Category: End-of-Life Planning

Sandwich Generation Guide: Organize Parents’ & Kids’ Records

January 8, 2026

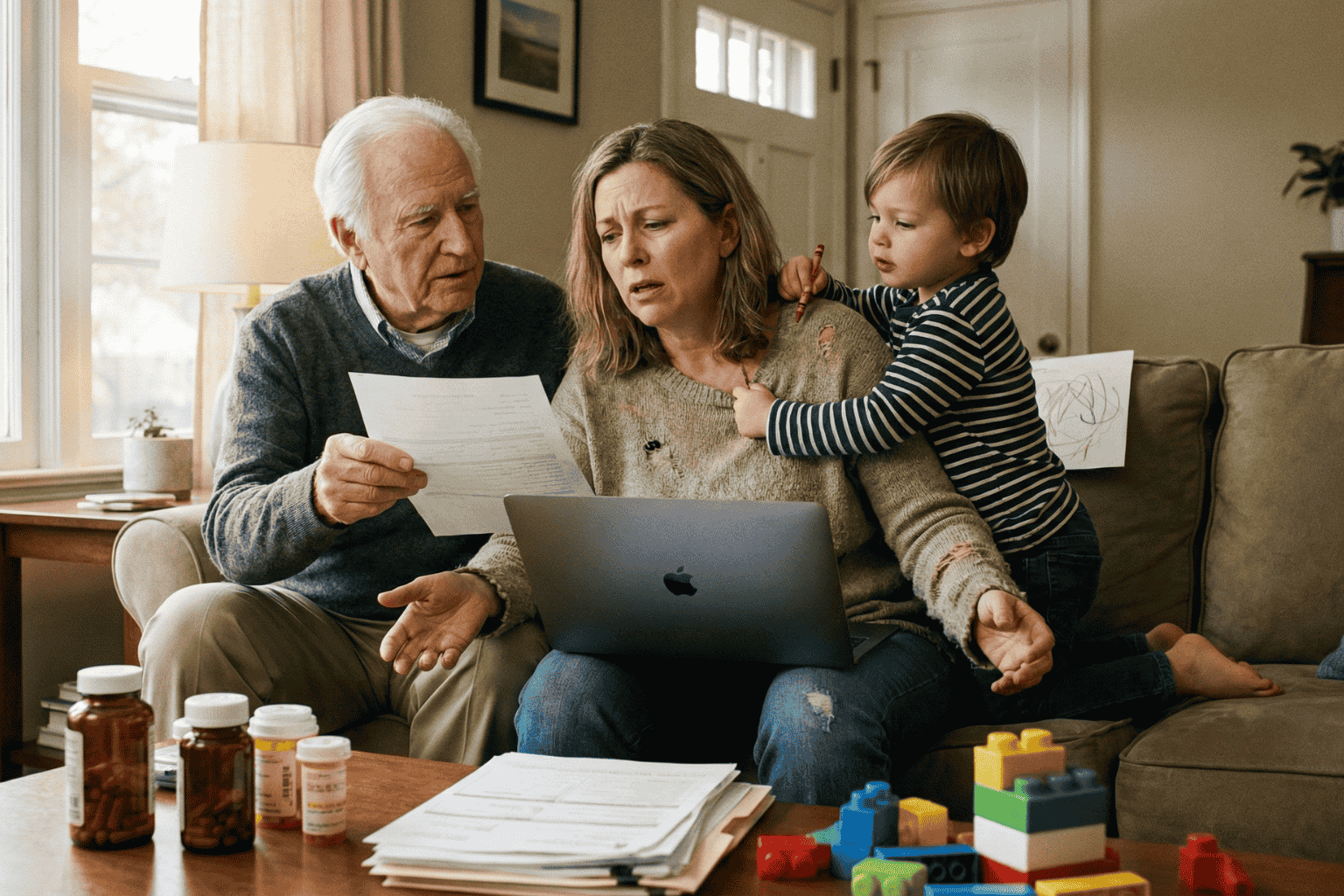

The Squeeze is Real

The term “Sandwich Generation” sounds polite, almost clinical. But for the millions of adults living it, the reality feels a lot more like a pressure cooker. They are squeezed tight. On one side, there are children needing help with homework, permission slips, and growing pains. On the other, aging parents need support with doctors, medications, and a lifetime of accumulated paperwork.

It is exhausting.

The hardest part usually isn’t the physical caregiving. It is the administration. It is being the unpaid, overworked secretary for two different households. One minute, a parent is hunting for a vaccination card for summer camp; the next, they are frantically searching for Mom’s Medicare supplement number because a receptionist is waiting on the line.

When these worlds collide, chaos wins. Unless, of course, there is a system in place.

Two Households, One Overloaded Brain

The main problem isn’t a lack of effort. It is a lack of centralization. The “Sandwich” caregiver is trying to run two different operating systems at once.

Consider the children. Their documentation is constant and urgent:

- Social Security cards (usually lost in a drawer somewhere).

- Immunization records that schools demand every September.

- Birth certificates for sports or travel.

Then look at the parents. Their paper trail is decades long and much heavier:

- Wills, Trusts, and Deeds (often hidden in “safe” places that no one can find).

- Complex lists of daily medications.

- Insurance policies that need to be renewed.

- The dreaded “In Case of Emergency” contacts.

Keeping the kids’ files in a backpack and the parents’ files in a dusty filing cabinet across town simply doesn’t work. Not in 2026. When an emergency happens, and they always happen at inconvenient times, nobody wants to be driving across town to find a piece of paper.

The “Kitchen Table” Talk

Getting organized starts with a conversation, not a scanner. This is the tricky part. Many adults feel awkward asking their parents about wills or bank accounts. It feels intrusive.

But the conversation doesn’t have to be about control. It should be about safety. The approach matters. Framing it as, “We need to make sure the doctors know what you need if you can’t tell them,” works a lot better than, “Give me your passwords.”

The goal is strictly practical: preventing a crisis from becoming a disaster.

Cut the Clutter: What Actually Matters?

A common mistake is trying to save everything. But honestly, nobody needs to digitize a utility bill from 1998. To survive the squeeze, caregivers need to be ruthless about what they keep.

The “Must-Have” list is actually quite short:

- The Legal Shield: Power of Attorney. This is non-negotiable. Without it, an adult child is legally a stranger to their parent’s bank or doctor.

- The Medical Snapshot: A simple, updated list of what pills they take and who their primary doctor is.

- The Money Trail: Just a list of where the accounts are. Not necessarily the balances, but the locations of the banks and insurance policies.

Stop Relying on Physical Folders

Paper is fragile. It burns, it tears, and most importantly, it stays in one place.

If a parent falls ill while the caregiver is on vacation, that physical folder in the hallway closet is useless. This is why moving to a digital system is the only logical step for a modern family.

