Tag: Personal Finance

2026 Student Loan Defaults: Secure Your Financial Records

March 6, 2026

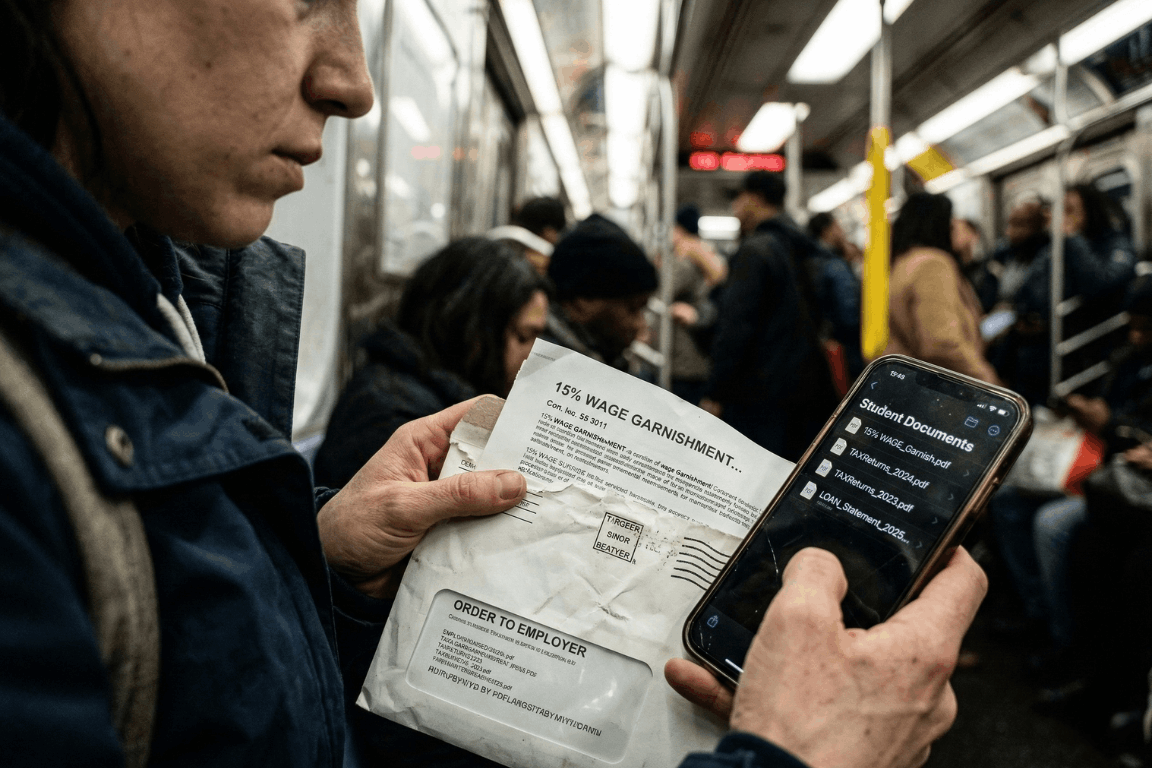

A massive financial wall hit millions of Americans earlier this year. Pandemic payment pauses are officially ancient history. The temporary relief programs dried up entirely. After months of messy court battles regarding income-driven repayment plans, the federal government decided to bring back its heaviest collection tools. Starting in early 2026, the U.S. Department of Education began sending administrative wage garnishment letters to defaulted borrowers. The numbers from major credit bureaus, like Experian, look pretty grim. The entire country is watching a massive wave of loan delinquencies happen in real time. People are suddenly staring down severe financial penalties. Getting through this economic squeeze requires a lot more than just reading news updates. It demands immediate, highly organized access to specific financial paperwork.

The 2026 Student Loan Landscape: A Shocking New Data Trend

So, who is actually defaulting right now? Historically, student loan defaults mostly hammered sub-prime borrowers. That whole narrative flipped completely upside down in 2026. Recent reports from credit bureaus reveal something entirely unexpected. Nearly a quarter of newly defaulted borrowers belong in the “prime” credit tier or even higher. These are the exact demographics the financial industry usually views as incredibly stable.

