are subject to RMDs, then you must make your withdrawal by the end of this year or by April 1st next year if it’s your first year being eligible. So if you turn 73 in 2024, you’ll have until April 1, 2025 to make your first RMD.

Anyone receiving more Social Security but paying Medicare premiums may not feel much of a difference in their increased Social Security benefits since standard Medicare Part B premiums are rising by 6%. As many participants have their Medicare premium deducted right from their Social Security payment, the $9.80 increase will take a portion of the average $59 benefit increase. The annual deductible will also increase this year from $226 to $240.

Insureyouknow.org It will always be important to review your retirement savings every year, but this is becoming even more important to do in the face of rising costs and changing regulations. With Insureyouknow.org, storing all of your financial information in one easy-to-review place can help you ensure that you are still on track to meet your retirement goals at the start of each annual review.

How 2024 Inflation Adjustment Will Affect Your Paycheck

March 15, 2024

This year may come with slightly larger paydays for some Americans. This is because of the new changes to taxable income and deductions that the IRS has put in place in order to help taxpayers with inflation. With the cost of living increasing without wages and salaries doing the same, the new tax adjustments are meant to help consumers deal with higher prices.

As federal income tax brackets are adjusted by 5.4% this year, the change could result in a small paycheck bump, depending on what your withholding is. Since the consumer price index only declined by .1% in November 2023, many Americans are struggling financially.

Here’s everything you need to know about the 2024 tax changes that might affect your bottom line.

Decoding Tax Bracket Creep

The new IRS tax brackets and increased standard deductions have been in effect since January 1st. These adjustments will apply to your next tax return in 2025. It’s standard for the IRS to make changes every year to account for inflation. This is done to help people with the rising costs of living and prevent “bracket creep,” which happens when inflation forces people into a higher income tax bracket without their real income having increased.

So even if you make more money this year, these changes may keep you from falling into a higher tax bracket. You may even find that you have fallen into a lower tax bracket and see an increase in your take-home pay. This becomes even more likely if your pay has stayed the same as in the previous year. For example, if you made $45,000 last year, you would have been in the 22% tax bracket. In 2024, the same $45,000 income places you in the 12% bracket, which means you’ll owe less federal taxes and have less money withdrawn from your checks.

Choose Your Deduction and Know Your Taxable Income

The federal income tax bracket that you fall into determines how much you’ll pay in taxes for the year. Your tax bracket excludes the standard deductions or any itemized tax deductions. Most people with simple taxes claim the standard deduction, which reduces their taxable income. If you receive wages from only one job and receive a W-2, then the standard deduction is usually the best way to maximize your tax refund. But if you are self-employed or have specific deductions you want to claim, then you may elect to itemize your deductions instead.

Once you calculate your taxable income by subtracting either the standard or itemized deductions from your adjusted gross income, then you’ll know which bracket you fall into and how much income tax you should owe. “You always want to keep a running total in your mind of how your income is changing,” says certified financial planner Roger Stinnett. “Because it’s complex.”

2024 Tax Brackets and Standard Deductions

For the 2024 tax year, both the federal income tax brackets and the standard deduction were raised. These amounts will apply to your 2024 taxes, which you won’t file until 2025.

For those married filing jointly with a combined income between $23, 201 and $94,300, the estimated taxes owed would be $2,320. For a single taxpayer with an income between $11,601 and $47,150, they would owe $1,160, plus ten percent of any amount over $11,600.

The standard tax deduction for 2024 for those who file single will be $14,600, which is a $750 increase from 2023. For those married and filing together, the standard deduction will be $29,200, which is a $1,500 increase from last year.

Watch Your Withholdings

The federal and state withholdings on your paycheck will determine whether or not you’ll owe taxes at the end of the year or receive a refund from overpaying throughout the year. Regardless of your changes to your income, you may be placed in a lower or higher tax bracket because of the new adjustments.

It will be important to keep track of any life changes that may affect your filing situation, such as marriage, divorce, the birth or adoption of a child, retirement, buying a home, having to file for bankruptcy, and more. If you know your situation has changed since the previous year, it will be important to adjust your withholding by filing a new W-4 with your employer. If you had a large refund or owed a large amount last year, then this is a sign to check your withholding.