Using a secure, encrypted platform, like InsureYouKnow.org, solves the geography problem. It puts the information in the cloud, protected by encryption that is tougher than any lock on a filing cabinet. It means the right information is available on a smartphone, right in the hospital lobby, exactly when it is needed.

Don’t Go It Alone

There is a hero complex in the Sandwich Generation. Everyone tries to carry the load solo. But that is a recipe for burnout.

Once the records are digital, they should be shared. A spouse, a reliable sibling, or a family attorney needs access, too. Modern digital vaults allow for this kind of “trusted partner” access. It ensures that if the primary caregiver gets the flu or gets stuck in a meeting, someone else can step in and handle the situation.

Finding Some Peace

At the end of the day, organizing these records isn’t really about paperwork. It is about buying back time.

Every minute saved by not hunting for a lost insurance card is a minute that can be spent actually being a parent or a son or daughter. The paperwork will always be there, but the stress doesn’t have to be. By merging these two chaotic worlds into one secure place, the Sandwich Generation can finally take a breath.

How to Choose a Medical Power of Attorney and Stay Prepared

November 6, 2025

A few years ago, a close friend of mine went through something that completely changed how I look at “being prepared.” Her dad had a stroke while working in the garden. One minute he was watering plants, the next, he was in the hospital, unable to speak. The doctors were asking who could make medical decisions for him, but no one had an answer. Everyone froze.

It was heartbreaking to watch. Her mom was in shock, her siblings were arguing, and everyone was scared. Nobody knew what he would have wanted.

That day taught me something that I’ll never forget. Planning ahead isn’t just about being responsible. It’s an act of love. And that’s exactly what a Medical Power of Attorney is all about.

What a Medical Power of Attorney Really Means

A Medical Power of Attorney (MPOA) sounds like a complicated legal thing, but it’s actually simple. It’s a document that lets you choose someone you trust to make healthcare decisions if you can’t.

That person, your agent, doesn’t suddenly take over your life. They only step in if you can’t speak for yourself. Their role is to protect your wishes and make sure what you want actually happens.

It’s one of those things we tend to put off, but once it’s done, it brings a quiet kind of comfort. You know things will be okay, even if you can’t explain what you want in the moment.

Why It Matters

If you don’t have a Medical Power of Attorney, hospitals usually turn to whoever’s nearby or follow state laws about next of kin. That can work, but it can also cause a lot of tension. In stressful moments, people don’t always think clearly. They guess, they argue, they panic.

Having an MPOA avoids all that. It gives doctors one clear person to speak with and gives your family direction when things feel uncertain. It’s a simple form, but it can prevent a lot of heartache later.

How to Choose the Right Person

Choosing your agent isn’t about who’s closest to you. It’s about who knows you best. The person you trust most doesn’t have to be family. It could be a friend, a sibling, or someone who simply understands you.

Here’s what to think about:

- Who stays calm under pressure?

- Who knows how you feel about medical care and quality of life?

- Who will listen to doctors carefully and ask good questions?

- Who will do what you want, even if others disagree?

Once you decide, talk to them. It doesn’t need to be formal or serious. Maybe just bring it up during a car ride or while cooking dinner. Tell them how you feel about certain treatments or what kind of care you’d want. These honest conversations matter so much more than any form.

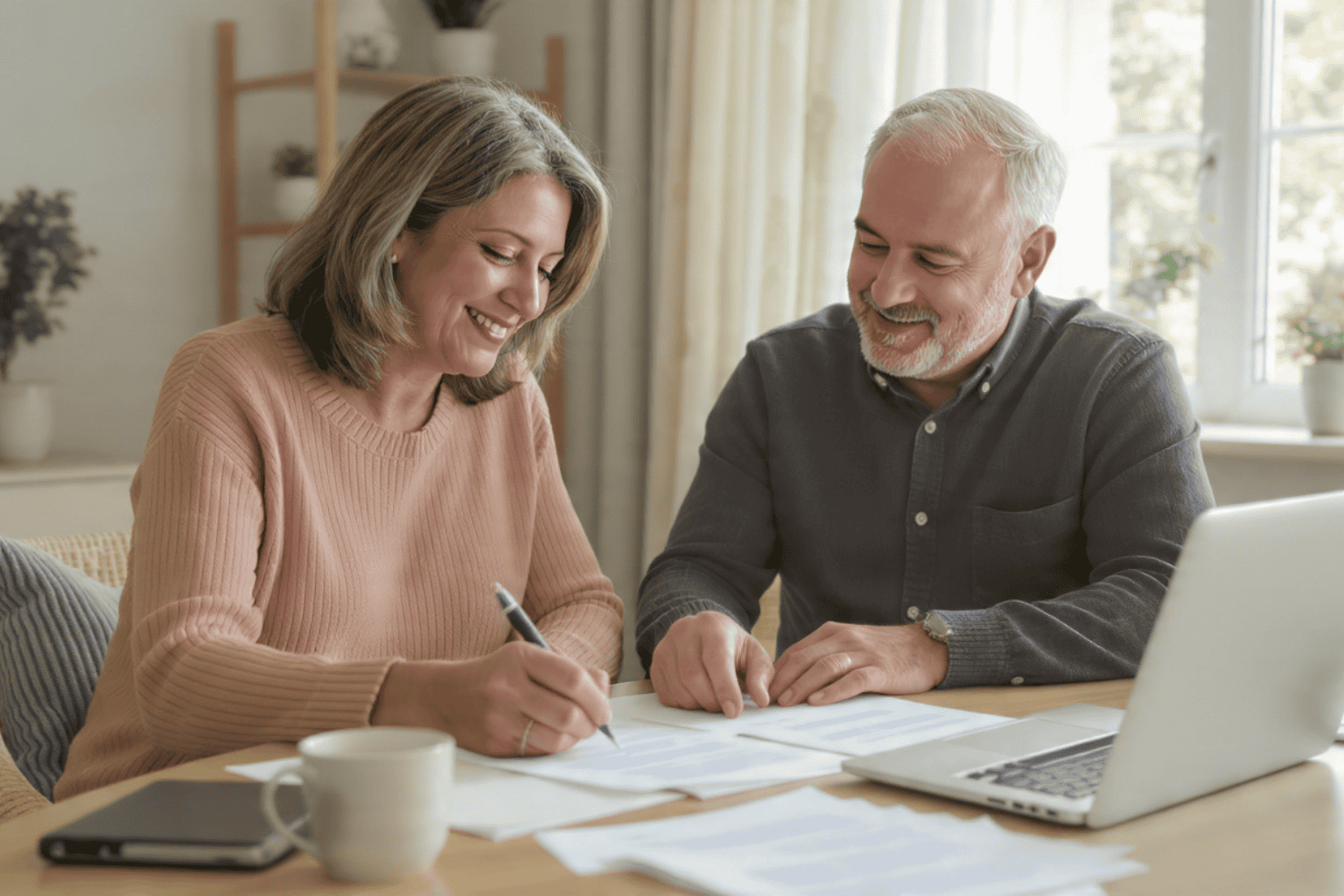

Keeping Your Documents in Order

Once your form is signed, keep it somewhere easy to find. In an emergency, no one wants to dig through stacks of paper.