With over 5 million borrowers currently sitting in default status, and millions more falling behind every month, the economic pain is obvious. Borrowers are stuck navigating a bizarre maze of constantly changing payment plans. Making things worse, millions of accounts got bounced around between different private servicing companies over the last two years. Monthly payments got lost in the mail. Crucial paperwork simply vanished. Hold times to speak with basic customer service stretched into hours. Once a federal student loan reaches 270 days past due, it hits official default status. At that specific moment, the government gets to use an administrative superpower that regular credit card companies cannot even touch. They can literally take wages without ever stepping foot inside a courtroom.

Understanding Administrative Wage Garnishment: The 15% Reality

The fallout from a federal default happens fast. Through a process called Administrative Wage Garnishment (AWG), the Department of Education can legally force an employer to pull up to 15% of a borrower’s disposable pay. Disposable pay simply means the cash remaining after legally required deductions, like federal and state taxes, come out of the check.

Federal law does leave a very small safety net in place. Borrowers get to keep a weekly take-home amount equal to at least 30 times the federal minimum wage. But for anyone living from one paycheck to the next, suddenly losing 15% of their income is pure disaster. It usually means missing the rent, skipping the grocery store, or defaulting on other credit cards. Before the garnishment actually kicks in, the government must send a 30-day advance written warning. That specific 30-day window is basically everything. It acts as the only real timeframe a borrower gets to object or set up a different payment plan before their paycheck actually shrinks.

How to Stop Garnishment: The Heavy Burden of Proof

Borrowers holding a garnishment notice still carry some legal rights. During those 30 days, individuals can officially demand a hearing to stop the withholding order. They might attempt to prove extreme financial hardship. Or, they could try applying for federal loan rehabilitation. Rehabilitation usually involves agreeing to make nine on-time payments over a 10-month window to get the loan back on track.

Another route involves submitting a formal financial hardship appeal. Winning this appeal means legally proving that a 15% pay cut makes buying basic survival items impossible. The government looks at documented living expenses and compares them against very strict IRS Allowable Living Expense guidelines. If a family spends more on food or housing than the IRS thinks is necessary for that specific family size, the extra amount gets totally ignored. Proving hardship is notoriously difficult. Using these rights is never a walk in the park. It requires gathering highly specific legal and financial records immediately. In these types of administrative hearings, the burden of proof lands squarely on the borrower.

The Critical Role of Organized Financial Documents

Sloppy paperwork turns a bad money situation into an absolute nightmare. When the garnishment letter shows up, the clock ticks fast. Spending hours digging through cluttered email inboxes for old messages from loan servicers wastes valuable time. Tearing up the living room looking for utility bills to prove basic living expenses just fuels the anxiety. If a borrower fails to hand over the correct evidence within 30 days, their employer receives the order. The garnishment starts.

This explains exactly why relying on a secure, independent electronic safe deposit box changes the playing field. Keeping a dedicated digital vault for vital life information ensures nobody gets blindsided by aggressive debt collectors. Storing all important financial, legal, and contractual documents in one simple location gives borrowers a huge advantage. They can instantly grab the exact proof they need to protect their paychecks and negotiate with default resolution teams.

Essential Documents to Secure in a Digital Vault

To build a strong defense against a default warning, individuals should make sure the following documents are digitized, safely uploaded, and ready for action:

- Original Loan Agreements and Master Promissory Notes: Finding original contracts immediately helps verify the true debt amount. It also spots accounting errors and confirms which company actually owns the loan today.

- Complete Tax Returns: Proving financial hardship or enrolling in an income-driven repayment plan means submitting paperwork. The Department of Education demands recent federal and state tax returns before they even start talking.

- Official Pay Stubs: Current pay stubs are absolutely required to figure out actual disposable income. They also help verify that any proposed wage garnishment does not illegally drop below the minimum wage protection limit.

- Household Expense Records: Tracking basic living costs is a strict requirement for hardship appeals. Think about rent agreements, mortgage papers, utility bills, health insurance premiums, and pharmacy receipts. These papers help prove that living expenses are reasonable and fit within tight IRS standards.

- Correspondence with Loan Servicers: A strong paper trail of older payments, approved forbearances, and emails with the loan servicers can literally save the day. This proof is extremely important if someone needs to show a loan was wrongfully thrown into default in the first place.

The Absolute Security of Zero-Knowledge Storage

Privacy is absolutely non-negotiable when dealing with highly sensitive financial details. Relying on physical metal filing cabinets leaves people wide open to lost papers, house fires, or basic theft. Depending on regular, unencrypted email folders or a messy computer desktop basically hands sensitive financial data directly to hackers. Cybercriminals routinely target email servers specifically to find W-2 forms and tax returns. Once they grab those files, identity theft is pretty much guaranteed.

