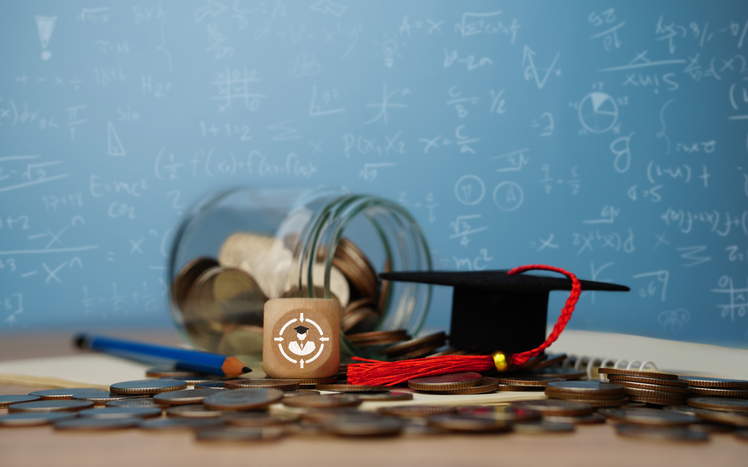

Category: Financial

Cost of Tuition Shouldn’t Deter Students

July 15, 2025

According to the Education Data Initiative, the cost of tuition at a four-year college has increased by 141% over the last twenty years. The average yearly cost for classes ranges from $9,750 at a public school and $35,248 at a private school.

Even with the rising cost of college, a degree still gives many graduates a higher earning potential. In 2023, workers with a bachelor’s degree earned 61% more than those with a high school diploma.

A 2024 Third Way survey found that 29% of high school students don’t plan on attending college because of the price, but the cost of tuition doesn’t have to be a barrier.

Here’s everything parents and prospective students need to know about saving for college.

Earn a Two-Year Degree for Less

One of the easiest ways to save money on tuition is to remain where you are. When you attend an in-state school and can prove your residency, you avoid the much higher out-of-state tuition rate. You can save a lot of money on tuition if you earn the first two years of your degree at a public community college before transferring.

A year at a community college can cost as little as $3,500, while attending an out-of-state public university can cost $35,000 per year. Plus, if you weren’t accepted into your first-choice university after high school, earning your two-year degree improves your odds of being accepted into another four-year university as a transfer student.

Most states also offer dual enrollment during high school. This means that students can attend both their high school and a local community college simultaneously, earning college credits or even a two-year degree by the time they graduate from high school. Not only do graduates get a head start, but they also shave two years’ worth of tuition off their bottom line, since the state funds these programs.

“A lot of people don’t go to college because it’s just so expensive,” says Ahmad Shehadeh, a Roxbury Community College student who’s attending through a Massachusetts state-funded program. “So by tuition being free, it’s benefiting the community in a way, and I’m glad that other people like me will have the opportunity to go to college and pursue what they need to pursue: their dream.”

For more information on your state’s dual enrollment opportunities, you may check the Education Commission of the States.

Meet With Your Counselors

To find out if your high school offers programs like dual enrollment, you’ll need to meet with your school’s guidance counselor, and the sooner you start high school, the better. Guidance counselors can help students devise their post-graduation plans and assist with the college admissions process, financial planning for tuition, and even scholarship applications.

The same rule applies to college. Financial aid counselors can help prospective students determine how to pay for their classes. Contact a counselor at each of your potential schools. For instance, they will know if their college offers work programs, such as the Federal Work Study program, where students can work on campus part-time while enrolled in classes.

All high school and college counselors will likely encourage every potential student, regardless of age, to complete a FAFSA form to determine if they qualify for any government aid.

Saving With a 529 Plan

Parents who want to begin saving for their children at birth will yield the most savings if they start earlier. The longer you wait to begin saving for your child’s tuition, the more you’ll have to save up each month to have enough for four years of tuition by the time they graduate from high school.

Using a savings account that yields interest for as long as possible is also beneficial. A 529 plan is a high-yield savings account designed for educational expenses. If you can save $100 a month in a 529 plan for 18 years, the total amount contributed will be $21,600. If the average annual return is 5%, your total savings with interest would be $35,400.

A 529 also comes with tax incentives. The money you earn as interest is tax-free, as well as any funds you withdraw for the beneficiary’s educational expenses. Additionally, these accounts are designed for anyone who wants to attend college. Adults who wish to return to school can open these accounts, name themselves as the beneficiary, and use the interest-bearing funds for their tuition.

Budget As You Go

College learning tracks vary for each individual. There’s always the option of taking one to two classes per semester instead of a full load of four or more. Students may opt to complete their degrees over a more extended period for various reasons, such as needing to work full-time or having children. Saving up for classes as you take them comes with some upsides, such as being able to focus more intently on coursework.

“If you’re working during college, you’re gaining important work skills that will be valued by future employers,” says Daniel Douglas, director of social science research at Trinity College in Connecticut. “You know about showing up on time, following directions given by a supervisor, and being generally diligent in your duties.”

Whether you’re a high school student or an adult who wants to attend college, begin to calculate how much money and time coursework will cost you. For example, if you still have to juggle a full-time job, then you need to be realistic about when you’ll attend classes and study. Time needs to be part of your budget, too.

When to Consider a Loan

There is no shame in considering a student loan once you’ve exhausted every other payment option. This is especially true if you have a high return on investment, meaning you’re earning a degree that will help you obtain a high-earning career. If you’re considering a loan, start with Federal Student Loans, which offer several built-in protections.

The cost of tuition shouldn’t deter anyone from pursuing their dreams. By doing research and conferring with counselors, you can come up with a plan to pay for college, even if that means getting creative. With Insureyouknow.org, you may store all of your research, financial planning, and school records in one place, making it easier for you to review and stay focused on your goals.

