Tag: secure document storage

2026 OBBBA Estate Tax Changes: What Families Must Update

March 11, 2026

The wealth transfer landscape just experienced a massive earthquake. When the One Big Beautiful Bill Act (OBBBA) took full effect on January 1, 2026, it completely tossed out the old estate planning rulebook. For years, financial planners, wealth managers, and tax attorneys had been bracing for the Tax Cuts and Jobs Act (TCJA) to expire. Everyone fully expected federal estate tax exemptions to get sliced in half overnight. Instead, lawmakers pivoted. The OBBBA rolled out permanent, historically high exemption thresholds that caught many off guard.

But breathing a sigh of relief and doing nothing is a very dangerous game. The new rules demand a fresh, immediate look at existing wills, family trusts, and generational wealth strategies. Navigating state-level tax cliffs, optimizing new child savings accounts, and securing vital legal documents in an encrypted digital vault are no longer optional steps. Taxpayers have to adapt to this new 2026 reality right now. Otherwise, they risk leaving their family’s financial future completely exposed to unnecessary taxation and legal chaos.

The New $15 Million Federal Exemption

Let us look closely at the numbers. The absolute heart of the OBBBA’s estate planning shift is a massive, permanent bump in federal estate, gift, and generation-skipping transfer (GST) tax exemptions. As of the start of 2026, the baseline sits at a staggering $15 million per person. For a married couple, that builds a $30 million fortress against federal wealth transfer taxes. And yes, those figures are indexed for inflation. They will keep inching up year after year to match economic changes.

Before this legislation passed, a low-level panic had set in among high-net-worth households. Families rushed to execute lifetime gifts, terrified the exemption would drop back down to roughly $7 million. Today, that ticking clock is gone. The absolute permanence of the $15 million threshold lets people slow down. Families can now make smarter, highly calculated, long-term choices about distributing their wealth without an artificial deadline hanging over their heads.

Realistically, only a tiny sliver of the absolute wealthiest estates will ever see that punishing 40% federal estate tax hit. Removing that massive federal tax burden for the vast majority of households changes the entire financial game. The planning focus now shifts sharply toward income tax efficiency and carefully managing assets that grow in value over time.

The Strategic Pivot to Capital Gains and Step-Up in Basis

With federal estate taxes officially off the table for most, a new financial villain emerges: the capital gains tax. This shift makes the “step-up in basis” strategy incredibly valuable. Under the current tax code, when someone inherits an asset think real estate, art collections, stock portfolios, or a family business the tax basis of that asset gets “stepped up.” It adjusts legally to the fair market value on the exact day the original owner passes away.

Consider an individual who bought a commercial property decades ago for $200,000. Today, the market values that property at a cool $2 million. If the owner hands that property to their children right now as a living gift, the kids take on that original $200,000 cost basis. If those heirs turn around and sell the building, they will get slapped with brutal capital gains taxes on $1.8 million of profit.

But what if that same property transfers at death? The heirs receive it with a stepped-up basis of $2 million. They could sell the building the very next day and owe absolutely zero capital gains tax. Because the OBBBA erased the fear of a 40% estate tax for most, holding onto highly appreciated assets until death is now the smartest play. It shields heirs from massive, wealth-destroying income tax bills.

Why Lifetime Gifting Remains Vital for High-Net-Worth Estates

Still, families hovering near or above that $15 million (or $30 million joint) mark cannot just sit back and relax. Lifetime gifting remains a cornerstone strategy for the ultra-wealthy. The basic math of estate planning has not changed one bit. Assets left inside a taxable estate will keep growing. Eventually, that future growth will face the 40% federal estate tax axe.

Moving assets today locks in the current $15 million exemption. It guarantees that any future market growth happens completely outside the taxable estate. Take a $10 million business interest as an example. Placing it into an irrevocable trust today is a smart move. If that business grows to $25 million over the next ten years, that entire $15 million of growth is totally safe from federal transfer taxes.