Using a specialized platform built with heavy-duty cloud encryption makes sure financial data stays completely private. The absolute best platforms run on Amazon cloud encryption mixed with a “zero-knowledge” setup. In a zero-knowledge system, only the actual account owner knows the password. The site administrators never get to see it. That means absolutely nobody else can ever gain access, view the files, or mine the stored documents to sell the data.

Strategic Document Sharing with Trusted Partners

Fixing a defaulted student loan is almost never a solo job. Borrowers usually need to bring in certified financial planners, tax accountants, or specialized student loan lawyers to help decode the messy federal rules.

Advanced secure portals allow individuals to selectively share specific document folders with these exact trusted partners. Sending unencrypted PDFs of tax returns and pay stubs back and forth through regular email is a massive cybersecurity hazard. Instead, account holders can simply give a legal advisor temporary, secure access to the required files right inside the encrypted vault. This targeted sharing feature speeds up the whole default resolution process, keeps communication secure, and leaves the rest of the vault totally locked down. Setting up automatic monthly reminders inside the portal also helps users routinely update their financial snapshots, keeping their defense strategy completely fresh.

Facing economic uncertainty requires a solid game plan. The return of federal student loan wage garnishments in 2026 creates a massive hurdle. Credit bureau data clearly shows that financial distress is hitting borrowers across every single demographic right now. Surviving this wave of defaults demands aggressive, proactive money management and flawless record-keeping. Centralizing vital financial documents into a secure, encrypted digital safe deposit box lets individuals tackle economic chaos with total confidence. Being prepared is simply the ultimate defense. It ensures that when critical financial information is needed the most, it stays protected, perfectly private, and instantly ready to use.

Why Freelancers Need Vault for Business, Insurance and Personal Docs

December 3, 2025

Running a small business or working independently as a freelancer can be incredibly rewarding, but it also comes with a unique kind of pressure. There is no support team to handle accounts, filing, legal paperwork or insurance policies. Everything falls on one person. And when documents get scattered across laptops, email inboxes, envelopes, and drawers, that pressure doubles.

Many professionals don’t realise the value of having one organised vault for business, insurance, and even personal documents until something goes wrong like a tax review, a lost invoice, a sudden medical emergency or an unexpected client dispute. Situations like these can turn a normal week into chaos if the necessary files aren’t available when they’re needed.

The Hidden Risk Behind Scattered Paperwork

Almost every freelancer or business owner ends up collecting a long list of important documents over time:

- Contracts and NDAs

- Tax records and GST filings

- Business registration and licenses

- Insurance policies

- Personal documents like PAN / Aadhaar / passport copies

- Client invoices and payment proofs

When these are stored in different places some printed, some emailed, some saved on a mobile phone, some forgotten on a hard drive it becomes hard to track what exists and what is missing. Searching for one paper in the middle of work is stressful and wastes valuable time that could be spent earning money.

It is not just about convenience scattered documents increase the chances of financial loss, missed tax claims, denied insurance claims and even legal trouble.

Why a Single Vault Makes Life Easier

Keeping all important documents in one vault (preferably digital) can completely transform the way a business operates. A well-organised vault helps in:

Faster Access When Needed

Instead of digging through old emails or piles of files, documents are found in seconds. During tax season, project negotiations, audits or emergencies, this makes an unbelievable difference.

Confidence with Clients and Authorities

Being able to quickly retrieve contracts, invoices or payment receipts shows professionalism. It also protects the business during disputes or late payments.

No More Panic During Emergencies

If a device breaks, a document goes missing or an accident occurs, a vault ensures that everything is backed up and safely stored.

Clear Separation of Personal and Business Finances

Many freelancers mix personal and business papers by accident. Keeping them in labelled folders inside one vault keeps everything organised without confusion.

Which Documents Should Be Included?

A good vault should include every document that is hard to replace, legally important or financially relevant. For example:

Business-related documents

- Licenses and registrations

- Client contracts and project agreements

- Invoices sent and payment receipts

- Expense proofs bills, subscriptions, travel, utilities

- Bank statements and annual reports

Insurance-related documents

- Health insurance policies

- Life insurance details

- Business and asset insurance

- Renewal receipts and claim history

Personal documents

- Identity proofs such as Aadhaar, PAN, Passport

- Important legal documents

- Nominee details

Keeping everything in one vault does not mix the documents it simply allows them to be stored together but categorised, making access extremely efficient.