Here’s what to keep together:

- Your MPOA form (signed and dated).

- A Living Will or Advance Directive describing your medical preferences.

- A HIPAA release form so your agent can speak with doctors.

- Health insurance cards and policy info.

- Emergency contacts for family and doctors.

- Photo IDs for you and your agent.

I like to keep mine in a labeled folder at home and another copy saved online. It’s one of those “just in case” things that saves everyone stress later.

Why Digital Storage Helps

Paper gets lost. It gets packed in a box or tossed by accident. That’s why having a digital copy is smart.

A secure site like InsureYouKnow.org makes it easy to upload and store important documents safely. You can label them, share access with your agent, and know that if you ever need them, they’re right there. It’s simple, private, and safe.

It’s not about being tech savvy, it’s about being practical.

Keep It Updated

Life changes. People move, relationships shift, new doctors come into your life. Once a year, take five or ten minutes to check that your MPOA and other forms are still up to date.

It doesn’t take long, but it gives you peace of mind that everything’s current.

A Final Thought

Setting up a Medical Power of Attorney isn’t about expecting bad things to happen. It’s about kindness, for yourself and the people who love you.

Once it’s done, you can stop worrying. You’ll know that, no matter what happens, your family won’t be left guessing. They’ll already know because you cared enough to prepare.

It’s not just a document. It’s peace of mind, and maybe one of the most loving things you can do.

Love in the Final Chapter: Caring for a Loved One in Home Hospice

October 15, 2025

When it comes to end-of-life care, 71% of Americans believe the goal should be to help people die without pain, discomfort, and stress. The focus of hospice care is on quality of life and symptom management, and it is designed to provide comfort to individuals with a life expectancy of six months or less.

A team of medical professionals addresses the patient’s physical, psychological, and spiritual needs on a case-by-case basis, ensuring that every patient receives a care plan tailored to their specific needs. Care is most often delivered in the patient’s home, and the hospice team can support caregivers during this process.

Quality is Key

Hospice is end-of-life care, but that doesn’t mean someone receiving care will pass right away. While doctors recommend hospice when a patient only has six months or less to live and is no longer responding to curative treatments, many patients live longer. In such cases, what matters still is a patient’s quality of life, not quantity.

“Each person’s journey at the end of life is different,” says Jessica Kelly, a licensed hospice nurse in New York. “We tailor our care to meet those unique needs, whether that’s managing pain, supporting emotional well-being, or helping families share meaningful moments together.”

Home Care Takes a Toll

While it is nearly everyone’s preference to pass away in the comfort of their own home, the task of caregiving can be more than loved ones expect. “I do think that when patients are at home, they are in a peaceful environment,” says Parul Goyal, a palliative care physician. “It is comfortable for them. But it may not be comfortable for family members watching them take their last breath.”

The burden put on loved ones, especially spouses, can cause caregiver syndrome, which is characterized by the stress and burnout that comes from providing constant care to someone who is chronically or terminally ill.

“Our long-term-care system in this country is really using families, unpaid family members,” says Katherine Ornstein, a professor of geriatrics and palliative medicine at Mount Sinai. “What we really need to do is to broaden the support that individuals and families can have as they’re caring for individuals throughout the course of serious illness.”

Self-Care for Caregivers

Providing care to a hospice patient can be both rewarding and difficult. Social psychology researchers Richard Schulz and Joan Monin found that caregivers suffer when they witness their loved one’s suffering without feeling like they can remedy it. It becomes important not just to care for the patient but for caregivers to care for themselves as well.

One way to start accepting a terminal diagnosis is to begin getting a loved one’s affairs in order. It can be helpful to collect necessary documents and passwords and to begin sorting through possessions. Staying busy during the care process can help manage emotions as they arise.

Handling Grief

It’s easy to get paperwork and belongings in order. It’s not as easy to manage your grief. The loss of a loved one is among life‘s most significant stressors. Grief can affect every aspect of your health. While everyone’s experience is different, it is common to feel intense emotions during a loved one’s illness and after losing them.

Here are ways caregivers can take care after loss:

- Express your emotions. Bottling them up will only intensify them.

- Don’t put yourself on a timeline. People move forward at their own pace. Trust that your pain will lessen over time.

- Take care of yourself as you grieve. Eat nourishing meals, stay hydrated, and sleep enough.

- When you’re ready, exercise. It can reduce stress, tension, and sadness.

- Hospice providers make grief support groups available to anyone who has lost a loved one in hospice care.

- The Hospice Foundation also offers a newsletter to help during bereavement.

When to Seek Help

Most people find a way to adjust to their loss, but it is a painful and uncomfortable process. About 10% to 15% of people who are grieving have a complicated reaction to their loss. Grief experts agree that if grief is unmanageable, meaning someone has not returned to their pre-loss level of functioning within six to 12 months, it may be time to seek the professional help of a grief counselor. Your hospice team can help you find the care you need.

Handling a loved one’s affairs is one way caregivers can manage their grief. With Insureyouknow.org, you may organize financial documents, property records, and other documentation of personal effects. Getting everything in order can bring you some peace of mind during emotionally challenging times.

10 Things to Know About Beneficiary Designation

October 1, 2025

When people think about estate planning, they often focus on wills, trusts, and last wills and testaments. But one of the most powerful tools you already use, and might be overlooking, is beneficiary designation. These designations on life insurance policies, retirement accounts, and payable-on-death (POD) or transfer-on-death (TOD) accounts determine exactly who receives those assets, often outside the probate process.

The Department of Labor estimates that 15% to 40% of beneficiary designation forms contain errors that can delay or even prevent an inheritance from being received. Even worse, mistakes are common: a 2023 survey by MassMutual found that one in five Americans has never updated beneficiaries after significant life changes such as marriage, divorce, or the birth of a child.

“Beneficiary designations are powerful legal documents that override what your will may say,” says Christine Benz, Director of Personal Finance at Morningstar. “If you don’t review them regularly, you may unintentionally disinherit your loved ones.”

Here are ten essential things you should know about beneficiary designations.

1. Beneficiary designations often override your will

Assets with beneficiary designations usually pass outside probate and independently of your will. That means if your will leaves “everything to my children” but your life insurance still names an ex-spouse, the ex-spouse will likely inherit those funds.

2. Always name both primary and contingent beneficiaries

Without a contingent beneficiary, if the primary beneficiary predeceases you, the account may revert to your estate and go through probate. “Naming backups ensures your wishes are carried out even if life takes unexpected turns,” says David Frederick, Director of Client Success at First Bank Wealth Management.