High-level tools like Spousal Lifetime Access Trusts (SLATs) and Generation-Skipping Dynasty Trusts are working harder than ever under the OBBBA. They let families use the big exemptions while keeping assets safe across multiple generations. However, pulling this off requires a mountain of complex legal paperwork. Keeping those irrevocable trust agreements highly secure and instantly accessible is the only way to ensure these sophisticated strategies actually work when the time comes.

The Hidden Trap of State-Level Estate Taxes

Here is a massive trap waiting to spring on unsuspecting families. The federal government eased up, but state governments definitely did not. Assuming the $15 million federal shield protects against all estate taxes is a very expensive mistake. Over a dozen states still enforce their own estate or inheritance taxes. Their exemption limits are usually far, far lower than the federal line.

Take New York’s infamous “tax cliff,” for example. In 2026, if a resident’s estate goes over the state exemption limit by even a fraction, the state taxes the entire estate. The law does not just tax the overflow; it taxes the whole thing. That triggers millions in surprise tax bills. Massachusetts and Oregon also enforce notoriously strict state-level limits.

Families living in or holding real estate in these specific states have to plan locally. Often, this means utilizing aggressive lifetime gifting. Many states with estate taxes completely lack a matching gift tax. Shrinking the taxable estate before death through planned giving can bypass the state tax cliff entirely.

New Provisions: Trump Accounts, 529s, and Charitable Giving

The OBBBA did not just tweak old rules; it brought brand-new tools to the table. Families need to weave these modern provisions into their legacy plans right away to maximize tax efficiency.

- Trump Accounts: A brand-new tax-advantaged setup designed specifically for children. For U.S. citizens born between 2025 and 2028, the federal government drops in a one-time $1,000 seed contribution. From there, families and employers can add up to $5,000 a year until the child turns 18. The wealth grows completely tax-deferred, offering a massive head start on generational wealth building.

- Expanded 529 Plans: Education savings just got a lot more flexible. Families can now pull out up to $20,000 a year for K-12 private school expenses, effectively doubling the old limit. Furthermore, the legal definition of qualified expenses expanded in 2026. Things like private tutoring and specialized textbooks now count, making these accounts far more versatile.

- Charitable Deduction Floors: Starting in 2026, taxpayers who itemize are looking at a new hurdle. Only charitable giving that passes 0.5% of their adjusted gross income actually counts for a tax deduction. This rule forces families to get highly strategic. “Bunching” donations into a single year using Donor-Advised Funds (DAFs) or private foundations is now the undisputed best way to squeeze out maximum tax benefits while supporting chosen causes.

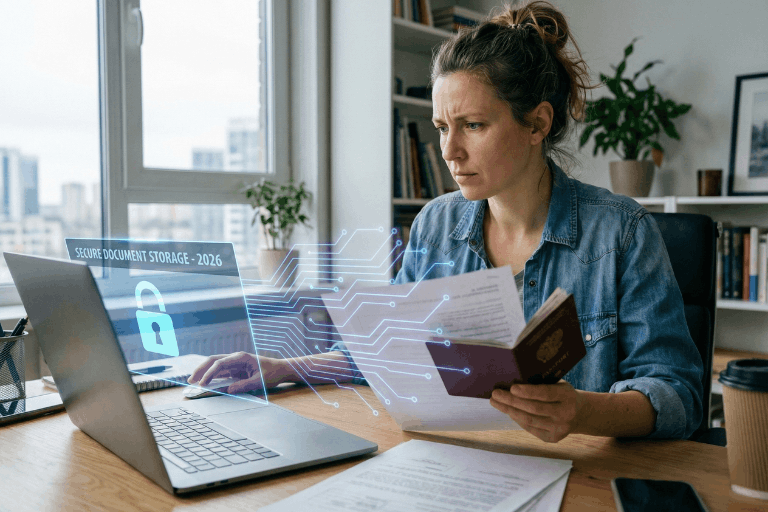

The Critical Need for Digital Organization and Secure Storage

Every time tax laws undergo a massive rewrite, financial advisors sound the alarm. Update the wills. Change the trust terms. Fix the outdated beneficiary designations. But spending thousands of dollars and dozens of hours updating an estate plan is completely useless if no one can actually find the paperwork when tragedy strikes.