Everything to Know if You Want to Live and Age in Place

June 1, 2025

Most people would prefer the comfort of having their own space as they age. Studies show that as many as 90 percent of adults wish to remain home. Living in place, sometimes known as aging in place, also equates to maintaining independence for as long as possible.

“For many of us, home is comfort. There’s a history we are familiar with: It’s family, friends and neighbors. It reflects our culture and our community,” says Emily Johnson, a licensed clinical social worker. “As we begin to lose control of other aspects of our life, staying in our home says, ‘I can accept help, but I am still running the show.”’

Remaining home as you grow older requires careful consideration and thoughtful planning. Here’s everything you need to know about living and aging in place.

Make Your Plans Now

The best thing to do if you want to age in place is to plan for it now while you are still able to. Consider what kind of help you may need now or want in the future. Planning ahead gives you time to set up your home and budget for the required changes and services.

Be sure to factor in any health conditions you or your spouse may already have. Think about how that condition may make it difficult to care for yourself independently. Then, talk to family and friends about what level of support they can offer. Ensure everyone’s realistic and plan to revisit the issue periodically over time.

On average, an adult over the age of 65 falls every second in the U.S. You can prevent accidents at home with these simple safety measures:

- Apply contrasting colored electrical tape on stair landings.

- Remove throw rugs without grip from the home.

- Clear away clutter, including loose cords.

- This includes the outdoors; porches and walkways should be swept and shoveled.

- Ensure the home is well-lit and place night lights in halls and bathrooms.

- Always use handrails and install grab bars in showers and tubs and next to the toilet.

- Always wear proper-fitting supportive shoes in the house and outdoors.

As conditions change, you may need to reassess your home regularly for potential hazards. To troubleshoot, ask a family member or friend to complete a walkthrough with you for a second set of eyes.

Budget For Services

Home-based care services can be used in short-term situations, such as during recovery from surgery, or in the long term for those who need ongoing help. In addition to healthcare services, people may need help with chores, meal delivery, or transportation for doctor’s visits.

While home-based services can be expensive, they may cost far less than moving into an assisted living facility. The Eldercare Locator is a resource that connects people to caregivers through local support services.

People often rely on various payment sources, including personal funds, long-term care insurance, and government programs. For more information on government-based healthcare and financial assistance, visit USA.gov.

Prioritize Your Long-Term Health

If your goal is to stay home, then make your overall health maintenance a top priority. Stay current with your doctor’s visits and set alarm reminders for medications.

Make a plan to maintain body strength as you age, powerful legs to support balance and assist you in getting up safely from a seated position. “Strength, balance, and flexibility exercises are key to preventing falls, which are among the greatest threats to our healthy longevity,” says Scott Kaiser, a family physician and geriatrician.

In addition to scheduling regular exercise into your routine, don’t forget about your mental well-being. “Investing in meaningful relationships is one of the most important things we can do to increase our health, quality of life, and wellbeing,” says Kaiser. Remain engaged in social activities and plan visits with loved ones, including video calls with those who live farther away.

Prepare for the Unexpected

Always be prepared for unexpected events and medical emergencies. “Be proactive,” says Johnson. “Where are there gaps now or barriers to living independently in the future?” For instance, if you have a preexisting allergy or medical condition like diabetes, wearing a medical alert ID bracelet is a simple precaution. A wearable electronic monitor that can alert emergency personnel in the event of a fall is another easy measure to implement.

Even if the plan is to stay at home for as long as possible, there may come a time when that’s no longer safe. The decision about whether or not to move away from home is a difficult and emotional one to make.

It’s best to mentally prepare for that possibility now while there’s still time to have some control over where you’ll go. Learn as much as possible about the available housing options and include loved ones in the search.

Living in place is an attainable goal with the right amount of forethought. At Insureyouknow.org, you may store all of your financial and medical records in one easy-to-review place. By staying on top of your budget and health needs, you will have already taken care of the most critical components of your aging-in-place plan.

How to Prepare for College Living: A Survival Guide for Incoming Students

February 15, 2025

Congratulations! You’ve been accepted into college, and soon, you’ll embark on one of the most exciting adventures of your life, along with 16 million others. But before you start dreaming about campus life, late-night study sessions, and newfound independence, there are some practical steps to ensure a smooth transition. From dorm essentials to financial planning, this guide will help you prepare for college living.

1. Master the Art of Budgeting

Living on your own means managing your finances wisely. Here’s how to stay on top of your budget:

- Create a Budget: Track your expenses, including tuition, rent, food, transportation, and entertainment.

- Use Budgeting Apps: Apps like Mint, YNAB, or PocketGuard can help you stay organized.

- Open a Student Bank Account: Many banks offer students accounts with low or no fees.

- Look for Discounts: Your student ID is your best friend—use it for travel, entertainment, and shopping discounts.

2. Pack Smart: The College Essentials Checklist

You don’t want to arrive at college and realize you forgot something crucial. Here’s what to bring:

- Dorm Room Must-Haves:

- Bedding (twin XL sheets, comforter, pillows)

- Storage bins and organizers

- Desk lamp and power strips

- Laundry hamper and detergent

- Shower caddy and flip-flops

- Tech Gear:

- Laptop and chargers

- Noise-canceling headphones

- Portable hard drive or cloud storage subscription

- Kitchen Supplies:

- Mini fridge (if allowed)

- Microwave or coffee maker

- Reusable water bottles and utensils

- Emergency Kit:

- First aid supplies

- Medications

- Flashlight and extra batteries

3. Set Up Your Health & Insurance Plan

Make sure you have a solid plan in place for medical needs:

- Health Insurance: Check if you’re covered under your parent’s plan or if your college offers coverage.

- Locate Healthcare Providers: Know where the nearest doctor, dentist, and urgent care clinic are.

- Stock Up on Essentials: Pack prescription medications, vitamins, and a basic first-aid kit.