3. Use precise, unambiguous language

Simple errors — misspelled names, missing dates of birth, or vague terms like “my children” — can delay distributions or spark disputes. Include full legal names and identifiers wherever possible.

4. Be careful naming minors or vulnerable beneficiaries

If you leave money directly to a minor, a court may appoint a guardian to manage the funds on their behalf. Likewise, naming a person with special needs may jeopardize their eligibility for government benefits. In these cases, a trust is often the safer route.

5. Update after significant life changes

Marriage, divorce, births, or deaths all require updates to your designations. A 2022 Fidelity report found that more than 30% of account holders had an ex-partner still listed as a beneficiary. “Life changes — and your beneficiary designations need to change along with it,” says Jina Etienne, CPA and estate planning educator.

6. Avoid naming your estate as a beneficiary

Although allowed in some settings, naming your estate as a beneficiary usually negates many of the advantages of beneficiary designation — primarily, probate avoidance. If the asset passes through your estate, it may be subject to probate, court costs, delays, and potential claims by creditors. It could also accelerate taxation in certain retirement accounts. For example, when an estate is the beneficiary of an IRA, required distributions must be completed within five years.

7. Understand tax implications

Beneficiary designations don’t just control who receives assets — they also shape how they receive them. Under the SECURE Act, most non-spouse beneficiaries must withdraw inherited retirement accounts within 10 years. That rule can create significant tax burdens if not carefully planned for. Trusts and other strategies can help distribute assets more tax-efficiently, but they need to be set up correctly.

8. Double-check execution and form requirements

Completing a beneficiary designation form isn’t just about writing a name — it’s a legally binding document, often requiring strict adherence to formatting, signatures, spousal consents, and deadlines. The Department of Labor report highlights that paper forms have “a 15 % to 40 % error rate” (e.g., incomplete, unsigned, ambiguous). Some plans also require spousal consent before naming another beneficiary. Always verify that the financial institution has accepted and recorded your form.

9. Coordinate across all accounts

Each account has its own beneficiary designation form. Be sure they all align with your overall estate plan. “I often see people update their will but forget to check their 401(k) or IRA,” says Megan Gorman, Founder of Chequers Financial Management. “The result can be uneven distributions that don’t match the person’s intentions.” Here are a few coordination tips:

- When changing a will or trust, revisit every beneficiary form to ensure alignment.

- Avoid naming different children or percentages on different accounts unless it’s intentional. Over time, account balances may diverge, leading to unintended disparities.

- If you plan to leave assets to a trust, confirm the trust is drafted correctly to qualify as a “see-through” trust under IRS rules.

- Do not assume default designations by financial institutions will honor your wishes — they often won’t.

10. Communicate your decisions

Even properly completed forms can cause confusion if no one knows they exist. Tell beneficiaries or your executor where to find documents and how to access accounts. “Don’t assume people will know where your papers are kept,” says Anthony Burke, Senior Director at MetLife. “Clear communication reduces stress and delays for your loved ones.” Additionally, including a cover memo or letter of explanation can help reduce delays or confusion among beneficiaries or administrators.

Beneficiary designations may look simple — just a name or two on a form — but their implications are anything but trivial. From accidentally leaving assets to an ex-spouse to triggering costly tax consequences, mistakes can easily undermine your best intentions.

Insure You Know

If you haven’t reviewed your designations lately, now is the time. At Insure You Know, we believe smart insurance and estate planning go hand in hand. Taking a few minutes today to update your beneficiaries can spare your family confusion, conflict, and financial hardship tomorrow.

What Happens to Your Digital Assets After You Die?

September 24, 2025

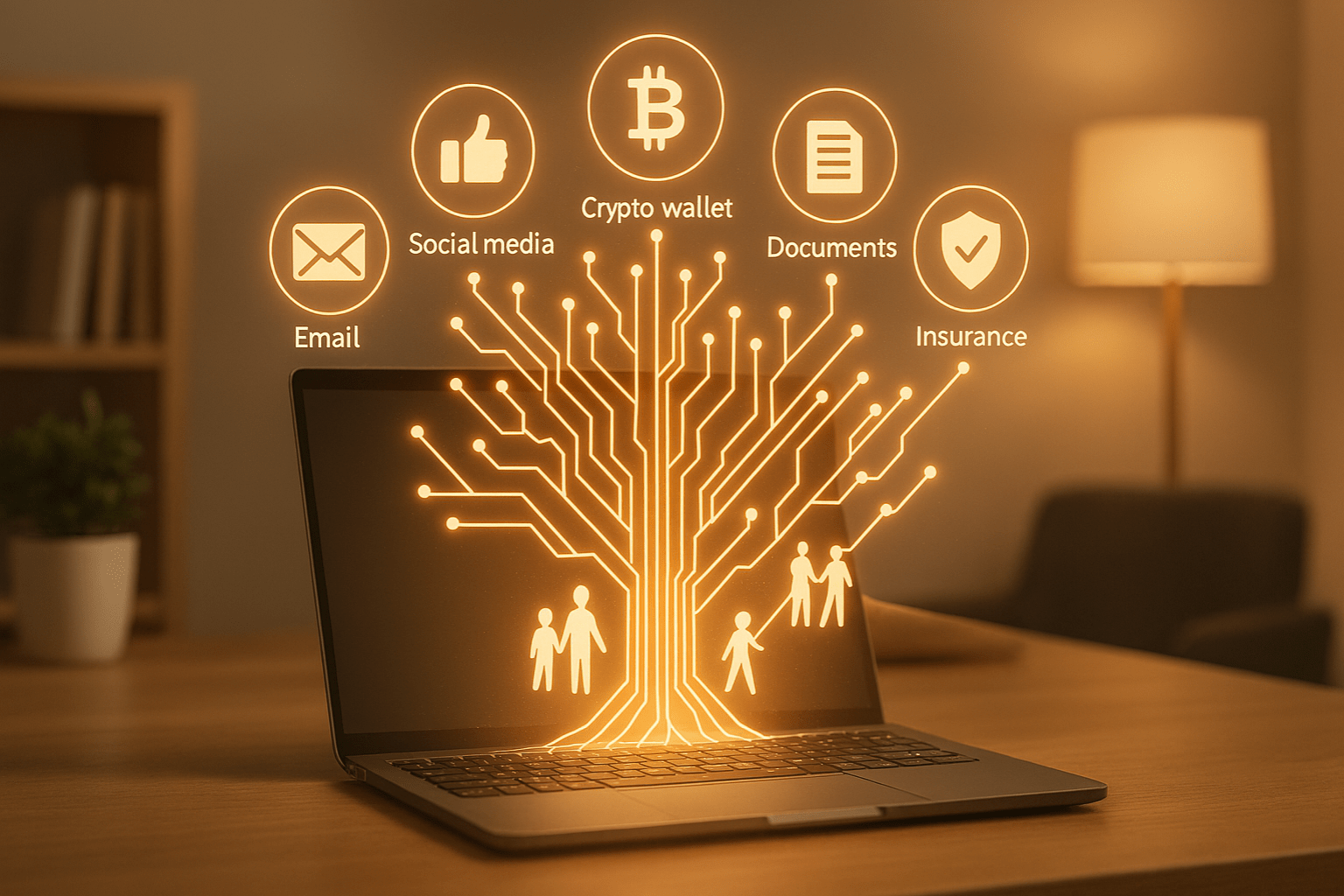

We spend so much of our lives online that it’s easy to forget just how much we’ve tucked away in digital spaces. Photos on Google Drive. A lifetime of emails. Bank apps, crypto wallets, even the music and books we’ve bought but never actually “own.” All of these things add up to what people now call your digital assets.

