Tag: vital records

Top 3 Vital Documents Every Senior Needs to Organize Today

April 1, 2026

Every single year, thousands of older homeowners throw away hundreds, even thousands, of dollars. Why? They simply didn’t file the right piece of paper. Meanwhile, families are out there making agonizing medical choices in crowded hospital hallways because nobody knows where mom or dad put their living will. And don’t even get started on Medicare benefits lost to the void of a messy filing cabinet.

These aren’t freak accidents. This stuff happens constantly to otherwise prepared families who just didn’t get their paperwork sorted in time.

If you’re a senior, or helping one manage their affairs, three specific types of documents need your attention right now: property tax exemptions, Medicare files, and advance directives. Getting a handle on these and actually keeping them where people can find them protects your money, honors your medical choices, and cuts out the panic when things go sideways.

Why Property Tax Exemption Documents Are More Important Than Ever

Sure, most older homeowners know property tax breaks exist. But hardly anyone realizes exactly how much cash they’re leaving on the table by not claiming them or by forgetting to renew them.

Fast forward to 2026, and a bunch of states have seriously beefed up their senior tax relief. Take New York: qualifying homeowners 65 and up can now shield up to 65% of their home’s assessed value from taxes (up from the old 50% cap). In New Jersey, the Stay NJ program is knocking up to $6,500 a year off tax bills for households making under $500,000. Over in Texas, they’ve expanded the over-65 school district exemption so much that plenty of folks aren’t paying school taxes at all anymore.

Here’s the catch, though. They don’t just hand this money to you automatically. In Texas alone, roughly 15% of eligible folks never file for their homestead exemption. That’s about $1,500 a year just evaporating. You see the same thing happening nationwide.

And then there’s the renewal trap. A lot of these tax breaks force you to refile every single year. Miss a random deadline in March or April? You lose the discount for the whole year. If your proof of age, income, and residency isn’t sitting somewhere obvious, blowing past that deadline is incredibly easy.

Here is what you actually need to keep handy:

- Proof of age (like a birth certificate or government ID)

- Proof you actually live there (mortgage statements, recent utility bills)

- Your latest income info (Social Security award letters, tax returns)

- The actual exemption application and those annoying annual renewal notices

- Any random letters the county assessor mails you

When you finally get this stuff organized ideally in a secure digital spot that your kids or trusted contacts can reach claiming your tax break turns into a quick annual chore instead of a frantic scavenger hunt.

The Medicare Documents That Too Many Families Cannot Find

Medicare is arguably the most crucial benefit you’ll ever get. Yet, the paperwork usually ends up shoved in a jammed desk drawer nobody else can open. Or worse, sitting in a messy pile on the kitchen counter.

For seniors and the people taking care of them, there’s a core stack of Medicare records you absolutely must keep safe and share with at least one person you trust.