Other 2024 Tax Changes to Know

The IRS also announced higher contribution limits for tax-deferred retirement plans for the 2024 tax year. Americans may now contribute up to $23,000 into their 401(k), 403(b) and most 457 plans, which is $500 more than in 2023. The limit on annual IRA contributions also increases to $7,000, up from $6,500 the previous year. For those that save for added healthcare costs, the FSA contribution limit has also increased to $3,200, which is up from $3,050 for 2023. And if you collect Social Security, then you’ll receive a 3.2% cost-of-living adjustment in 2024.

The purpose of these tax changes is to help taxpayers feel the pain of inflation less. If you’ve noticed a higher paycheck, then different withholdings may be why. Figuring out whether or not you’ll be falling into a different tax bracket this year will help you determine if you’ll be benefiting from the new changes. Insureyouknow.org can help you store all of your financial information and tax preparation documents so that when it comes time to file, the process will be as painless as paying less taxes in 2025.

How to Cut Down on the Cost of Owning a Car

February 15, 2024

In 2023, the average cost of owning a new car was $12,182 a year or $121 a month according to AAA. In addition to car payments, insurance, and maintenance costs, the price of gas is $5 a gallon,, which means that most U.S. households will spend $2,750 on gas per year. “If you are living paycheck to paycheck, it could put you over the edge,” says Ivan Drury, senior manager for Edmunds.com, a car shopping site. “But even if you are not, it’s very emotional. It’s in your face twice a week.”

The good news is that by cutting your expenses in other areas, such as with car insurance, you can save money and make up for the added charges at the pump. Besides simply driving less, which isn’t an option for many people, here are a few ways to make car ownership more affordable.

1. Shop Around For Car Insurance

According to J.D. Power, only 1 in 7 drivers changed auto insurers last year, but shopping around for lower premiums could save you a lot of money. In addition to your location and the type of car you own, other factors affect your rates, including your age and credit score. If you’ve improved your score within the last year, this one factor may lower your car insurance bill.

You can collect quotes through an insurance agent or use an online search engine, such as Experian, who claims to have saved drivers an average of $961 a year or $80 a month in 2021. Calling around or doing a quick search takes only fifteen minutes and could shave a lot of money off of your premium.

2. Check For Discounts and Adjust Your Existing Policy

Your existing carrier may offer discounts you don’t even know about, such as for paying your bill online and in advance. According to Zebra, paying your bill early online saves the average customer $170 a year. Bundling insurance policies, such as combining your homeowners and auto insurance, is another way insurance companies incentivize their policies through discounted rates.

There are usually three types of coverage on any given insurance policy, including liability, collision, and comprehensive. While most states require drivers to carry some amount of liability coverage, eliminating collision and comprehensive coverage could save you up to $900 a year. You may also opt to lower your car insurance premium by raising your deductible from $500 to $1,000. This makes sense if you don’t have a new or expensive car and can afford to pay the deductible if anything were to happen.

3. Outside Financing And Refinancing

One of the smartest ways to avoid high interest rates on a car payment is by securing outside financing. Compared to what the dealership will offer you, this can save you a ton of money in interest alone. Your local bank or credit union can help you shop around for the best offer. If you already have a monthly car payment, the next best thing to do is to look into refinancing your loan. Drivers who benefit the most from refinancing are those who have improved their credit score since initially securing their loan.

Of course if you can purchase a car outright, avoiding any kind of financing is always the very best option. If it’s possible for you to stick to a budget and save up, you may even be able to negotiate a better deal on the purchase price of your desired vehicle. Forty percent of the cost of owning a car is actually depreciation, which can equal more than $3,000 annually. That means that buying a gently used car is a great deal, without the rapid decline in value.

4. Sell One of Your Cars or Trade it Out

If you have a luxury or oversized vehicle, then trading your vehicle or a more practical car is always an option. Once you have a simpler car, you’ll save money on gas, insurance, and even maintenance costs. “Less fancy cars are more reliable,” says editor of Autotrader Brian Moody. “They have fewer gadgets.”