The modern estate is no longer just a stack of paper. It consists of digital assets, cryptocurrency private keys, online bank logins, and electronically signed medical directives. Trusting a rusty filing cabinet in a home office or a dusty safe deposit box at a local bank is a disaster waiting to happen. Fires, floods, or simple human error can wipe out years of meticulous legal planning in an instant. When a sudden emergency hits, a chosen digital executor needs fast, zero-friction access to the full financial picture. Hunting down scattered passwords while dealing with grief is a nightmare no family should face.

To make sure a newly updated 2026 estate plan actually works in the real world, families are rapidly migrating to encrypted, independent electronic safe deposit boxes. A centralized digital vault puts life insurance policies, updated trusts, and crucial medical records in one secure spot. Platforms utilizing military-grade cloud encryption and zero-knowledge architecture are the modern gold standard. Why? Because even the host website cannot see the user’s passwords. It guarantees sensitive financial blueprints stay permanently locked away from hackers, yet remain instantly available to trusted, designated contacts during life’s hardest moments.

Conclusion

The 2026 One Big Beautiful Bill Act handed families incredible tools to protect generational wealth. At the same time, it threw complex curveballs regarding capital gains, state taxes, and charity rules. The massive $15 million federal exemption is not an excuse to get lazy. It is a rare opportunity to build smarter, highly tax-efficient strategies. Taxpayers need to sit down with their legal and financial teams to completely overhaul their legacy plans today. And once those plans are updated? They must be locked inside a bulletproof, password-protected digital repository. That is the only way to ensure a carefully built financial legacy survives, stays protected, and activates exactly when the family needs it most.