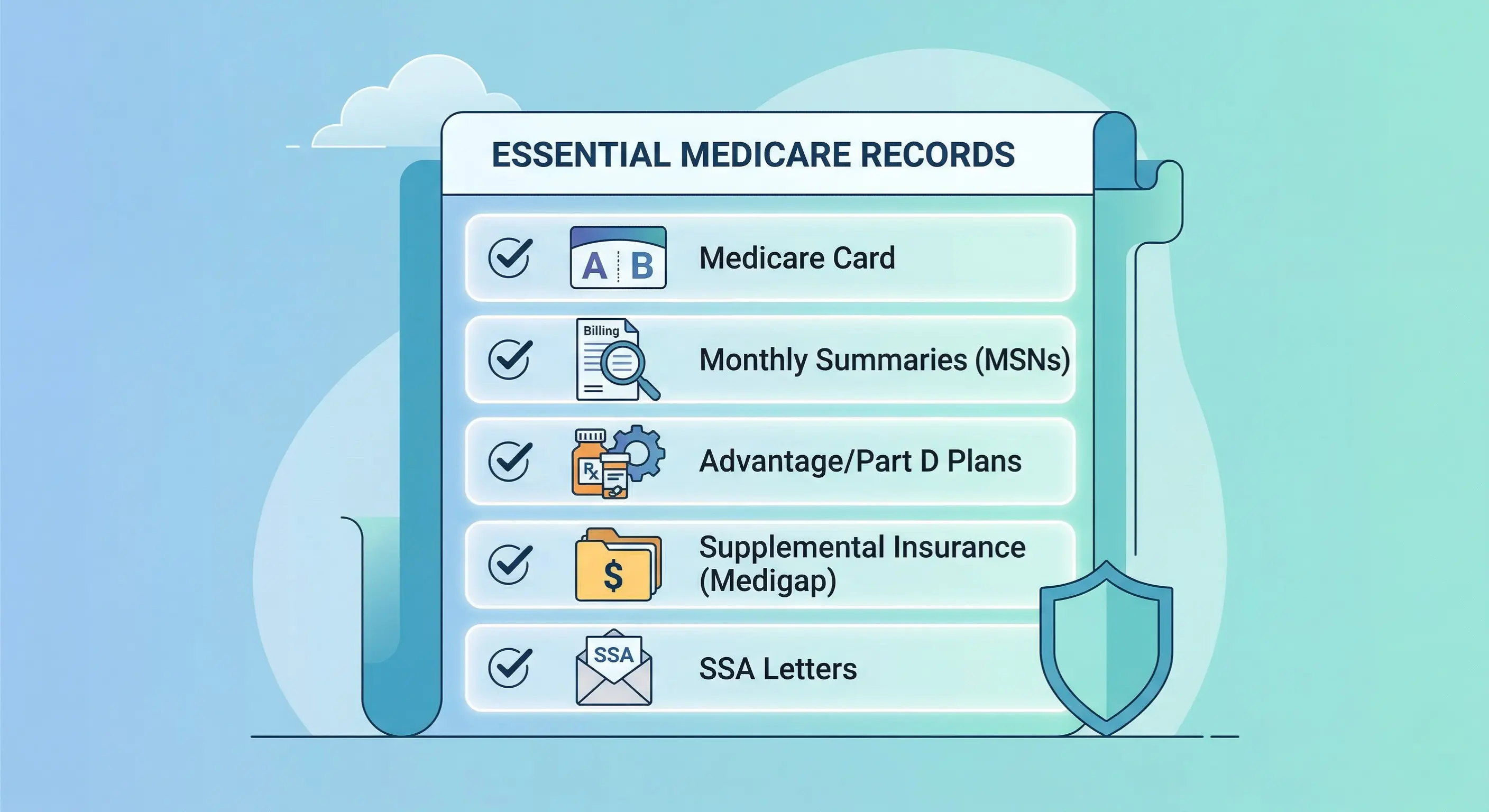

Keep these essential Medicare records organized:

- Your actual Medicare card (Part A and Part B)

- Medicare Summary Notices (MSNs) these are the monthly statements showing what they billed and what Medicare actually covered

- Enrollment docs for your Medicare Advantage or Part D plan

- Explanation of Benefits (EOB) from any Medigap or supplemental policies

- Letters from Social Security about your eligibility or premiums

- Paperwork for the Medicare Savings Program, if you use it

- Any records of fights or appeals with Medicare

Look, this isn’t just busywork. These papers prove you have coverage during an emergency. They help you spot billing fraud. They are totally necessary when you’re trying to coordinate care between three different doctors. If you end up in the hospital and your daughter needs to argue with the billing department, handing her these records will save her hours on hold and prevent massive bills.

Also, remember that Medicare Part B pays for a voluntary chat with your doctor about advance care planning. If you do this during your annual wellness visit, it shouldn’t cost you a dime out of pocket. Keep the notes from that conversation on file, too.

Living Wills and Advance Directives: The Documents That Speak When a Senior Cannot

Out of everything you could possibly organize, the living will is probably the most personal. It’s also the one document guaranteed to go missing right when everyone desperately needs it.

The University of Michigan’s National Poll on Healthy Aging found something pretty alarming: 54% of adults between 50 and 80 haven’t bothered with an advance directive or living will. So what happens? A medical crisis hits, and total strangers (doctors who just met the patient) or terrified family members have to make gut-wrenching decisions under crazy pressure.