If your family has more than one car, then you may be able to sell one of them and end up saving a lot of money every month. Many families find that they adjust to sharing a vehicle, and when you need your own car for some reason, using Uber or Lyft periodically may still cost less than owning a vehicle.

5. Save on Gas

Nearly twenty percent of the cost of car ownership comes from fuelling up. Unless your vehicle requires premium fuel, save by filling up with regular gas. You may also choose to slow down as gas mileage increases at lower speeds. If you can, try driving less, such as by walking to close destinations or starting a carpool for work. If you are able to get your annual mileage below 7,500, then your insurance company might even give you a discount on your coverage for that too.

6. Save up for Maintenance

The cost of vehicle maintenance is equal to fourteen percent of the total cost of owning a car. By keeping up on routine maintenance and using synthetic oil, you will avoid more expensive issues down the road. When a large repair does arise, always call around to get quotes and go with the best deal. Since emergencies happen, setting up a sinking fund for unplanned car expenses is always a good idea. By putting away only $83 a month, you’ll save up $1,000 a year, which could be used for an unforeseen mechanic bill. “You could set aside money every week,” suggests Lauren Fix of Car Smarts. “Then the money will be available rather than using a credit card at a high interest rate.”

The less money you spend on your car, the more you’ll have for other expenses in your life, from groceries to vacations. With Insureyouknow.org, you can store all of your vehicle and financial records in one place. That way when it’s time to refinance, shop around for better insurance, or sell your car, everything you need will already be at your fingertips. There’s never a good reason to throw away your hard-earned money on unnecessary expenses.

Do You Realize How “Precious” a Child Is?

September 15, 2022

The cost of raising a child through high school has risen to $310,605 because of inflation that is running close to a four-decade high, according to an estimate by the Brookings Institution, a nonprofit public policy organization based in Washington, DC.

In 2017—years before the pandemic and during an extended period of very low inflation—the U.S. Department of Agriculture (USDA) projected that the average total expenditures spent on a child from birth through age 17 would be $284,594. This estimate assumed an average inflation rate of 2.2 percent and did not include the expenses associated with sending a child to college or supporting them during their transition to adulthood. Since 2020, the inflation rate has skyrocketed— 8.5 percent as of July 2022—partly due to supply-chain issues and stimulus spending packages that put more cash into Americans’ pockets. The Federal Reserve has now raised interest rates substantially to control inflation.

The multiyear total is up $26,011, or more than 9 percent, from a calculation based on the inflation rate two years ago, before rapid price increases hit the economy, reports the Brookings Institution.

The new estimate crunches numbers for middle-income, married parents, and doesn’t include projections for single-parent households, or consider how race factors into cost challenges.

Expenses

The estimate covers a range of expenses, including housing, education, food, clothing, healthcare, and childcare, and accounts for childhood milestones and activities—baby essentials, haircuts, sports equipment, extracurricular activities, and car insurance starting in the teen years, among other costs.

In 2019, the typical expenses to raise a child were estimated by the USDA as follows:

- Housing: 29%

- Food: 18%

- Childcare and Education: 16%

- Transportation: 15%

- Healthcare: 9%

- Miscellaneous (included Personal Care and Entertainment): 7%

- Clothing: 6%

Housing

Housing at 29 percent is the most significant expense associated with raising a child. The cost and type of housing vary widely by location. Other variables include mortgage or rent payments, property tax, home repairs and maintenance, insurance, utilities, and other miscellaneous housing costs.

Food

The cost of food is the second-largest expense, at 18 percent of the overall cost of raising a child. Over time, food prices have trended up, with food-at-home pricing increasing 12.1 percent and food-away-from-home pricing increasing by 7.7 percent from June 2021 to July 2022. The USDA expects rising costs for 2022, with increases as high as 10 percent and 7.5 percent, respectively.

Childcare and Education

Childcare and education expenses in 2019 accounted for 16 percent of the cost of raising a child, and it continues to increase.

The widespread acceptance by employers of remote work and letting employees work from home part or full-time has eased the burden of childcare costs for many families, cutting the cost by as much as 30 percent for some workers.