Digital Vault vs Physical Storage Which Is Better?

Some business owners still rely on physical files, and while that is familiar, it has limitations. Paper can be misplaced, damaged by water or fire and is hard to access when travelling or working remotely.

A digital vault has several advantages:

- Documents can be accessed anytime, even while travelling or from another device

- Multiple categories and labels reduce confusion

- Search options make it easy to locate files quickly

- Backup storage ensures documents are not lost

- Sensitive information can be password protected

For professionals who work across locations or serve international clients, digital access becomes even more valuable.

Real-World Scenarios Where a Vault Saves the Day

A secure, organised vault may feel like an optional system until the moment it becomes essential:

- A client wants to verify payment for an old invoice

- A large company payroll team requests old tax receipts for onboarding

- A medical emergency requires quick access to insurance details

- A visa form needs a scanned copy of passport and financial proof

- A GST or income tax review asks for expense records from previous years

Having everything stored neatly in one place turns stressful events into simple tasks.

A Small Habit That Leads to Big Stability

Building a vault doesn’t require complicated software or a huge investment. It only needs a habit: every time an important document arrives, store it in the vault immediately. Small, consistent organisation protects both personal and professional life in the long run.

For freelancers and small business owners, a vault is not just storage. It is preparation. It is peace of mind. It is a safety net during the uncertain moments that every business eventually faces.

Final Thought

Success in business isn’t only about skills or marketing. It is also about stability and preparedness. Keeping business, insurance and personal documents in one secure vault gives a professional the confidence to grow without fear of losing control over paperwork. With organised records, business becomes smoother, income becomes predictable and stressful situations become manageable.

What Happens If You Don’t Keep Your Insurance Info Updated?

November 19, 2025

Most of us buy insurance with good intentions. We sign the papers, file them away, and honestly, we don’t think much about them again. Life gets busy. Updating insurance info is the kind of task that quietly slips off the radar. But here’s the thing: life changes constantly, and your insurance doesn’t magically keep up.

If your policy stays the same while everything else in your life shifts around, you might end up with coverage that doesn’t match your situation anymore. And that usually shows up at the worst possible time.

Why Keeping Info Updated Actually Matters

Insurance companies depend on accurate details. They decide coverage and pricing based on the information you gave them at the start. If something meaningful changes and you don’t tell them, the policy may not reflect reality anymore.

Think about how often little changes happen: moving to a different place, adding someone new to the family, buying things you’d be upset to lose, fixing up your house, or even having changes at work. None of these moments seem “insurance-worthy” at the time, but they actually matter.

What Could Happen If Nothing Gets Updated

A lot of people assume that as long as premiums are paid, everything is fine. Unfortunately, insurance doesn’t exactly work that way.

1. Claims Might Not Go Smoothly

If something goes wrong and you file a claim, the insurer will check whether your information matches your real situation. If they find a big difference, the claim might get delayed, reduced, or rejected. For example, if your home is worth more because of renovations and you didn’t update the policy, the payout probably won’t cover the full damage.

2. You Might Not Have Enough Coverage

People often don’t realize their coverage is outdated until something happens. Maybe your family has grown, or you’ve bought more valuable items. A policy that once fit perfectly might not come close now.

3. The Policy Could Be Cancelled

Insurance companies expect major details to be accurate. If something important wasn’t updated, they can cancel the policy. In rare cases, they may even say it was never valid.

4. Renewal Might Become Expensive

Sometimes outdated details cause confusion during reviews. Even if the claim goes through, renewal might come with a higher price tag.

5. Stress Piles Up When You Least Want It

Insurance is supposed to offer relief during stressful times. Outdated information can turn that relief into more stress, more paperwork, more delays, and more frustration.

Things Worth Reviewing From Time to Time

It helps to check these once in a while:

- Where you live

- Changes in your family

- Any expensive new purchases

- Home improvements or upgrades

- Vehicle changes or new drivers

- Major health or job changes

- Beneficiaries

A simple yearly check is enough for most people.

Easy Ways to Keep Everything Updated

You don’t need to make this complicated. A few easy habits can help:

- Glance over your policies once a year.

- Whenever something big happens, just send a quick update.

- Keep all your insurance documents in one place so you don’t forget what you have.

- Make a short list of things that typically change over time.

- Ask the insurer when you’re unsure; they’re used to these questions.