A living will is just a legal paper that outlines what medical treatments you want if you can’t speak for yourself. A healthcare proxy (sometimes called a durable power of attorney for healthcare) officially names the person you trust to make those choices for you. The living will itself gets into the weeds about things like dialysis, ventilators, resuscitation, and feeding tubes.

And please don’t think this is only for the very old or the terminally ill. Car accidents and strokes don’t check your calendar. It is so much better to write a living will at 65 while you’re healthy than to try scraping one together at 85 in the ICU.

Make sure you store and share these key advance directive documents:

- The living will itself

- Durable power of attorney for healthcare

- Your POLST or MOLST form (Physician Orders for Life-Sustaining Treatment), if you have one

- The actual healthcare proxy paperwork

- Your written wishes regarding organ donation

- Copies of all this given to your primary doctor and any major specialists

Quick tip: if you’re a snowbird splitting time between two states, do yourself a favor and create an advance directive for both. Keep copies of both documents together in both houses.

The Common Thread: These Documents Are Useless If No One Can Find Them

A tax exemption that lapsed. A Medicare card buried in a shoebox under the bed. A living will locked tight in a safe that only grandpa knew the combination to. This exact nightmare plays out in living rooms across the country every single day.

The real goal here isn’t just printing out forms. It’s about locking them down somewhere secure, actually keeping them up to date, and making sure your trusted point person knows exactly where to look when the time comes.

That is exactly why platforms like InsureYouKnow.org exist. It’s a secure, encrypted digital safe deposit box. You can stash your vital records there, give access to the people you trust, and even set up nudges to review everything once in a while. Nobody wants to do paperwork just for fun. You do it for the peace of mind.

You do it so that when life throws a curveball, the right papers are in the right hands immediately.

Seniors and their families already have enough stress to deal with. Getting your records straight today basically guarantees you one less crisis tomorrow.

InsureYouKnow.org is a secure electronic safe deposit box for life’s most important information. The platform does not provide legal, financial, or insurance advice it helps ensure that the right people have access to the right documents when they need them most.

How to Tell Your Beneficiaries About Life Insurance Without Stress

March 19, 2026

Billions of dollars in life insurance death benefits sit unclaimed across the United States annually. Families often desperately need these funds, and the policies themselves remain completely valid. The problem usually stems from a simple communication gap where the named individuals had no idea the coverage even existed.

Industry investigations revealed major insurers releasing over $7 billion in previously forgotten benefits between 2006 and 2016, but only after regulators forced them to cross-reference death records. Experts strongly believe the actual amount of missing money is substantially higher. Current data points to roughly $6 billion in unpaid benefits sitting in limbo, largely caused by outdated contact details and uninformed relatives.

This situation is entirely preventable. Fixing the issue does not demand expensive attorneys, formal family meetings, or highly uncomfortable discussions. Policyholders just need to share the right details clearly and proactively so the information actually sticks.

Why Beneficiaries Remain in the Dark

Policyholders avoid talking about their coverage for several reasons. Some individuals harbor superstitions regarding death. Others fear the topic might sound morbid or cause unnecessary distress among relatives. A large portion of people simply assume loved ones will figure everything out when the moment arrives.

Insurance providers lack automatic alert systems to notify anyone when a policyholder passes away. No alarm sounds and no automatic check gets mailed. Companies usually only discover a death has occurred when a relative reaches out directly. That requires the family to actually know about the coverage beforehand.

The most frequently forgotten accounts include decades-old plans, employer-sponsored group coverage from previous jobs, and small whole-life policies intended for final expenses. Important paperwork easily gets lost during house moves. Premium drafts might quietly exit a bank account for years without a surviving spouse noticing. Lacking a clear handover of documents leaves surviving relatives guessing and frequently finding nothing.

Starting the Conversation Without Uncomfortable Feelings

Discussing these financial safeguards never has to sound like a grim announcement. Financial planners frequently suggest centering the talk on care and future preparation instead of loss. A simple mindset shift changes everything. The focus moves away from passing away and toward actively protecting important family members.