Education is a major expense when it comes to raising children. When it comes to kindergarten through high school, parents can choose between public and private schools. For private schools, the Education Data Initiative estimated that tuition costs an average of $12,350 per year. Associated costs, like technology, textbooks, and back-to-school supplies, could bring that up to $16,050. For a child to be in private school from kindergarten through eighth grade, the estimated cost could be about $208,650. Additional expenses for extracurricular activities such as sports, the arts—music, theater, and yearbook—and other clubs also add up and are accompanied by fees for participation, equipment, and travel, which have also increased due to inflation.

Healthcare

The total cost of a health plan is set according to the number of people covered by it, as well as each person’s age and possibly their tobacco use. For example, a family of three, with two adults and a child, would pay a much higher monthly health insurance premium than an individual.

Strategies

Raising children is rewarding and fulfilling to many people. But it’s also become very expensive. By preparing mentally and implementing financial planning strategies, you can be well-equipped to raise your child to adulthood comfortably, even on a budget.

InsureYouKnow.org

If you are a parent, you are responsible for raising your child and providing food, clothing, shelter, and security. Consider getting insurance coverage—including life, short- and long-term disability, and health insurance to avoid putting your family at risk financially in the event of unexpected hardship. To cope with the rising costs of raising children, live within your means, save money wherever possible, and shop around for home and auto insurance each year for the best deals. At insureyouknow.org, you can track your expenses to raise a child and file insurance policies that cover your family’s financial and healthcare needs.

Sticker Shock in the Grocery Aisles

July 31, 2022

Unless you go out to eat or get take-out for every meal you consume, you can’t avoid buying groceries—even if you have them delivered to your doorstep. With inflation at the highest rate it has been in 40 years, you’ve surely noticed that prices continue to rise in the grocery aisles.

If you want to stabilize your grocery bill and make your budget go further in your fight against price inflation, try some of the following money-saving strategies when you face your next grocery trip or delivery.

Check Your Pantry and Freezer

Before you go grocery shopping, check the shelves of your pantry and freezer. By taking inventory of what you already have at home, you’ll avoid buying multiples of the same item. You might be able to shorten your grocery list and spend less.

Choose Store Brands Over Name Brands

Name brand groceries are usually priced higher than their store brand counterparts. Many times, you might not be able to tell the difference between the two. With prices going up, switch to generic brands to lower your grocery spending.

Buy in Bulk

While you’ll pay more money upfront for groceries in larger quantities, it’s a smart move to buy in bulk. Typically, you’ll pay less per item and you’ll have staples on hand that may allow you to do less grocery shopping throughout the month.

Cut Back on Meat

Cutting back on meat will have a significant impact on your grocery bill because beef, pork, and chicken tend to be some of the more expensive items in your shopping cart— inflation or not. Going meatless a day or two a week and turning to cheaper alternatives, like beans and lentils, can help you cut costs.

Plan Meals

Planning your meals and making grocery lists based on a meal plan will prompt you to be less likely to waste money on something that looks appealing in the store, but you might not need for the family meals and snacks you prepare at home.

Consider Substitutions

Using substitute items can result in cost savings without sacrificing the quality or taste of the meal. For example, fruits and vegetables that are not in season tend to be more expensive. Using different produce in meals than a recipe calls for may enhance and not compromise a recipe.

Minimize Food Waste

Reduce food waste by making a grocery list and sticking to it; buy frozen instead of fresh; rethink sell-by dates if food still looks and smells fresh; freeze meats, bread, and vegetables that you aren’t going to use immediately.

Store Items Where You Can See Them

Keep items where you can see them, and you’ll be more likely to use them. An organized refrigerator and a neatly arranged pantry can help you quickly find and use items.

Learn to Preserve or Can Foods

You can pickle, preserve, or can foods—all options gaining popularity. These practices have been around for centuries and have helped folks survive harsh winters and economic downturns. With a little upfront investment of time and money, you can acquire the tools necessary to preserve seasonal foods. This can prolong their shelf life and reduce food waste and costs.

Sign Up for Loyalty Programs

Most grocery stores offer loyalty programs that are free to join. You can benefit from discounts that automatically get applied to your cart at checkout or you can get access to exclusive coupons on their apps.