4. Learn Basic Life Skills

College is a time to gain independence, so mastering basic skills will help you thrive:

- Cooking Basics: Learn how to make simple meals to save money and eat healthier.

- Laundry 101: Know how to separate colors, use detergent, and read washing machine settings.

- Time Management: College life is busy—use planners or apps to manage assignments and social activities.

5. Prepare for Roommate Life

Sharing a living space can be a challenge, but good communication helps:

- Set Boundaries Early: Discuss sleep schedules, cleaning duties, and guest policies.

- Be Respectful: Small gestures, like cleaning up after yourself, go a long way.

- Resolve Conflicts Maturely: Address issues directly and respectfully to maintain a positive environment.

6. Get to Know Campus Resources

Colleges offer plenty of support services—take advantage of them!

- Academic Support: Visit tutoring centers and writing labs.

- Mental Health Services: Many colleges offer free or low-cost counseling.

- Career Services: Start networking and building your resume early.

- Student Organizations: Join clubs to meet new friends and enhance your college experience.

College is a time of growth, challenges, and unforgettable experiences. By planning ahead, you can make the transition smoother and set yourself up for success. Embrace the adventure, stay organized, and don’t hesitate to ask for help when needed. You’ve got this!

InsureYouKnow.org

College graduation prompts transitioning from a school-based existence to one replete with adult responsibilities. By preparing for the unforeseen future, college grads who do their homework and keep their records at insureyouknow.org, can begin living their lives to the fullest.

Get The Most Out of Credit Card Rewards for Your Next Vacation

February 1, 2025

According to a survey conducted by Lending Tree, even though 87% of all credit cardholders earn rewards, nearly 70% are sitting on unused cash back, points, or miles. Regarding travel, only 12% optimized their rewards to earn a free flight or hotel stay last year. “Many people who collect rewards are doing so with a goal in mind, such as a dream vacation with their family,” says Matt Schulz, a credit analyst at Lending Tree. “As they earn, those rewards points and miles sit unused.”

While the reasons behind leaving rewards vary, many people don’t know how to use them. Understandably, cashing in rewards benefits for the first time can be intimidating, but that’s no reason to leave value on the table.

Here’s everything you need to know about earning the most travel benefits from your spending and cashing them in for priceless vacation memories.

Compare Credit Cards to Find the Best Fit For Your Goals

Take your time comparing credit cards to find one that fits your needs, and then make it your main payment method. This means comparing bonus offers and the types of rewards offered.

You’ll want to make sure you’ll be able to use the points you earn for the travel you want. A good credit score is a normal requirement to get the best travel rewards cards, which is usually at least 670. If you’re not quite there yet, you may want to focus on improving your credit first to get the best offers.

Everything to Consider When it Comes to Bonus Offers

If you’re open to getting more than one credit card, then you may want to get a few that offer the best sign-up bonuses. A sign-up bonus involves charging a certain amount of money within a specified time period to earn the cash back or points bonus. When using your rewards for travel, you would then put that cash back or points toward your next vacation, including airfare and lodging.

For instance, with a Citi Double-Cash Card, rated the third-best credit card in 2024 by Card Critics, you could earn $200 cash back or 20,000 Thank-you points after spending $1,500 within the first six months. For most people, charging $1,500 worth of expenses over six months is feasible, but your spending capability should be the top consideration when comparing bonus offers. “Sign-up bonuses can be really helpful for folks on a tight budget,” Schulz says. “Just make sure that you’re comfortable with how much you have to spend to get the bonus.”

If you find yourself trying to spend more than you normally would to earn a sign-up bonus, then the cash-back offer likely doesn’t make financial sense. As long as you think of bonus offers as something you could earn simply by paying your existing bills, then they’re a great way to earn rewards toward a vacation you might not otherwise be able to afford.

Rack up Rewards Beyond the Sign-Up Offers

Once you’ve earned your sign-up offers, you’ll want to spend as much on your credit card to continue earning rewards. When considering which cards are the best for you, you’ll want to pay attention to the rewards they offer and what kinds of purchases qualify for reward points. Many card purchases only qualify for points in certain categories, such as gas or groceries, while others only qualify with specific experiences like dining or travel.

This is why it’s so important to think about what you’re already spending money on, because the goal is to earn rewards for what you already need to buy rather than changing your lifestyle to rack up points. “No matter how lucrative the rewards, overspending to get them doesn’t make sense,” Schulz says. “The math just doesn’t work in your favor.” If you’re someone on a budget that saves by not eating out a lot, then a card that rewards you for groceries is going to be the best fit for you, while the person who eats out and hardly ever cooks at home is going to benefit the most from using a card with dining rewards.

Know the Difference Between Types of Points

Typically, credit cards work with certain airlines and hotels where you can redeem your points, so when choosing the card for you, make sure you want to use the companies where your points will be easy to redeem and worth the most value. There are three types of reward points: fixed value, variable value, and transferable points.

- Fixed value points have a clear published dollar value. For example, points might be worth one cent each when redeemed for travel rewards. The advantage of fixed value points is that you can always use your rewards for purchases that would otherwise require cash, but the downside is that there’s no way to outsize the value of your points. A $100 ticket may require 10,000 points at one cent per point.

- Variable rewards involve the cost of a hotel stay or airfare being attached to a specific amount of points, so one night at a specified hotel may cost 20,000 points, even if the cash amount of the room varies. The perk of variable rewards is knowing when to redeem them for outsized value.

- Transferable points are also known as flexible points because they can be transferred to other partner programs for redemption. You may also be able to cash in on rewards as statement credits or redeem them toward travel at a fixed rate. This variability makes transferable points desirable.

It’s easy to lose track of how many points you’ve earned, especially if you decide to earn with more than one card, so consider using a spreadsheet to keep track of your earnings. Once you’re ready to redeem your points for travel, you’ve made it the most exciting part. Simply begin with your credit card’s website, which should be your first stop in redeeming your rewards. The website should have all of the information you need to know, such as comparing cash back versus points for travel or step-by-step directions for transferable points, plus any current promotions.