Several approaches help these talks feel completely natural:

- Tie it to a life event: Welcoming a new grandchild, navigating a health scare, or updating a will provides an easy opening. Someone might say, “While getting these organizational tasks done, it is important to share the details of this life insurance coverage.”

- Frame it as a gift: Informing dependents about their financial protection acts as a generous gesture. Policyholders can position the talk as offering clarity. A good phrase to use is, “To prevent any future scrambling, here are the essential details needed for the records.”

- Use a document review as the opener: Checking financial records every year builds excellent habits. Inviting an adult child or spouse to observe the review creates a low-pressure environment to share policy specifics naturally.

Essential Information for Beneficiaries to Know

Mentioning the mere existence of a policy falls short of being helpful. Grieving relatives require highly specific data to process claims quickly. Handing over this data early minimizes delays, lowers stress levels, and guarantees the funds reach the intended destinations promptly.

The National Association of Insurance Commissioners recommends granting access to the following specific details:

- The exact name of the provider and the full name of the insured person as listed on the contract

- The specific policy number and the exact type of coverage selected

- The total death benefit value alongside any attached riders

- Direct contact details for the provider or the managing agent

- The exact physical or digital location of the official documents

- Clear distinctions between primary and contingent individuals along with the designated percentage splits

Any individual holding multiple plans through an employer, private company, or professional group must document and share every single one. Relatives frequently uncover hidden coverage months or years after a funeral, making thorough documentation crucial.

Explaining Primary and Contingent Beneficiaries Clearly

The difference between primary and contingent designations frequently causes confusion. A primary designation puts a person or entity first in line for the funds. A contingent designation acts as a backup, stepping up only if the primary individual cannot collect the funds due to passing away themselves.

Everyone named on the contract must understand their exact role. Splitting funds requires each party to know their specific percentage share. Transparent communication stops arguments and blocks potential legal headaches later on. It helps to remind everyone that designated beneficiaries on a contract will overrule any instructions written into a standard estate plan.

Keeping Documents Accessible During Critical Moments

Spoken words offer a solid starting point but fall short long-term. People forget things quickly while grieving. Physical papers easily succumb to fires, floods, or misplacement during a move. The safest strategy pairs direct communication with a highly secure, centralized storage spot for all vital records.

Tucking the contract next to estate papers represents the traditional route, yet it carries flaws. Locking physical copies inside a bank safe deposit box often requires the policyholder to be present for access. This creates massive roadblocks for relatives at the worst possible time.

Digital platforms solve this accessibility problem beautifully. Encrypted online vaults allow users to stash life insurance details, medical coverage, banking numbers, and legal files in a single hub. Trusted contacts receive access to designated files, guaranteeing the correct people find the right information instantly from any location.

Updating Beneficiary Designations and Communicating Changes

Designations must evolve alongside major life shifts. Marriages, divorces, new babies, or the loss of a designated relative demand an immediate contract review. Neglected updates stand out as a top reason for delayed payouts and legal disputes. Industry research shows roughly 8% of claims hit roadblocks specifically due to obsolete contact data.

Updating a file means everyone involved needs a notification. Swapping out a former spouse for a new partner means both sides require an update, when appropriate. These chats might feel slightly awkward, but leaving a grieving family to fight over uncertain terms causes much deeper pain.

Creating an annual calendar alert to verify these designations builds a highly effective habit. Digital platforms often send automated monthly nudges to check for necessary updates. This turns file maintenance into a seamless part of standard financial upkeep.

Early Conversations Protect Loved Ones Tomorrow

Sharing policy details ranks among the most impactful financial steps a person can take. The process requires zero legal background and avoids feeling overly morbid. It just takes a willingness to speak directly and the discipline to organize the supporting paperwork.

Relatives who understand the coverage, know the storage location, and possess the correct contact numbers can actually focus on healing instead of hunting down forms. Providing that exact peace of mind remains the core purpose of buying coverage. The product only works if the protected individuals know it exists.

Utilizing an encrypted digital vault to hold these financial and legal records proves incredibly practical. This ensures the preparation goes far beyond spoken words. It builds an adaptable record that follows a family through every life stage, waiting quietly until the exact moment it becomes necessary.