Getting free items, including food offerings, from a local Buy Nothing Group means you can bypass high prices at a store—and you don’t even have to offer up anything in exchange. These groups focus on sharing rather than trading or bartering within a designated area. Join your local Buy Nothing Group on Facebook.

InsureYouKnow.org

Shopping for SHOP Coverage

May 15, 2022

Signed into law in 2010, the Affordable Care Act changed many regulations affecting small businesses and insurance. The law established the Small Business Health Options Program (SHOP) for small employers —generally those with 1–50 employees—who want to provide health and dental coverage to their employees affordably, flexibly, and conveniently.

Qualifications to provide SHOP coverage

Find out on the HealthCare.gov website if your business or non-profit organization qualifies for SHOP by meeting the following four requirements:

1. You have 1-50 full-time equivalent employees (FTEs)

- Use the FTE Calculator to see if you qualify. Note: To qualify for SHOP, you must have at least one FTE employee other than owners, spouses, and family members of owners and partners.

2. You offer coverage to all full-time employees—generally, workers averaging 30 or more hours per week

- You don’t have to offer coverage to part-time employees—those averaging fewer than 30 hours per week—or seasonal workers.

3. You enroll at least 70 percent of the employees to whom you offer insurance

- Employees with other health coverage aren’t counted as rejecting your offer.

- Use the SHOP Minimum Participation Rate Calculator to see how many of your employees must accept.

- Some states have different minimum participation requirements. See if this affects you.

- If you don’t meet your minimum participation requirement, you can enroll between November 15-December 15 any year. During this time, the participation requirement isn’t enforced.

4. You have an office or employee work site within the state whose SHOP you want to use

- Visit this page, select your state, and see how to access SHOP insurance in your state.

- See what to do if your business operates in multiple states.

- If eligible, you don’t have to wait for an open enrollment period. You can start offering SHOP coverage to your employees any time of year.

Reasons to offer SHOP coverage

- SHOP insurance gives you choice and flexibility to:

- Offer your employees one plan or let them choose from multiple plans.

- Offer only health coverage, only dental coverage, or both.

- Choose how much you pay toward your employees’ premiums and whether to offer coverage to their dependents.

- Decide how long new employees must wait before enrolling.

- You can get the information you need in one location. You can make an informed decision about your SHOP insurance options with the tools at HealthCare.gov where you can compare plans and prices and find out if you qualify for SHOP.

- You can use your current SHOP-registered agent or broker or find an agent or broker in your area to help you enroll in coverage.

- You may be able to get the Small Business Health Care Tax Credit. Enrolling in SHOP insurance is generally the only way for eligible small employers to take advantage of the Small Business Health Care Tax Credit. You may qualify if you have fewer than 25 FTE employees making an average of about $56,000 or less. See how much your business could save. Updated IRC guidelines for small business health care tax credit and the SHOP marketplace can inform you if you are a small employer.

InsureYouKnow.org

Whether you are an employer or an employee in a small business, you may find it helpful to review SHOP coverage how-to guides, fact sheets, tools, and other resources. After making SHOP health insurance decisions, you can keep your records about the best plan for you and its costs, benefits, and features at insureyouknow.org.

Medicare Enrollment: Open Until December 7

October 28, 2021

Medicare is a national health insurance program administered by the federal government for people 65 or older. You’re first eligible to sign up for Medicare three months before you turn 65. You may be eligible to get Medicare earlier if you have a disability, End-Stage Renal Disease (ESRD), or Amyotrophic lateral sclerosis (ALS)—also known as Lou Gehrig’s disease.

From October 15 through December 7 every year, depending on your circumstances, you are allowed to enroll in or switch to another Medicare Advantage plan or Medicare Part D prescription drug plan, or to drop your plan and return to Original Medicare. View a complete list of Medicare enrollment dates.

If you qualify for Medicare coverage or know someone who may need your help to learn about Medicare, coverage options, and how to apply, keep reading for a quick course in Medicare Basics.

Medicare Basics

Medicare and Medicare-approved private insurance companies offer the following options for you to get health care coverage:

- Part A (Hospital Insurance): Helps cover inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care.