Whether or not you’re on a tight budget, earning rewards that can be used toward your next vacation is something anyone who uses a credit card should be taking advantage of. As exciting as traveling can be, traveling for less is even more so. With Insureyouknow.org, you can keep track of your spending, rewards earned, and travel goals all in one easy-to-access place. Once you learn how to get the most out of your rewards, you’ll become an expert on traveling for less in no time at all.

Medicare Grocery Allowances: Who Qualifies and Is it Worth it?

January 15, 2025

In 2020, the Medicare Advantage expanded coverage benefits for those with chronic conditions, such as cancer, autoimmune disorders, diabetes, end-stage renal or liver disease, heart disease, and more. The coverage expansion is referred to as the special supplemental benefits for the chronically ill or SSBCI. Some additional benefits include food allowances and prepared meals, but in some instances, they may even include over-the-counter medications, transportation, and in-home support services.

If you’re interested in receiving a grocery allowance or meal benefits or need food assistance, here’s everything you need to know about the additional coverage.

How the Medicare Grocery Allowance and Meal Benefits Work

Grocery allowances and meal benefits are not the same. If you qualify for grocery allowances, they are issued through prepaid debit cards on a monthly or quarterly basis. While the grocery allowance varies by state, it is usually $50 each quarter.

Under the CHRONIC Care Act, as of 2020, Medicare Advantage plans could also provide meals anytime to keep eligible recipients from needing hospitalization. Meal benefits are often more popular than grocery allowances, but it’s usually only offered for a limited amount of time, which is typically four weeks after a hospital stay.

Knowing Which Plans Offer Food Assistance

Not all Medicare Advantage plans include food allowances, so it’s important to determine if you qualify before choosing a plan. Traditional Medicare Part A and Part B and Medicare supplement plans, which are meant to supplement gaps in coverage, do not offer a grocery allowance. Some Part C Medicare Advantage Plans do offer grocery allowances and meal benefits, such as special needs plans or SNPs and dual-eligible special-needs plans D-SNPs. D-SNPs are meant for Medicare members who are also enrolled in Medicaid and who have a chronic condition. Those with Medicare Advantage plans who are disabled or who have a low-income subsidy or LIS may also be eligible to receive grocery benefits.

The CHRONIC Care Act of 2020 gave Medicare Advantage plans the ability to offer non-medical benefits such as funds for groceries. “Therefore, the Medicare Advantage plan can decide if they want to provide those benefits, and those benefits have to be designed only for the chronically ill,” says Alexandra Ashbrook, director of the Food Research and Action Center. “The non-medical services have to be targeted to people who have at least one chronic health condition, such as those at risk of hospitalization or some other adverse health outcome requiring intensive care coordination,” she says.

Qualifications for the grocery and meal benefits vary by plan, so it’s important to check with the plan’s provider to see what they offer and if your health condition qualifies. Choosing a plan based solely on food allowances isn’t the best approach over the long run. So, even if the plan offers a grocery or meal benefit, it may not justify what you pay for the plan. Whether or not the plan covers medical needs should always be the priority. Take into account every benefit the plan offers before making a decision.

What to do if You Don’t Qualify for Medicare Food Allowances

There are still other options for those who do not qualify for the grocery allowance through their Medicare Advantage Plan. Low-income seniors 60 or older can apply for food assistance through the Supplemental Nutrition Assistance Program or SNAP. Many people don’t even realize that they qualify for these benefits. “Unfortunately, only about 48% of eligible older adults are participating in SNAP,” Ashbrook says. “That’s a really important gap that health care providers and health systems could help to close before looking at any of the other additional food programs.”

Those who are 60 or older and have an income below 185% of the federal poverty income guidelines may also qualify for the Senior Farmers’ Market Nutrition Program SFMNP or the Commodity Supplemental Food Program or CSFP. The SFMNP provides coupons for fresh fruits and vegetables, which can be used at farmers’ markets and community farms, while the CSFP is a monthly package of healthy food that the USDA distributes to local agencies for participants to pick up. If eligible, some states even offer package deliveries.

To find out if you are eligible for SNAP or either of these additional programs, you may fill out an application online. If you’re a veteran, for instance, you may be more likely to qualify for USDA food assistance programs. Even if you are not eligible for Medicare grocery allowances, SNAP, or other supplemental programs, you still have options. Meals On Wheels is another program designed to help low-income seniors access prepared meals. The meals are provided on a sliding scale based on a recipient’s income to make them an affordable option for those in need.

If any food assistance will help you, then exploring every available benefit will pay off. Whether it’s a Medicare food allowance or a USDA-based food assistance program, helping purchase and prepare healthy foods can go a long way in improving the quality of your everyday life. With Insureyouknow.org, you may keep track of your applications, health records, and grocery budgets in one easy-to-access place for all your meal planning needs.

Is Your Home Ready for Extreme Weather?

January 1, 2025

From wildfire season with smoky air to higher temperatures and unexpected blackouts during freezing temps, the reality of extreme weather conditions is causing homeowners to better prepare their homes. While every homeowner should feel safe at home, a recent survey by Certain Teed revealed that less than 48% of people feel confident in their home’s durability in the face of extreme weather.

The good news is that smart updates will bring peace of mind and add value to your home. While some projects cost more money and time than others, there are several that require less of an upfront investment. No matter your budget, here are five easy home improvement areas to consider to protect your home and feel safer during weather events.

HVAC Systems Can Protect Against Temperatures and Poor Air Quality

Because people spend 90 percent of their time indoors, the quality of your home’s indoor air is crucial to the quality of your home life. One way homeowners can prepare for extreme weather and climate events is to make sure they have a reliable and well-maintained HVAC system in place. While it can be difficult to predict when climate-related issues may happen, an HVAC system can maintain inside temperatures, withstand harsh weather outside, and provide filtration that improves indoor air quality no matter what unfolds.