The tricky question is: what happens to them when you’re no longer here?

A Hidden Part of Your Estate

Think about how a traditional estate works. You leave a house, some savings, maybe a car, and your family knows how to claim those things. But with digital property, it is different. Passwords lock things up. Privacy laws keep companies from handing over your accounts. In many cases, providers do not even recognize heirs unless you have given explicit permission.

That means your online life, all those accounts and files, might just sit there untouched. Some platforms will eventually delete them. Others freeze them in time. And unless someone has the right access, even valuable things like cryptocurrency can disappear forever.

Why Families Struggle

It is easy to imagine the problems. Maybe your daughter knows you kept all the family photos in your Google account but cannot get past the two-factor authentication. Or perhaps you held a few thousand dollars in a crypto wallet that requires a private key only you knew. Even something as simple as canceling a subscription can be a nightmare if nobody has your login.

The result? Frustration, wasted time, and sometimes permanent loss.

The Law and the Fine Print

Adding to the confusion are the laws and service agreements. In many places, executors do not automatically get digital access. US states that follow a law called RUFADAA allow it only if you have given written consent, usually in your will. Big tech companies add another layer: Google lets you set up an Inactive Account Manager, Facebook has legacy contact settings, and Apple has its own Digital Legacy program. If you do not turn those on, your family may have no options.

So between legal barriers and tech restrictions, the default outcome is often nothing happens and accounts remain locked away.

How You Can Plan Ahead

The solution is not complicated, but it does take a little thought:

- Make a list of important accounts. It does not have to be detailed, but your family should at least know what exists.

- Decide who should handle them. Pick someone you trust and tell them they will be your digital executor.

- Write it into your will. A line or two giving that person authority can make a big difference.

- Use built-in tools. Set up legacy contacts where available. It only takes a few minutes.

- Keep access information safe. A password manager with emergency access, or a sealed note in a safe, works better than trying to share details in casual ways.

The key is to make sure someone you trust knows how to act when the time comes.

One practical way to protect your digital legacy is by using a secure service like InsureYouKnow. It allows you to store important documents, account information, and passwords in a safe, encrypted digital vault. You can control who has access and receive reminders to keep your records up to date, making it easier for your loved ones to manage your digital assets according to your wishes.

Why It Matters

Digital assets are not just about money. Sure, cryptocurrency or an online business can carry real financial weight, but the sentimental side matters just as much. Family photos, voice notes, or personal letters stored in an inbox can be treasures to those you leave behind. Without a plan, those things may vanish into the cloud forever.

By setting aside an hour or two to prepare, you can spare your loved ones unnecessary stress and give them access to the parts of your life that matter most.

Digital Inheritance: Secure Your Online Legacy with InsureYouKnow

August 13, 2025

Think about how much of your life now lives online. Photos you never printed. Banking and insurance details you don’t keep in a filing cabinet. Emails, social media posts, maybe even a bit of cryptocurrency sitting in a digital wallet. It is all part of your story, and it does not just disappear when you do.

That is why digital inheritance matters. It is about making sure the people you trust can find and use what you leave behind, without having to play password detective or deal with frustrating account lockouts.

In the next few minutes, we will explore how to put a plan in place for your online life, and how a secure tool like InsureYouKnow.org can help you create a well-organized digital legacy your loved ones can actually access when it counts.

What Constitutes Digital Assets

When you think about what you own online, it is probably more than you realize. There are the obvious things like your insurance papers, bank records, medical files, and maybe a scan of your driver’s license sitting in a folder somewhere.

Then you have your accounts. Email, social media, streaming logins, and online banking all hold bits of your life, whether that is photos from years ago or details about your finances.

And do not forget the paid stuff. Cloud storage plans, memberships, crypto wallets, or payment apps like PayPal. Some of it has sentimental value, and some of it is worth real money.

Figuring out exactly what you have is step one in digital estate planning, and it makes life much easier for the people who will need to handle things later.

Risks of Digital Legacy Without Proper Planning

Not thinking about your digital stuff after you’re gone can really cause headaches. Sometimes you can’t get into accounts at all, and all those photos or important files? They might just disappear.

Hackers or scammers could also sneak in. They might use your info, drain money from digital wallets, or mess with accounts in ways that are hard to fix.

And honestly, it’s a lot for your family. They could spend hours digging for passwords, calling different companies, or trying to figure out what belongs where — all while they’re already dealing with grief.

Just taking a little time now to plan your digital estate can save a ton of trouble later and make sure the people you care about aren’t stuck sorting through a mess.

How InsureYouKnow.org Helps

Keeping track of all your digital stuff can be a pain, you know? InsureYouKnow.org makes it kind of simple. You just toss all your important docs, passwords, whatever, into one safe spot. You get to decide who sees what.

And if something happens, a family member can just log in and grab what they need. No digging through emails. No guessing passwords. Way less stress.

Honestly, it just makes your digital life easier and ready for your loved ones when it counts.

Best Practices in Preparing Your Digital Legacy

You know, getting your digital stuff in order now can save a lot of headaches later. Start by listing all your accounts and assets — emails, social media, bank stuff, subscriptions, crypto, everything.

Use password managers or secure lockers to keep logins safe. Also, jot down who should access what and how, and store it somewhere safe.

Finally, think about adding instructions in your will or estate plan. That way, your family can handle your digital life smoothly and without stress.

Step-by-Step Action Plan

Getting your digital stuff in order doesn’t have to be complicated. Here’s a simple way to do it.

- Make a list – Write down all your accounts, subscriptions, documents, crypto wallets… basically everything. Group them so it’s easy to see.

- Keep it safe – Store passwords and important docs in InsureYouKnow’s secure vault. That way, it’s all in one place and protected.

- Pick someone you trust – Decide who can access what. Set clear permissions so they know what’s theirs to handle.