- Part B (Medical Insurance): Helps cover:

- Services from doctors and other health care providers

- Outpatient care

- Home health care

- Durable medical equipment (like wheelchairs, walkers, hospital beds, and other equipment)

- Many preventive services (like screenings, shots, or vaccines, and yearly “wellness” visits)

- Part C (Medicare Advantage): Medicare-approved private insurance companies that provide all Part A and Part B services and may provide prescription drug coverage and other supplemental benefits.

- Part D (Prescription Drug Coverage): Medicare-approved private insurance companies that provide outpatient prescription drug coverage.

- Medicare Supplemental Insurance (Medigap): Extra insurance you can buy from a private company that helps pay your share of costs in Original Medicare. Policies are standardized, and in most states named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, no matter which insurance company sells it.

- You need both Part A and Part B to buy a Medigap policy.

- Some Medigap policies offer coverage when you travel outside the United States.

- Generally, Medigap policies don’t cover long-term care (like care in a nursing home), vision, dental, hearing aids, private-duty nursing, or prescription drugs.

- If you’re under 65, you might not be able to buy a Medigap policy, or you may have to pay more.

- Medigap policies are standardized, and in most states named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, no matter which insurance company sells it.

- Find a Medigap policy that works for you.

Medicare Options

When you first sign up for Medicare and during open enrollment periods, you can choose one of the following two ways to get your Medicare coverage.

- Original Medicare (Includes Part A and Part B)

- With Original Medicare, you can go to any doctor or hospital that takes Medicare, anywhere in the United States. Find providers that work with Medicare.

- Join a separate Medicare drug plan (Part D) to get drug coverage. If you choose Original Medicare and want to add drug coverage, you can join a separate Medicare drug plan. Medicare drug coverage is optional. It’s available to everyone with Medicare.

- If you have other insurance you also may have other coverage, like employer or union, military, or veterans’ benefits, learn how Original Medicare works with your other coverage.

- Medicare Advantage (Part C)

- Medicare Advantage is a Medicare-approved plan from a private company that offers an alternative to Original Medicare for your health and drug coverage. These “bundled” plans include Part A, Part B, and usually Part D.

- In most cases, you’ll need to use doctors who are in the plan’s network.

- Plans may have lower out-of-pocket costs than Original Medicare.

- Plans may offer some extra benefits that Original Medicare doesn’t cover—like vision, hearing, and dental services.

- Most Medicare Advantage Plans include Part D coverage.

- Below are the most common types of Medicare Advantage Plans:

- Health Maintenance Organization (HMO) Plans

- Preferred Provider Organization (PPO) PlansPrivate Fee-for-Service (PFFS) PlansSpecial Needs Plans (SNPs)

- Find a Medicare Advantage Plan for 2022.

Medicare Costs

Generally, you pay a monthly premium for Medicare coverage and part of the costs each time you get a covered service. There’s no yearly limit on what you pay out-of-pocket, unless you have supplemental coverage, like a Medicare Supplement Insurance. Get Medicare costs for current premium rates.

Health Insurance Assistance

Contact your local State Health Insurance Assistance Program (SHIP) to get free personalized health insurance counseling. SHIPs aren’t connected to any insurance company or health plan.

Sign Up Process

When you’re ready, contact Social Security to sign up for Medicare coverage:

- Apply online (at Social Security): This is the easiest and fastest way to sign up and get any financial help you may need. You’ll need to create your secure my Social Security account to sign up for Medicare or apply for Social Security benefits online.

- Call 1-800-772-1213. TTY users can call 1-800-325-0778.

- Contact your local Social Security office.

- If you or your spouse worked for a railroad, call the Railroad Retirement Board at 1-877-772-5772.

Note: Medicare provides your coverage, but you’ll sign up through Social Security (or the Railroad Retirement Board) because they need to see if you’re eligible for Medicare, including whether you (or another qualifying person) paid Medicare taxes long enough to get Part A without having to pay a monthly premium. They also process requests to sign up for Part B for Medicare.

InsureYouKnow.org

After you’ve met all the requirements to apply for Medicare coverage, have made your choices, and have signed up online, keep track of your decisions and copies of your Medicare, Medigap, and Medicare Advantage Plan membership information at insureyouknow.org.