Preventative maintenance on your HVAC system and changing the filter every 30 to 90 days will help prolong the life and quality of your investment. Keeping your system at or above 64 degrees Fahrenheit during the colder months also helps prevent expensive issues like frozen and burst pipes.

Choose the Right Roofing Materials For Your Climate

Roof upgrades significantly increase your home’s resilience as well as its value. “The roof is the first line of defense on a home,” says Teed Lucas Hamilton, manager of applied building science at Certain. “It is important to select the right materials for your climate,” he says. Impact-resistant roofing, solar reflective shingles to combat rising temperatures, and fire-resistant materials are all things to consider when choosing roofing materials. In areas where strong wind is a possibility, hurricane fastening and straps can also further secure your roof.

When updating the roof, take into account the gutters. Simple add-ons like leaf filters help prevent blockages so that water doesn’t back up during heavy rainfall. When flooding is a concern, gutters should direct drainage away from the home’s foundation. Too much water around the foundation can lead to serious structural issues in the future, such as cracks in the foundation. A sump pump, which runs automatically to keep water out of basements and away from the foundation, is another wise investment in areas with heavy rain and storms.

Consider Window Updates or Replacements

In areas where debris impact is an issue, shutters that can cover existing windows ahead of a storm can safeguard a home during large storms. Impact windows, which have a heavy-duty frame and glass that’s engineered to remain intact even if it breaks in a collision, are another option, but depending on the number of windows your home has, they can get expensive.

Less expensive alternatives to shutters and window replacements include sealing existing windows and applying tints.

“First, use caulk to seal up any holes and cracks on the outside. Then apply weatherstripping and use a window or door insulation kit to block the cold and heat from the inside,” Hamilton says. “These changes help strengthen the barrier between your home and the outdoors, saving on heating and cooling and keeping the elements outside.”

Applying window tinting is another example of an inexpensive update that can block up to 80% of summer solar heat while also keeping some heat inside during winter months. Updates such as these protect from weather and increase energy efficiency by creating a better barrier between your home and the outside elements.

Make Simple Exterior Updates

Steel doors, which are made of more durable materials than some more elaborate door styles, upgrade a home’s entry points by withstanding storms. When certain updates, such as replacing every window in the house, are not in your budget, replacing the home’s main entry points with stronger doors can be a good place to start.

Changing the color of your exterior paint is another affordable update that can help with temperature control. “You might think that choosing the exterior color of your home is only about picking what color you like best,” says Angie Hicks, co-founder of Angi, formerly known as Angie’s List. “The climate you live in is crucial to picking the right color.”

In hot climates, light colors will help to reflect the sun and keep the interior cool, while those who live in climates prone to extreme colds should choose darker tones to retain heat better.

Maintenance is Key to Safeguarding Your Property

With increased extreme weather events, your home could be damaged slowly over time. It becomes more important to inspect your home for changes and keep up on maintenance to prevent larger repairs and damage down the road. Checking your roof after storms, such as noting any cracks, sagging, or debris in the gutters, is an important part of keeping your roof resilient during the next event. Trees around your home should also be checked for cracks in large branches or soggy soil around the roots, as those should be addressed to prevent damage in a future storm. Gutters should also be cleared regularly to prevent blockages, as well as collect debris from the yard that could become projectiles.

Insureyouknow.org Make sure you’re aware of how your community issues weather alerts. While some use outdoor sirens, others depend on media and smartphones to alert residents of severe storms. No matter what kind of hazards your community may be prone to, the National Weather Service recommends developing a plan with your family ahead of time, such as knowing where your emergency meeting place is or where the safe room is in your home. Safe rooms are usually those without windows at the lowest level of your home. In the event that your home is compromised, Insureyouknow.org can protect all of your vulnerable paper documents by ensuring digital access, providing you with one less thing to worry about so that you may focus on the safety of yourself and your loved ones.

QLAC 101

August 15, 2024

If you’ve saved well for retirement, then you may find you can cover your living expenses without needing to withdraw from your retirement accounts. But if you think that by age 73, you won’t need your full required minimum distributions or RMDs, then you might want to consider getting a qualified longevity annuity contract, or QLAC.

Anyone between the age of 18 and 75 can purchase a QLAC, but there may be some people that this annuity makes more sense for. If you’re looking to avoid the market risk on some retirement accounts and ensure a steady, guaranteed income in retirement, a QLAC is probably a good fit for you. If you also have concerns about the longevity of your savings and having enough money later in life, then you may benefit from a QLAC.

Here’s everything you need to know about a QLAC before deciding if it’s right for you.

How a QVAC Could Lower Your RMDs

A QLAC is a deferred fixed annuity contract sold by insurance and financial companies that you purchase with money from a retirement account, like a 401(k) or an individual retirement account (IRA).It’s important to know that Roth IRAs cannot be used to purchase QLACs as they do not come with RMDs to begin with.

RMDs are mandated starting at the age of 73 as of this year, but that will rise to age 75 in 2033. One appeal of the QLAC is that it can reduce the balance in your retirement accounts used to calculate those RMDs. “People tend to spend their RMDs,” says Steven Kaye, a financial planner in Warren, New Jersey. “So a QLAC forces people—in a good way—to leave more money in their IRAs,” he says.

One way to avoid using your RMDs is to use the funds from one of your retirement accounts to purchase a QLAC, which will guarantee that you receive regular payments for as long as you live. “So, if you used 25% of a $400,000 qualified account, your $100,000 purchase of a QLAC would immediately reduce your RMDs by 25%,” says Jerry Golden, investment advisor. “And the income from a QLAC could be deferred until as late as age 85,” he says.