- Check and update often – Things change, you know? Make a habit of reviewing your list regularly.

Doing this makes your digital life organized, safe, and way easier for your family when they need it.

Real-Life Scenario

Imagine this: Sarah had been using InsureYouKnow.org to organize her digital life. She had all her accounts, documents, and login info stored securely, and she’d assigned her brother as her digital heir with clear permissions.

When Sarah unexpectedly passed away, her brother didn’t have to hunt for passwords or guess what to do. He simply accessed the secure vault, grabbed the important files, and managed her online accounts without stress.

Thanks to pre-planning her digital estate, Sarah made things much easier for her loved ones. This shows how a little preparation can save a lot of headaches and ensure your digital legacy is handled smoothly.

Conclusion

Thinking about your digital stuff might feel a bit overwhelming, but honestly, getting it in order gives you peace of mind. Your loved ones won’t have to scramble or guess what to do.

Just start small. Make a list of your accounts and important files. Then use InsureYouKnow.org to keep everything safe and organized. A little planning now can make a huge difference later, and it keeps your digital life easy for your family.

Understanding What Hospice Care Means

July 1, 2024

When treatment for serious illnesses is causing more side effects than benefits, or when health problems become compounded, then a patient and their family members may begin to wonder about hospice. “We recognized as people consider hospice, it’s highly emotional times,” says medical director for Austin Palliative Care Dr. Kate Tindall. “It might include worries and fears.” But one of the things she hears most often from patients and their families is that they wish they had started sooner. Understanding who qualifies for hospice and what it entails is the first part of deciding what might be best for those with terminal conditions.

What is Hospice Care?

Hospice is meant to care for people who have an anticipated life expectancy of 6 months or less, when there is no cure for their ailment, and the focus of their care shifts to the management of their symptoms and their quality of life. With hospice, the patient’s comfort and dignity become the priority, so treatment of the condition ends and treatment of the symptoms, such as pain management, begins. There are no age restrictions placed around hospice care, meaning any child, adolescent, or adult who has been diagnosed with a terminal illness qualifies for hospice care.

An individual does not need to be bedridden or already in their final days of life in order to receive hospice care. Other common misconceptions about hospice care are that it is designed to cure any illness or prolong life. It is also not meant to hasten death or replace any existing care, such as those already provided by a physician.

Determining When it’s Time for Hospice

Establishing care is most beneficial for the patient and their caregivers when it is taken advantage of earlier rather than later. Hospice can be used for months as long as eligibility has been met. Once there is a significant decline in physical or cognitive function, the goal for treatment should become to help that individual live comfortably and forgo anymore physically debilitating treatments that have been unsuccessful in curing or halting the illness.

Both individuals and their loved ones who would benefit from initiating hospice care are often unaware of the services or are uncomfortable asking about them. “It’s a hard conversation to have,” says professor of medicine and palliative care at the Duke University School of Medicine David Casarett. “Many people really want to continue aggressive treatment up until the very end.” While many wait for their providers to suggest it, it should be understood that if eligibility for hospice has been met, an individual and their caregivers can initiate hospice care on their own.

Establishing Hospice Care

In order to qualify for hospice care, a physician must certify that the patient is medically eligible, which means that the individual’s life expectancy is 6 months or less. Typically, the referral to hospice starts with the attending physician’s knowledge of that person’s medical history, while eligibility is then confirmed by the hospice physician. A hospice care team consists of professionals who are trained to treat physical, psychological, and the spiritual needs of the individual, while also providing support to family members and caregivers. Care is person-centered, with the importance being placed on the coordination of care, setting clear treatment goals, and communicating with all involved parties.

Receiving Care at Home

Hospice care is generally provided in the person’s home, whether it’s a personal residence or a care facility, such as a nursing home. “When people are close to the end of their lives, going to the hospital does not make them feel better anymore,” explains professor of medicine at the University of California Dr. Carly Zapata. “Because there’s not necessarily something that we can do to address their underlying illness.” Staying at home allows the individual to be around their personal things and close to their loved ones and pets, which can provide them with comfort during the end of their life.

What Does Hospice Care Include?

Hospice includes periodic visits to the patient and their family or caregivers but is available 24-7 if needed. Medication for symptom relief is administered, any medical equipment needed is provided, and toileting and other supplies such as diapers, wipes, wheelchairs, hospital beds are provided. What may surprise some people is that hospice patients may even receive physical and occupational therapy, speech-language pathology services, and dietary counseling.

If needed, short-term inpatient care may be established for those who cannot achieve adequate pain and symptom relief in their home setting. Short-term respite care may also become available to help family caregivers who are experiencing or are at risk for caregiver burnout. Bereavement care, or grief and loss counseling, is also offered to loved ones who may experience anticipatory grief. Grief counseling is available to family members for up to 13 months after the person’s death.

Paying for Hospice

The first step in finding a hospice agency is to search for ones that serve your county. If there are several options available, then it’s recommended to talk to more than one and see which agency will best fit the patient’s needs. Adequate research should be conducted since not all hospice agencies provide physical and occupational therapy.

Hospice is a medicare benefit that all Medicare enrollees qualify for, but it may also be covered through private insurance and by Medicaid in almost every state. Military families may receive hospice through Tricare, while veterans with the Veterans Health Administration Standard Medical Benefits Package are also eligible for hospice. Hospice agencies will also accept individual self-pay, while there are also non-profit organizations that provide hospice services free of charge.

Discontinuing Hospice Care

Though it is uncommon, if a patient does improve or their condition stabilizes, they may no longer meet medical eligibility for hospice. If this happens, the patient is discharged from the program. Another situation that sometimes arises is when a person elects to try a curative therapy, such as a clinical study for a new medication or procedure. In order to do that, the patient must withdraw from hospice through what is called revocation. Both children and veterans are exempt from being disqualified from hospice care if they choose to also pursue curative treatments. Any person may always re-enroll in hospice care at any time as long as they meet the medical eligibility.

Opting for Palliative Care

Individuals with chronic conditions or life-threatening illnesses may opt for palliative care, which doesn’t require people to stop their treatments. Palliative care is a combination of treatment and comfort care and can be an important bridge to hospice care if patients become eligible. Because transitioning to hospice care can be an emotional choice, palliative care providers often help patients prepare for that. Many people avoid palliative care because they think it is equal to giving up and that death is imminent, but studies show that for many, palliative care allows them to live longer, happier lives. This is due to the benefits of symptom management and spiritual support.

While hospice care can be difficult to accept, it can provide people with the best quality of life possible in their final days, as well as provide their loved ones with valued support. With Insureyouknow.org, you may keep track of all medical and financial records in one easy-to-review place so that you may focus on caring for your loved one, your family, and yourself during this period of their care.