Final Thoughts

Insurance is meant to support you when life gets tough, but it can only do that if the information behind the policy reflects your current situation. When details sit unchanged for too long, the coverage weakens and sometimes disappears when you need it most.

A few minutes of updating here and there can save you from a lot of trouble later. It doesn’t take much, but it makes a big difference when life throws something unexpected your way.

Moving Into a New Home? Important Documents to Update and Store

November 12, 2025

The day you move into a new home is always a blur. There are boxes everywhere, someone’s hunting for the screwdriver, and the Wi-Fi isn’t working yet. Between excitement and exhaustion, paperwork usually ends up in a pile somewhere, the “I’ll deal with it later” pile.

That pile matters more than it seems. Hidden inside are the documents that prove ownership, protect your investment, and make sure you’re covered if life throws a surprise your way. Spending even half an hour getting it sorted now can save weeks of hassle later.

Here’s an easy way to stay ahead of it all.

Step 1: Collect the Home Documents

Start with the basics: anything connected to the property itself.

The deed, the lease, closing papers, inspection reports, property taxes, the list’s not short, but every one of those pages has a job to do.

Keep them together. Snap photos or scan copies and upload them to a secure place such as InsureYouKnow.org. Paper can get lost, wet, or tossed out by mistake. A digital backup doesn’t.

Step 2: Update Every Insurance Policy

It’s easy to forget how many places your address lives: homeowners, renters, car, health, even life insurance. If you’ve moved, they all need an update.

A change of address sometimes shifts coverage or premiums. Check each policy, make sure everything looks right, and store a copy in your vault. When you actually need those papers, you won’t have to dig through drawers.

Step 3: Review Finances and Bills

Moving tends to scatter money trails. One bank has your old address, a credit card statement goes missing, and a subscription quietly keeps charging the wrong account.

Before things snowball, log in to each account, banks, credit cards, utilities, and loan providers, and double-check that your information’s current. Grab a recent statement or two and save them. Come tax season, you’ll be glad you did.

Step 4: Fix the ID and Legal Stuff

This is the least exciting part, but it matters. Out-of-date identification can make the simplest tasks harder.

Head to the DMV, update your license, change your voter registration, and check your vehicle paperwork. If you’ve moved to a different state, renew your passport details too. Take a quick photo of each ID and tuck it safely into your digital folder, one less worry if a wallet ever goes missing.

Step 5: Round Up Family and Pet Records

Families (and pets) come with paperwork of their own: school transcripts, vaccination cards, medical histories, and adoption or license documents.

Put them all in one place. Upload copies so you can reach them instantly when someone needs a school form or a vet asks for proof of shots. It’s one of those tiny habits that saves time again and again.

Step 6: Check Estate and Emergency Documents

A new home changes the big picture. If you own more now than before, or live in a different state, some legal documents might need attention.

Look at your will, trust, and power of attorney. Make sure beneficiaries are still correct and that addresses match. Upload those to your vault and share access only with the people you absolutely trust. That small act can spare family members confusion later.

Step 7: Why Digital Storage Beats a Drawer of Folders

Paper doesn’t last forever. It fades, tears, and somehow always disappears when you’re in a hurry. Digital storage, especially a secure platform like InsureYouKnow.org, keeps everything in one spot, encrypted and easy to reach from anywhere.

You can label folders, set reminders for renewals, and grant limited access to family or advisors. It turns chaos into order, quietly, efficiently, without any stress.

A Quick Reality Check

Moving is a mix of energy, emotion, and endless details. Once the boxes are gone and the house starts to feel like home, take an hour, grab that pile of paperwork, and go through it.

Scan, upload, label, done. Then forget about it for a while.

It’s not the glamorous side of homeownership, but it’s the one that keeps everything running smoothly. A little organization now means fewer surprises later, and that’s worth more than any new piece of furniture.

Updating Insurance and Documents During Major Life Changes

October 30, 2025

Life Keeps Moving

A new job, a move overseas, or the day someone finally retires all sound exciting. In the middle of packing boxes or filling out onboarding forms, it’s easy to forget the quieter side of change: the policies, records, and bits of paperwork that keep daily life running smoothly.

Missing an update here can cause small but annoying problems later. A wrong address on an insurance file, an expired policy, or a forgotten beneficiary can slow down a claim when it’s really needed

When Work Life Shifts

A new role often means new benefits, different coverage, and sometimes a short gap between plans. People tend to assume everything carries over automatically, but that’s rarely the case.