When you choose a QLAC, you’ll be able to set your payout date, which is when you’ll begin receiving payments. Just like with Social Security, the longer you wait to receive payments, the higher the payments will be. Once you have a QLAC, you’ll be able to delay RMDs until the payout date of your QLAC, which can be no later than age 85.

The Tax Benefits of Having a QLAC

Once you withdraw money from your QLAC, you’ll need to pay income taxes on it. However, a QLAC can be an efficient tax planning strategy. For example, by using $100,000 of a traditional IRA to purchase a QLAC, you’ll reduce the balance of your IRA by $100,000, which will lower the amount you’ll need to take out for RMDs. The lower your RMD, the lower your income will be on that, which could significantly reduce the income tax you’ll owe.

QLAC Contribution Limits and Inflation Riders

You are now permitted to buy a QLAC for up to $200,000 from an eligible retirement plan. Previously, you were limited to whichever was lesser of $145,000 or 25% of your account balance. The current $200,000 upper limit is a combined cap that applies to all of your eligible retirement accounts, even if you take money from different accounts or purchase more than one QLAC. But if you and your spouse have your own eligible retirement accounts, then you can each spend up to the $200,000 limit on your own QLACs.

Since a QLAC locks in future payments, you are protecting your retirement money from market dips later in life. But unless you purchase an inflation rider with your QLAC, which will lower the initial amounts you receive from an annuity, your monthly payment may lose value over time.If you’re considering acquiring a QLAC, then you’ll want to work with a financial advisor to make sure you’re picking the right one.

Considering Your Spouse When Purchasing a QLAC

Some QLACs offer a survivor payout, also referred to as contingent annuity payments. These would continue your annuity payments to your designated beneficiary, which is usually a spouse, after your death. Other QLACs offer death benefits that would return any unused premiums to your beneficiaries through a lump sum or series of payments. If you have a spouse or individuals who will depend on your annuity after your passing, then you need to make sure any QLAC you choose has one of these features. Without these features in your annuity, your survivors would get nothing.

In addition to making sure your QLAC comes with a survivor payout or death benefit, you may also consider getting a joint QLAC with your spouse. If you’re married, a joint QLAC would provide income payments that continue for as long as one of you is alive. The only downside to choosing a joint contract is that it decreases your income payments, compared to a single life contract.

When a QLAC Isn’t For You

If you’re 65 and in poor health, you probably don’t want to wait until age 85 to start receiving income payments, so a QLAC may not benefit you at all. “If the probabilities are that you have a longer than average life expectancy, QLACs can be a windfall,” says Artie Green, a financial planner. “But if you have a shorter than expected longevity, of course, that works against you with any annuitization.” QLAC recipients can use their funds on whatever they want, but often they spend it on late-in-life health care or housing costs. The purpose of a QLAC is longevity protection that could minimize or even eliminate the risks of running out of money.

There are really only two scenarios in which a QLAC is a good fit. The first is if you have reached age 73 and do not need your RMDs to cover expenses. The second is if you think you’ll reach 73 and not have enough funds to pull from. QLACs can be a safeguard that guarantees you an income late in life, while also reducing your need for RMDs and even lowering your income taxes on them. At Insureyouknow.org, you may keep all of your financial and retirement planning in one place, making it easy for you to forecast and plan for your future.

Six Things to Know about SIMPLE IRA

April 30, 2024

Offering a SIMPLE IRA (Savings Incentive Match Plan for Employees) to employees is an effective way for small businesses to offer their employees a retirement plan. At a glance, this plan allows both the employer and employee to make contributions, and there are less reporting requirements and paperwork involved for the small business owner. Besides the ease in which these plans can be established for employees, the main perks are tax incentives for both the employer and the employee. “They are fairly inexpensive to set up and maintain when compared to a conventional retirement plan,” says client advisor at First American Bank Karina Valido. “For employers, contributions are tax-deductible. For participants, contributions and earnings are not taxed until withdrawn.”

Even though the SIMPLE IRA is a straightforward retirement option, here are six things to know about this plan, whether you’re an employer or an employee.

- Employee Contribution Limits in 2024

With a SIMPLE IRA, an employee can, but isn’t obligated to, make salary reduction contributions. In 2024, the maximum amount an employee under the age of 50 can contribute is $16,000. With a SIMPLE IRA, you may also contribute to another retirement plan as long as both contributions don’t exceed the yearly limit. The annual limit for combined SIMPLE IRA and 401(k) contributions in 2024 cannot be more than $23,000 or $30,500 for people who are 50 or older. Since an employer cannot offer both plans, this would only apply to those employees who held a previous account elsewhere.

- Employer Contribution Requirements

Employers must do one of two things: match employee contributions or make nonelective contributions. If an employer chooses to match each employee’s salary reduction contribution, they must do so by up to 3% of their employee’s compensation. While an employer may choose to match less than 3%, they must at least match 1% for no more than two out of five years. If an employer chooses to make nonelective contributions of 2% of the employee’s compensation, they must do so for every employee, regardless of having some employees who are making their own contributions. So if an employer chooses to make nonelective contributions, then they must also match the contributions of those employees who choose to contribute to their own plans.

- SIMPLE IRA Tax Advantages

For employees, salary reduction contributions to their SIMPLE IRA reduces their taxable income and their investments will grow tax-deferred over time. Because it’s a tax-deferred account, you won’t need to pay capital gains taxes when you buy and sell investments within the account. Plus, unlike many other retirement plans, such as a 401(k), employer contributions to a SIMPLE IRA are immediately vested and belong to the employee.

Employers also benefit from tax incentives with the SIMPLE IRA. They can get a tax credit equal to 50% of the startup costs, or up to a maximum of $500 per year, for three years. This credit is in addition to the other tax benefits they will receive from contributing to employee retirement plans.