Legal and Financial Planning for Those with Alzheimer’s and Their Caregivers

November 1, 2023

If you or a loved one is diagnosed with Alzheimer’s or dementia, then there are certain things that you will need to plan for legally and financially. An estimated 6 million Americans have Alzheimer’s, and it is currently the seventh leading cause of death in the United States. Alzheimer’s is a brain disorder that slowly decreases memory and thinking skills, while dementia involves a loss of cognitive functioning; both cause more and more difficulty for an individual to perform the most simple tasks. Though a diagnosis can be scary, the right planning can help individuals and their families feel more at ease.

Putting Legal Documentation in Place

Christopher Berry, Founder and Planner at The Elder Care Firm, recommends three main disability documents that should be in place.

First, there needs to be a financial power of attorney, a document that designates someone to make all financial decisions once an individual is unable to do so for themselves. If an individual lacks a trusted loved one to make financial decisions, then designating a financial attorney or bank is an option.

The next document that needs to be in place is the medical power of attorney that designates someone to make medical decisions for an individual. In many cases, it may be appropriate to appoint the same person to be the financial and medical power of attorney, as long as that person is well-trusted by the individual. In the event that something happens to the original power of attorney(s), successor (or back-up) agents for power of attorney(s) should also be designated.

The last document is the personal care plan, which instructs the financial and medical power of attorney(s) on how best to care for the individual in need. For instance, those entrusted to the care of an individual will need to make sure they sign medical records release forms at all doctor’s offices; copies of the power of attorney or living will should also be given to healthcare providers.

These three documents provide a foundation to make decisions for the individual diagnosed with Alzheimer’s or dementia when they no longer can themselves. It’s ideal to include the individual in these conversations in the early stages of their diagnosis, so that they may be a part of the decision-making process and appoint people that they will feel most comfortable with during their care.

How to Pay for Long-Term Care

Since Alzheimer’s is a progressive disease, the level of care an individual needs will increase over time. Care costs may include medical treatment, medical equipment, modifications to living areas, and full-time residential care services.

The first thing a family can do is to use their own personal funds for care expenses. It’s important for families to remember that they will also pay in their time, as many children of loved ones with Alzheimer’s or dementia will become the main caregivers. It may be wise to meet with a financial planner or sit down with other family members, such as your spouse and siblings, to determine how long some of you may be able to forgo work in order to provide full time care.

When personal funds get low or forgoing work for a period of time becomes difficult, long-term care insurance can be a lifesaver. The key to relying on long-term care insurance though is that it needs to be set up ahead of the Alzheimer’s or dementia diagnoses, so considering these plans as one ages may be smart.

Veterans can make use of the veterans benefit, or non-service-connected pension, which is sometimes called the aid and attendance benefit. This benefit can help pay for long-term care of both veterans and their spouses.

Finally, an individual aged 65 or older can receive Medicare, while those that qualify for Medicaid can receive assistance for the cost of a nursing home. If someone’s income is too high to receive Medicaid, then the spenddown is one strategy to know; under spenddown, an individual may subtract their non-covered medical expenses and cost sharing (including Medicare premiums and deductibles) from their available income. With the spenddown, a person’s income may be lowered enough for them to qualify for Medicaid.

Minimizing Risk Factors During Care

Research published recently in the journal Alzheimer’s & Dementia found that nearly half of patients with Alzheimer’s and dementia will experience a serious fall in their own home. Author Safiyyah Okoye, who was at John Hopkins University when the study was conducted, recommends minimizing risks such as these by safeguarding homes early on in diagnoses. “Examining the multiple factors, including environmental ones like a person’s home or neighborhood, is necessary to inform fall-risk screening, caregiver education and support, and prevention strategies for this high-risk population of older adults,” she states.

The good news is that since the progression of Alzheimer’s is often slow, families have plenty of time to modify the home for increased safety.

In addition to fall prevention modifications, other safety measures may include installing warning bells on doors to signal when they’re opened, putting down pressure-sensitive mats to alert when someone has moved, and using night lights throughout the home. Coats, wallets, and keys should also be kept out of sight, because at some point, leaving the home alone and driving will no longer be safe. Conversations about these safety measures, such as when an individual will have to stop driving, are ones that caregivers should have early on with their loved ones. Including individuals in their future planning while they are still cognitively sound will help both them and their caregivers feel more comfortable with the journey ahead.

It’s important to remember that even though receiving an Alzheimer’s or dementia diagnosis can be devastating, it is not the end. People with Alzheimer’s can thrive for many years before independent functioning becomes difficult. Both patients and caregivers will feel more calm through planning ahead. Insureyouknow.org can help caregivers stay organized by storing all of their important documents in one place, such as financial records, estate planning documentation, insurance policies, and detailed care plans. Above all, there is hope for those with Alzheimer’s; research is happening every day for potential therapies and future treatments.

The Pros and Cons of Living with Children in Retirement

August 1, 2023

Combining households can be a positive experience for everyone. In order to ensure that every member of the family is comfortable with living together, it will be important to talk it out. Communicating about any concerns before moving in together and then regularly thereafter will ensure that everyone remains happy with the decision to cohabitate. Amy Goyer, an AARP family expert, tells children of retirees to embrace the chance. “Look at this as an opportunity,” she adds. “You have a chance to enjoy your mom or dad in their later years. This is a way for children to know their grandparents in a way they wouldn’t otherwise.”

Before combining households, retirees and their children should consider all of the pros and cons of living together during retirement beforehand.

The Pros of Living With Children During Retirement:

- Retirees can be a big part of their grandkids’ lives. Many parents choose to live with their children during retirement so that they can be a major part of their grandkids’ lives. Some parents want to help their children raise their kids, such as picking them up from school, helping with meals, or taking their grandkids to their extracurriculars after school. Parents who were busy with work while their own children were growing up may feel that they can now make up for lost time.

- Your family will have a strong support system in place. While you may want to help your children with their needs, they may also need to help you. This can range from needing a ride to a doctor’s appointment to needing care after surgery or during an illness. Either way, living together will enable each of you to be more available to one another in times of need.

- Combined expenses may make living together more cost effective for both of you. Having a real financial talk with your children before you decide to combine households may prove that it could save each of you a lot of money. Coming up with a budget of shared expenses can actually help family members thrive both as a whole and individually. With the right budget, retirees shouldn’t have to dig into their retirement as much every month, while their children will be able to save up more of their monthly income.

In addition to communicating with one another about finances and caretaking roles, make sure everyone is allotted their own personal time. For instance, grandparents may opt to have their friends over while their grandkids are in school and their children are at work. Working together to ensure that every member of the family gets space from one another from time to time will help prevent anyone from feeling stifled. Retirement expert Nancy K. Schlossberg, author of Too Young to Be Old: Love, Learn, Work and Play as You Age, says, “If you do your emotional work upfront, you’re more likely to be satisfied with your final decision.”