- Before leaving a company, check the exact date the old health plan ends.

- Ask the new employer when coverage begins; if there’s a gap, arrange a temporary plan.

- Look at personal policies to be sure the coverage amount still fits current income and family needs.

- Update names, addresses, and phone numbers across all accounts.

- Keep the older paperwork since it’s proof if a claim from that period ever comes up.

It’s a small chore during a busy week, but it prevents confusion later.

When a Move Crosses Borders

Relocating brings excitement, but every country plays by its own rules when it comes to insurance and legal documents. A policy that worked perfectly at home might be useless once abroad.

Before boarding the plane:

- Ask the insurer about international coverage and buy a global or expat plan if necessary.

- Re-draft wills or powers of attorney so they follow local laws.

- Tell banks and pension providers the new address since some freeze accounts if mail bounces back.

- Store digital copies of important papers in a secure online vault and let one trusted person know how to reach them in an emergency.

It takes a few emails and signatures, but it can save a lot of time and stress once the move is complete.

When Retirement Begins

Retirement changes how income and coverage work. Employer insurance usually ends, and new health options need to be arranged.

- Compare health plans designed for retirees or seniors.

- Review life insurance since sometimes a smaller policy makes more sense now.

- Gather pension statements and investment reports in one folder.

- Make sure wills and executors’ details are up to date.

- Keep digital and printed copies in one clearly labeled place.

A tidy file today makes life much easier tomorrow for both the retiree and their family.

Quick Review Checklist

A few questions worth asking after any big change:

- Does current insurance still cover what’s needed?

- Are beneficiaries correct and easy to contact?

- Are legal and financial papers current?

- Is everything backed up securely?

- Has someone trustworthy been told how to access it?

If each answer is yes, everything is already in good shape.

Keeping It All Together

Loose papers and forgotten folders can turn into a real headache. A secure digital vault, such as InsureYouKnow, keeps all records in one encrypted space that can be opened from anywhere. It’s simple, private, and designed for moments exactly like these: job changes, relocations, and retirements.

Final Thoughts

Big life transitions come with excitement and responsibility. Updating insurance and personal documents may not feel urgent, but it protects the plans built over years of effort. With organized records and the right digital tools, the next chapter, wherever it leads, starts off clear and worry-free.

Seasonal Insurance Check-Up: Keep Your Coverage Up to Date

October 29, 2025

If you’ve ever opened an old folder and thought, “Wait, when did I even file this?”, you already get the point. Insurance paperwork has a way of sitting quietly until life outgrows it. People check their policies once a year, feel responsible for a minute, then forget about them. Sounds familiar, right?

Life, though, doesn’t wait. A new job pops up, someone moves, a baby arrives, or maybe there’s a home remodel that changes everything. Those small shifts can make old coverage feel out of step. By the next annual review, it’s easy to realize things don’t quite fit anymore.

Life Changes Faster Than Paperwork

Insurance is supposed to protect what matters now, not what mattered last spring. But most people never notice how fast their details drift. Maybe the car value has dropped, or a phone number changed, or the policy still lists an address that no one lives at. Tiny errors, but they matter when a claim appears.

A quick seasonal review keeps things real. It’s like glancing at your pantry before heading to the store, fast, practical, and you avoid buying what you already have.

How to Do a Seasonal Review Without Losing a Weekend

Step 1. Gather your stuff.

Pull together every policy: car, home, health, life. Keep them in one folder, digital or paper, so you’re not hunting later.

Step 2. Check the basics.

Look at names, addresses, contact numbers, and nominee info. If something looks off, fix it.

Step 3. Match it to real life.

Bought something big? Changed jobs? Maybe started freelancing? Adjust the coverage so it actually fits.

Step 4. Note payments and renewals.

Set a quick reminder on your phone. Late payments sneak up quietly.

Step 5. Keep copies safe.

A cloud folder and one printed set usually do the trick. Tell someone close where they are.

When to Check Even Sooner

Some moments don’t wait for the next season. Big life changes mean the file needs a look right away:

- Marriage or separation

- New house or sold property

- Moving cities

- Starting a business

- A new baby or dependent parent

If your life just shifted, your coverage should shift too.

Why Bother?

People who do this regularly sound calmer when things go wrong. They don’t waste time searching or wondering what’s covered. The habit keeps surprises small.