- All About Withdrawals

During retirement, withdrawals will be taxed as regular income. Before the age of 59 ½, there’s a 10% penalty on withdrawals in addition to the income taxes you would owe. With the SIMPLE IRA, the withdrawal penalty rises to 25% if the money is taken out within two years of the plan being contributed to. Under qualified exemptions, like higher education costs or first home purchases, then you may avoid an early withdrawal fee, but you would still have to pay the taxes.

- Eligibility for SIMPLE IRAs

The Small Business Job Protection Act of 1996 created the SIMPLE IRA. It was designed with small businesses and self-employed individuals in mind and meant to be simple, accessible, and inexpensive. “A SIMPLE IRA is a small-business-sponsored retirement plan that, as the name indicates, is simple to establish and maintain,” explains financial advisor at Marsh McLennan Agency Craig Reid. “Available to U.S. companies with 100 or fewer employees, SIMPLE IRAs are a cost-effective alternative to the mainstream 401(k) plan.”

In order to be eligible for a SIMPLE IRA, an employer must have fewer than 100 employees and have no other retirement plan in place. They must also make contributions each year. For an employee to be eligible, they must receive at least $5,000 in compensation during any two prior years and expect to receive the same during the current year.

- The Difference Between SIMPLE IRA and SEP-IRA

Both a Simplified Employee Pension (SEP-IRA) and a SIMPLE IRA are employer-sponsored retirement plans that offer employees a tax-advantaged way to save for their retirement. Contributions in each grow tax-deferred until they are withdrawn during retirement. They are each designed to be easily established in small businesses, especially when compared to a 401(k).

One key difference between the two plans is that while a SIMPLE IRA allows both the employer and employee to make contributions, the SEP-IRA only allows the employer to contribute. The SEP-IRA, though, does allow higher contributions, which will be limited to $69,000 in 2024, compared to $16,000 in 2024 for the SIMPLE IRA. The other main difference between the two plans is that any employer can offer a SEP-IRA, while only businesses with less than 100 employees qualify for offering the SIMPLE IRA.

If you’re a self-employed individual, a small business owner, or you have recently begun working for a small business that offers you a SIMPLE IRA, it will benefit you to know the upsides of having one and understand the rules around the plan. With Insureyouknow.org, you can store all of your financial information and records in one place so that you may stay organized and allow yourself the best decision-making process in your retirement planning.

Navigating the Impact of Recent Real Estate Legislation

April 15, 2024

During March of this year, the National Association of Realtors (NAR) reached a settlement agreement to resolve a series of lawsuits that had to do with the practice of tying. Tying involves the home seller’s agent setting a commission rate for that homebuyer’s agent if they help facilitate a sale. According to the NAR, 90 percent of the homes on the market in the United States are sold this way as they are listed on the Multiple Listing Service (MLS).

Each year, Americans pay $100 billion in real estate agent commissions. If the settlement is accepted, the new terms may lower the amount agents can collect in home transactions. Since the proposed rules may change how U.S. homes are bought and sold, the new terms are important for realtors and potential homebuyers to understand.

The Problem With Tying

MLSs aren’t new, as the first MLS began in the late 1800s as a way for real estate agents to share information about the properties they were trying to sell. In exchange for the sharing of information, the agents agreed to compensate other brokers who helped them sell their properties. Today, more than 800 MLSs exist where agents list their properties. Sellers benefit from this arrangement because of increased exposure of their properties, while buyers benefit because they receive a database of nearly every home on the market.

The practice of tying, when the buyers’ agent is offered a commission for facilitating the sale of another agent’s property listing, has been shown to reduce competition and drive-up closing fees. Under tying, the commission the buyer’s agent will receive is determined before that agent can actually provide any services to the buyer. This can make it difficult for the home’s buyer to negotiate closing fees as well as require the home’s seller to offer higher commissions in order to sell their home.

Because real estate agents earn their income through these commissions, they are widely known to practice steering, which involves directing their clients toward homes that offer the best possible commissions for themselves. Since only one in 600 MLSs allow their agents to publish the commission they offer to buyers’ agents, buyers are generally unaware of these agreements between agents. The lack of transparent commission agreements makes it difficult for a buyer to know if their agent is steering them away from certain properties.

What the NAR Agreement Would Entail

If the proposed NAR settlement is approved, there will be two significant changes to prevent tying. First, MLSs will not be permitted to display commission rates. Commissions however can still be negotiated through real estate professionals off-MLS. Second, real estate agents will have to explicitly agree to the exact services they’ll provide their clients through written agreements, which will be known as a Buyer Representation Agreement and will include the agreed upon compensation for the realtor. If the changes are accepted, they will go into effect mid-July. Because of this, many realtors are suggesting those who are currently looking to buy to close by the end of June in order to avoid these proposed changes to the homebuying process.

Nearly every realtor who is a NAR member is covered in the agreement, and every member would have to abide by the proposed changes if the settlement is approved. Any members of HomeServices of America would not be covered due to ongoing court cases, as well as any brokerage firms with residential transaction volume above $2 billion in 2022. Any realtor who is unsure if they are involved in the changes or have questions moving forward are urged to get their information from the NAR’s facts.realtor.

What to Know About Traditional Commission Rates

The typical U.S. sales commission rate for real estate agents is five-to-six percent, which are among the highest in the world. But agents have been advertising low-to-zero percent commission rates to appeal to buyers for years. This isn’t because they’re foregoing their profit, but because they’re rewording their commission rate as “buyer credits.” Buyer credits can already be seen offered on many listings and are determined as the buyer sees fit at closing. In other words, commission rates and agent profits have already been negotiated outside of the MLSs for some time now. That’s why many futurists predict that these new guidelines will affect the future of real estate very little.

Because agent compensation will become a negotiation, many predict increased competition among agents, which the practice of tying had reduced for some time. “Fees have been a bit rigid,” said San Diego Real Estate Professor Dr. Norm Miller. “So it is about time we see more price competition on the fee side.” At the average U.S. home price $420,000, a six percent agent commission would be $25,200. If that six percent rate is reduced by half to three percent due to agent competition, then the price to sell or buy a home could be reduced to $12,600. Clearly, that could make buying a home more affordable for many.