The Pros of Living With Children During Retirement Could Also be the Cons:

- Retirees may not want to become full-time babysitters. If your children have children, and you’re disinterested in being a full-time babysitter to the grandkids, setting boundaries upfront about what you do and don’t want to do will be extremely important. Also, consider day-to-day life with young children and maybe pets. “If you have no tolerance for noise, do you want to move into a house with children or teenagers?” asks Jennifer Prell, president of Illinois elder-resource network Silver Connections.Be realistic about what you will and won’t be able to handle on a daily basis.

- Children of retirees may not want to become full-time caretakers either. Children of retirees may not be prepared for the burden of caring for their own parents.Again, establishing what everyone is comfortable with will be imperative. Contemplate the worst-case scenarios before moving in together. “Even if Mom moves in relatively healthy, that could change overnight,” elder-law attorney Kerry Peck points out. “Families generally underestimate the amount of care that Mom is going to require.”

- Retirees (or their children) may end up footing the bill for everyone. If retirees or their children become overly reliant on one another, then moving in together may become more expensive for one party than remaining apart. Having an honest talk about financial responsibilities and emergency savings before moving in together should help prevent unexpected expenses for either one of you down the road. “So many families run into trouble when something bad unexpectedly happens,” says Jill Schlesinger, author of The Dumb Things Smart People Do With Their Money. “That’s why it’s so important to talk to your kids about the What-Ifs,” said Schlesinger.

Consider Alternatives to Living Together

If you decide that joining households may not be the best option for your family, there are alternatives. Simply living closer to one another can reap the same benefits of living with children during retirement while removing the downsides.

While there’s an appeal to living ten minutes from one another, one of you may feel as if some of your independence has been lost. Talk to your children, and decide how close is too close. If in the end, you decide to live farther away from your children, planning reciprocal visits or spending part of the year with them may turn out to be the best of both worlds.

If you do decide to remain independent during retirement, make sure there’s plenty of room in your home for your children to visit or stay overnight. If you have more than one child, factor in enough space for all of them and their families, so that each of your children may visit you simultaneously.

In the end, living with your children during retirement should be beneficial for both of you. Insureyouknow.org can help your family keep the peace. When combining households, keeping the budget, financial information, healthcare records, and even family schedules in one easy-to-access place can help everyone work together to keep the household running smoothly. Since communication will be the key to living happily together, it will be important for everyone to be in the know.

Ask or Be Asked: Executor of an Estate

March 2, 2022

An executor of an estate is someone called upon to settle a deceased individual’s financial affairs. In your will, you may name a close relative, friend, accountant, attorney, or financial institution to act as executor of your estate. You also may designate co-executors—more than one person to handle your affairs. If you are asked to be an executor, consider it a great honor. But at the same time, keep in mind that it is also a great responsibility.

You should select an executor with integrity and good judgment. The law requires an executor to act in the estate’s best interest—known as “fiduciary duty”—even if they are also an heir, which is often the case. You’ll need to make sure they understand and are prepared for the job.

The Duties of an Executor of an Estate

An executor’s responsibilities can vary depending on the complexity of your estate, and the decisions you designate in your will. Following are some of the duties an executor of an estate performs.

- Locate the last will and file it in probate court

- Obtain certified copies of the death certificate

- Notify the state department of health of the death if a funeral home, crematorium, hospital, or nursing facility has not

- Distribute assets to beneficiaries

- Pay creditors

- Issue notices of death to banks, government agencies, and insurance companies

- File final tax returns

- Maintain property until the estate is settled

- Arrange care for any pets

- Make court appearances on behalf of the estate

- Notify current employer, if applicable

- Notify the deceased’s beneficiaries of the probate hearing

- Keep accurate records

- File the final accounting with the court and close the estate

As an executor, you may discover you need to hire a professional such as an accountant or attorney to help value and distribute certain assets, including:

- Assets with disputed ownership

- Business interests

- Royalties

- Out-of-state assets

- Complex investments

Ambiguities in a will and substantial bequests to a minor also may require a professional’s expertise, which your estate will pay customarily.

The Decision to Serve as an Executor

If you are asked to serve as an estate’s executor, realize that it is a great honor and a great responsibility. Consider your decision carefully before you agree. Think about the time commitment as well as the skillset and temperament required to perform the duties. Find out why the person asked you to serve as an executor and discuss his expectations for you to fill this role.

With this disclosure, you should be able to decide if you are qualified for the job and your fulfillment of an executor’s duties will be appreciated.

Compensation Considerations

Many executors perform their duties without compensation, especially if they are one of your estate’s beneficiaries. But executors can get paid for their work, and this arrangement is more common if the executor is a person outside your family or if settling your estate requires significant expenses such as travel, filing court documents, or overseeing the sale of your real estate.

Another option for you is to limit in your will the fees to a specific dollar amount. Or you may specify the payment of reasonable fees based upon state law.

Typically, executors can expect to get paid once the estate is settled. If they incur out-of-pocket expenses, such as utilities, property taxes, insurance, and storage fees before the estate is settled, they can usually reimburse themselves during their estate administration. But again, compensation is a subject that should be spelled out before you accept an executorship. Spending down any estate monies can be an area of great sensitivity, especially if heirs believe their inheritance was reduced because of your executorship.

InsureYouKnow.org

When you select an executor of your estate who accepts the responsibility to carry out your wishes regarding your estate upon your death, ask yourself the following five essential questions. Let the executor know if the answers can be found on your InsureYouKnow.org portal.

- Where is your original will? If you keep your will in your house, be specific about where to find it. If you filed it with your attorney, provide contact information. Don’t store it in a safe deposit box, where it may be difficult to access after your death. You should share your InsureYouKnow.org access credentials with the executor of your estate to be able to find a copy of your will online.

- Who should be notified? Compose a list of people and organizations with contact information for your executor to contact. If you keep this list at InsureYouKnow.org, you can update it regularly.

- What are your passwords and access codes? Let your executor know how to retrieve your passwords and access codes for email, social media, other media accounts, cellphones, and computers. Store and keep this data current at InsureYouKnow.org.

- Who will receive your possessions? If you have nonfinancial items such as family recipes, photos, heirlooms, and memorabilia, keep details with designated recipients at InsureYouKnow.org.

- Do you have any secret items? Let the executor or another person you trust know if you possess personal items that need to be dealt with on a confidential basis. Such items may include correspondence, photos, or documents personal in nature. You can keep a secure list of these items at InsureYouKnow.org.

Selecting a trusted executor to carry out your will is an important part of estate planning. Experts recommend updating your will every few years to make sure it still reflects your chosen executor and decisions to be carried out after your death. If you need to create or update your will, you can file copies at InsureYouKnow.org.

Whether you are the person asking or are the person being asked to be an executor of an estate, carefully consider and execute the responsibilities and duties required.