Here’s what they get out of it:

- Current coverage: Nothing outdated hiding in fine print.

- Fewer claim issues: Information is already right.

- Possible savings: You catch overlaps before paying twice.

- Less stress: Everyone knows where everything lives.

A little check four times a year adds up to peace of mind.

Make It Stick

Pick a date that already matters, your birthday month, tax season, the start of summer. Mark it as “insurance check-up” and actually do it. Once or twice and it’ll feel automatic.

The Bottom Line

Insurance only works when it keeps up with your life. A seasonal check-up isn’t overkill; it’s common sense. Fifteen minutes now can save weeks of frustration later, and that’s a trade anyone would take.

On the Lookout for Free Money? Focus Your Search on Grant Opportunities

June 11, 2020

Individuals, communities, nonprofit organizations, and businesses continue to feel the ever-increasing effects of the COVID-19 pandemic. To help keep them afloat while dealing with diminished incomes and benefits, isolation away from friends, family, and colleagues, or facing an unknown future of returning to their previous careers or businesses, they can seek emergency financial assistance.

As the following selected links demonstrate, a variety of grantors are currently offering grants to assist in meeting financial challenges resulting in the continuing threat of COVID-19.

Grantspace by Candid provides a continually updated list of emergency financial resources including the following grant opportunities.

For Individuals

- The United Way, accessible at www.211.org or by dialing 211, provides a comprehensive list of available resourcesto locate food banks, to help pay housing bills, and to access free childcare and other essential services available on local, national, and statewide bases.

- Coronavirus Tax Relief: Economic Impact Payments is an IRS web page that lets non-filers enter payment information and others to check on the status of their stimulus payments.

- Economic Impact Payments: What you need to know is a FAQ page created by the IRS to answer questions about stimulus payments.

- Restaurant Workers’ Community Foundation COVID-19 Relief Fund provides emergency funding for those employed by or own restaurants or bars facing unforeseen expenses not covered by insurance.

- Americans for the Arts Coronavirus Resource and Response Center includes a list of funding/grants resources.

- COVID-19 Freelance Artists Resources is an aggregated list of free resources, opportunities, and financial relief options available to artists of all disciplines.

- Creative Capital Arts Resources During the COVID-19 Outbreak is another list of financial resources for artists working in all disciplines.

- Freelancers Relief Fund grants financial assistance of up to $1,000 per freelance household to cover lost income and essential expenses not covered by government relief programs.

- Student Relief Fund lists resources for college students in need of support due to campus shutdowns caused by COVID-19.

- Artist Relief lists grants for artists facing dire financial emergencies due to COVID-19 in the U.S.

- Artist Relief Project publicizes grants for any artist in any discipline whose income has been impacted by COVID-19-related cancellations and closures.

- American Guild of Musical Artists (AGMA) Relief Fund provides support and temporary financial assistance to members in need.

- Equal Sound Corona Relief Fund for Musicians who have lost income due to a cancelled performance as a result of the COVID-19 outbreak.

- New Music Solidarity Fund offers emergency funds to support freelance artists in the new/creative/improvised music community.

- Dramatists Guild Foundation Emergency Grants provides emergency financial assistance to individual playwrights, composers, lyricists, and book writers in dire need of funds due to severe hardship or unexpected illness.

For Communities

- GrantWatch promotes an Opportunity for USA Organizations to Raise Funds to Benefit Communities Impacted by the Coronavirus (COVID-19).

- Community Foundations Nationwide Launch Coronavirus Relief Efforts is a full listing of more than 500 U.S. community foundations in all 50 states, plus the District of Columbia, that support those affected by COVID-19—directing critical relief to local nonprofits and partnering with local governments and health organizations to help contain its spread.

For Small Businesses

- Small Business Administration Disaster Assistance Loans provide economic relief to businesses that are currently experiencing a temporary loss of revenue.

- SBA Paycheck Protection Program – An SBA loan that helps businesses keep their workforce employed during the COVID-19 crisis.

- GoFundMe Small Business Relief Fund helps small businesses that have been affected by the COVID-19 pandemic and empower their communities to rally behind them. GoFundMe has partnered with Yelp, Intuit QuickBooks, GoDaddy, and Bill.com to provide small business owners with the financial support and resources needed to continue running their businesses during and after the coronavirus crisis.

- Facebook Small Business Grants Program – Facebook is offering $100M in cash grants and ad credits for up to 30,000 eligible small businesses in over 30 countries where it operates.