The Future of Real Estate

If the settlement is approved, the practices of tying and steering will likely end. Hopefully, homebuyers will be able to better negotiate the amount of commission their agent will receive or choose alternative forms of payment, such as paying by the hour or a flat fee. Homebuyer’s should also be less pressured to list their home through MLSs or use an agent at all. All of this could result in lower costs of housing transactions, but the full extent isn’t clear.

The overall effect on the economy is difficult to predict. The NAR settlement agreement would benefit middle-class families who have a large share of their wealth invested in housing. Because consumers typically share a small amount of their gains in wealth, the benefit to middle-class homeowners who sell their property is unlikely to make an influence on consumer demand. Other economists predict that the process of buying a home could involve more upfront costs if real estate agents begin foregoing commission rates, which could potentially make it less feasible for lower-income and first-time buyers to acquire property.

If you’re in the market for buying a home, the expected changes due to the impending NAR settlement may end up affecting you very little. Besides being able to negotiate your agent’s fees and services upfront, very little is expected to change as a result of the new guidelines. At the end of the day, if you decide to use an agent when buying or selling a home, you’ll want to choose a professional you trust, regardless of these changes. Insureyouknow.org will prove to be a valuable tool in the homebuying process, as you can store all of your financial information and agreements in one easy to access place.

2024 Changes that Would Impact Your Retirement Finances

April 1, 2024

Changes to retirement regulations are making 2024 out to be the perfect time to reexamine your retirement planning and make sure you’re getting the most out of your savings.

“The rules are constantly changing,” says director of Personal Retirement Product Management at Bank of America Debra Greenberg. “It’s always a good idea to familiarize yourself with what’s new to see whether it makes sense to take advantage of it.”

Here’s what you should know about several changes to retirement regulations in 2024.

It Pays to Plan for Retirement

While the changes to retirement regulations may seem small, Americans need all the help they can get right now. According to the National Council on Aging, up to 80% of older adults are at risk of dealing with economic insecurity as they age, while half of all Americans report being behind on their retirement savings goals.

“The IRS adjusts many things each year to reflect cost of living and inflation,” says Jackson Hewitt’s chief tax information officer Mark Steber. “It happens each year and taxpayers shouldn’t be alarmed — they might even have a bigger benefit.” Since retirement contributions are pre-tax, saving for retirement actually lowers your taxable income, which may even place you into a lower tax bracket. Plus, you may even be eligible for a tax credit of up to 50% of what you put into your retirement accounts.

Contribution Limits Will Increase

The contribution limits for a traditional or Roth IRA are increasing in 2024. The limit on annual contributions to an IRA will go up to $7,000, up from $6,500 last year.

Individuals will be able to contribute more to their 401(k) and employer-based plans as well. For those who have a 401(k), 403(b), most 457 plans, or the federal government’s Thrift Savings Plan, the contribution limit is increasing to $23,000 in 2024, which is $500 more than last year. Those who are 50 and older, can contribute up to $30,500 into the same accounts.

Starter 401k Plans are Possible

In 2024, employers who don’t sponsor a retirement plan may offer a Starter 401(k) deferral-only arrangement. A starter 401(k) is a simplified employer-sponsored retirement plan with lower saving limits than a standard 401(k). Employers are not allowed to make contributions, and employee auto-enrollment is required. In 2024, the annual contribution limit to this plan will be $6,000. Beginning this year, employees with certain qualifiable emergencies may also make penalty-free withdrawals from their 401(k) of up to $1,000, though they would still have to pay the income tax on those withdrawals.

529 Plans Can Now be Converted Into Roths

For parents who will no longer need their 529 funds for their children, the Secure 2.0 Act will allow for a portion of the 529 to be rolled into a Roth IRA. Beginning January 1st, the funds can either be used for educational expenses or put toward retirement, as a Roth IRA rollover. You may rollover up to $35,000, free of income tax or any tax penalties. The only limitations are that the 529 must have been in place for at least 15 years, and certain states may not allow the rollover.

Changes to Social Security and RMDs

In January, Social Security checks will increase by 3.2% due to the latest COLA, or cost-of-living adjustment. On average, Social Security monthly benefits will increase by $59 a month, from $1,848 to $1,907. Those who receive survivors or spousal benefits will receive even more.

For 2024, the maximum benefit for a worker who claims Social Security at FRA (Full Retirement Age)is $3,822 a month, which is up from $3,627 in 2023. For 2024, the FRA is 66 years and 6 months for those born in 1957 and 66 years and 8 months for those born in 1958. That means that anyone born between July 2, 1957 through May 1, 1958 will reach FRA in 2024.

The IRS uses a calculation based on the amount in your retirement account and your life expectancy to determine the minimum amount you are required to take out each year, known as RMDs (required minimum distributions). Secure 2.0 increased the age for starting RMDs from 72 to 73, effective in 2023. If you are subject to RMDs, then you must make your withdrawal by the end of this year or by April 1st next year if it’s your first year being eligible. So if you turn 73 in 2024, you’ll have until April 1, 2025 to make your first RMD.

Anyone receiving more Social Security but paying Medicare premiums may not feel much of a difference in their increased Social Security benefits since standard Medicare Part B premiums are rising by 6%. As many participants have their Medicare premium deducted right from their Social Security payment, the $9.80 increase will take a portion of the average $59 benefit increase. The annual deductible will also increase this year from $226 to $240.

Insureyouknow.org It will always be important to review your retirement savings every year, but this is becoming even more important to do in the face of rising costs and changing regulations. With Insureyouknow.org, storing all of your financial information in one easy-to-review place can help you ensure that you are still on track to meet your retirement goals at the start of each annual review.