- Financial Assistance for Small Business is a list of programs providing financial assistance to small businesses compiled by the U.S. Chamber of Commerce Foundation.

- Opportunity Fund Small Business Relief Fund supports eligible small businesses, especially those run by women, people of color, and immigrants, impacted by the COVID-19 crisis.

For Nonprofits

- Funding for Coronavirus (COVID-19) shares information about philanthropy’s response to the pandemic

- CARES Act: How to Apply for Nonprofit Relief Funds is a guide created by Independent Sector.

- Loans Available for Nonprofits in the CARES Act is a chart from the National Council of Nonprofits providing details on loan options, eligibility criteria, terms, and application information.

- State Public Policy Resources on COVID-19 is the National Council of Nonprofits page for nonprofit-specific materials from state officials and useful resources on what states are doing in response to COVID-19.

- Grantmakers Concerned with Immigrants & Refugees COVID-19 Resources is an aggregated list of resources for nonprofits working with immigrants & refugees.

In general, grant opportunities and corresponding applications adhere to strictly announced deadlines and requirements so potential grantees need to submit proposals on time and meet the specific provisions outlined in each grant’s description. At InsureYouKnow.org, you can save your documents and files relating to grant applications and set up reminders to alert you to keep track of timelines for submitting grant applications and to check on grants awarded.

Financial Advisors 101

November 26, 2019

Have you wondered if you need a financial advisor? Are you puzzled about the type of financial professional you need to help with investing, financial planning, selecting insurance, repaying debt, education funding planning, tax planning as well as estate and retirement planning?

Many titles, including robo-advisor, broker, investment advisor, and financial planner are used to describe financial advisors who help clients manage their money and achieve long-term financial goals. Although there is crossover among all groups, and many financial advisors hold multiple credentials, they can be described in general as follows:

1. Robo-advisors

Robo-advisors use computers to select and manage your investments. Some offer access to human advisors to answer questions, but their primary service is investment management, not financial planning.

Fees start as low as 0.25% of your balance and most charge 0.50% or less. Many have no or low account minimums, so you can start investing with a small amount of money.

Consider whenyou need help investing for financial goals like retirement, but don’t want or can’t afford a more holistic financial plan.

2. Online financial planning services

Relatively new to the market, these services offer investment management in conjunction with virtual financial planning. Clients typically meet with financial advisors by video or phone and receive comprehensive financial plans.

Fees, based on how much money is overseen for you, are described as “assets under management,” or AUM, that might range from 0.25% of your account balance to 1% or more, depending on the type of advisor you choose.

Consider when you are interested in investment management, a comprehensive financial plan, and ongoing access to financial planners for less than the cost of a traditional in-person advisor.

3. Traditional financial advisors

Working directly with clients to help them meet their short- and long-term financial goals, traditional financial advisors recommend specific investments and insurance products and may provide tax advice. In most cases, you’ll work with an advisor in your local area.

Fees will be based on a median financial advisor fee of about 1% of the assets managed for you, although some charge by the hour or have a set rate per service. Some require a minimum balance, such as $250,000 in assets.

Consider when you want specialized services, your situation is complex, or you want to meet your financial advisor in person.

4. Brokers

Brokers work for broker-dealers—firms in the business of buying and selling securities (stocks, bonds, mutual funds, and other investment products) for customers. Brokers are required to make “suitable” recommendations for clients.

Fees are typically a mix of commissions and an advisory fee for portfolio-management services. Each firm has its own compensation formula. Statements show advisory fees and transaction costs.

Consider when you need guidance or broad advice on funds or stocks, or on how to divide your assets among stocks and bonds based on your age and risk tolerance.

Tips for finding the best financial advisor for you

Once you’ve decided which type of financial advisor is best for your situation and budget, you can start your quest of finding an advisor appropriate for you.

You should interview a few financial advisors before choosing one. Ask questions (including ones about philosophy on financial planning and investing, experience working with clients like you, and the number of years in practice) and check out their credentials and disciplinary history.

To vet a registered investment advisor, visit the U.S. Securities and Exchange Commission database, search an individual’s name, and find information on qualifications, employment history, disciplinary actions by regulators, and criminal convictions.

When you’re ready to seek a financial advisor’s assistance, prepare by arming yourself with your personal financial data and specific questions to find the right pathway. Then, you can store quarterly and annual reports as well as investment portfolio changes at insureyouknow.org.