2026 Student Loan Defaults: Secure Your Financial Records

March 6, 2026

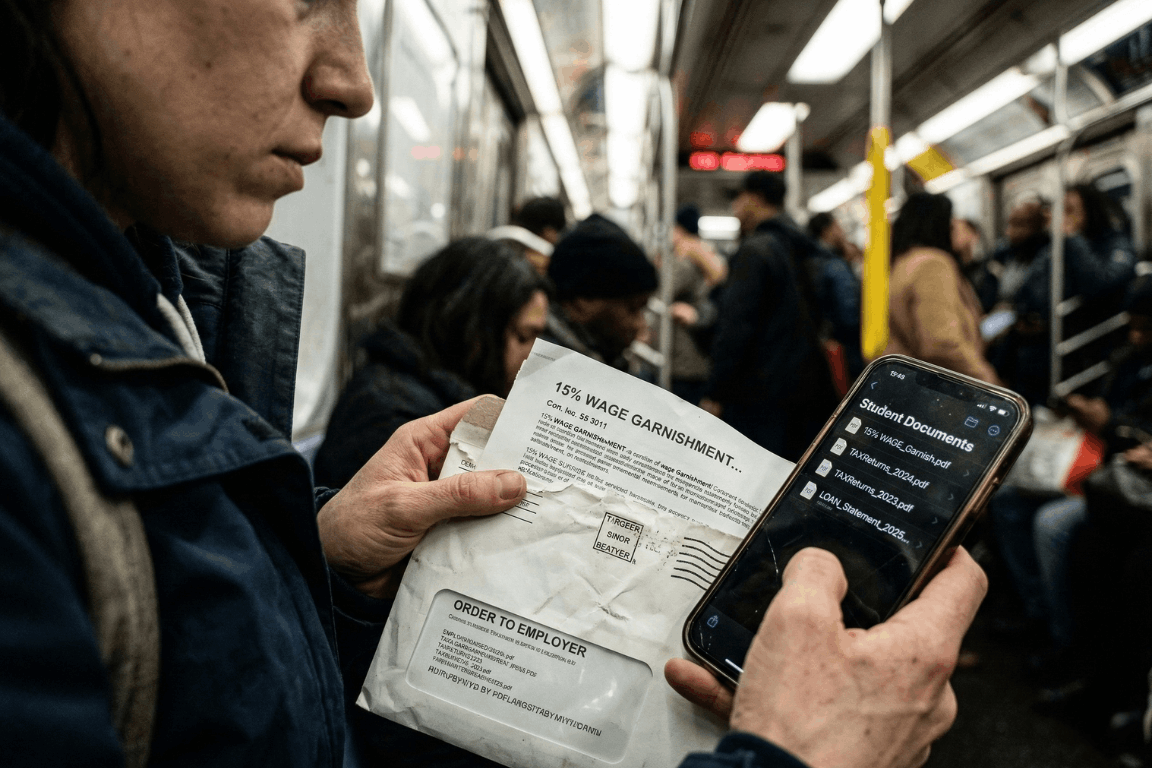

A massive financial wall hit millions of Americans earlier this year. Pandemic payment pauses are officially ancient history. The temporary relief programs dried up entirely. After months of messy court battles regarding income-driven repayment plans, the federal government decided to bring back its heaviest collection tools. Starting in early 2026, the U.S. Department of Education began sending administrative wage garnishment letters to defaulted borrowers. The numbers from major credit bureaus, like Experian, look pretty grim. The entire country is watching a massive wave of loan delinquencies happen in real time. People are suddenly staring down severe financial penalties. Getting through this economic squeeze requires a lot more than just reading news updates. It demands immediate, highly organized access to specific financial paperwork.

The 2026 Student Loan Landscape: A Shocking New Data Trend

So, who is actually defaulting right now? Historically, student loan defaults mostly hammered sub-prime borrowers. That whole narrative flipped completely upside down in 2026. Recent reports from credit bureaus reveal something entirely unexpected. Nearly a quarter of newly defaulted borrowers belong in the “prime” credit tier or even higher. These are the exact demographics the financial industry usually views as incredibly stable.

With over 5 million borrowers currently sitting in default status, and millions more falling behind every month, the economic pain is obvious. Borrowers are stuck navigating a bizarre maze of constantly changing payment plans. Making things worse, millions of accounts got bounced around between different private servicing companies over the last two years. Monthly payments got lost in the mail. Crucial paperwork simply vanished. Hold times to speak with basic customer service stretched into hours. Once a federal student loan reaches 270 days past due, it hits official default status. At that specific moment, the government gets to use an administrative superpower that regular credit card companies cannot even touch. They can literally take wages without ever stepping foot inside a courtroom.

Understanding Administrative Wage Garnishment: The 15% Reality

The fallout from a federal default happens fast. Through a process called Administrative Wage Garnishment (AWG), the Department of Education can legally force an employer to pull up to 15% of a borrower’s disposable pay. Disposable pay simply means the cash remaining after legally required deductions, like federal and state taxes, come out of the check.

Federal law does leave a very small safety net in place. Borrowers get to keep a weekly take-home amount equal to at least 30 times the federal minimum wage. But for anyone living from one paycheck to the next, suddenly losing 15% of their income is pure disaster. It usually means missing the rent, skipping the grocery store, or defaulting on other credit cards. Before the garnishment actually kicks in, the government must send a 30-day advance written warning. That specific 30-day window is basically everything. It acts as the only real timeframe a borrower gets to object or set up a different payment plan before their paycheck actually shrinks.

How to Stop Garnishment: The Heavy Burden of Proof

Borrowers holding a garnishment notice still carry some legal rights. During those 30 days, individuals can officially demand a hearing to stop the withholding order. They might attempt to prove extreme financial hardship. Or, they could try applying for federal loan rehabilitation. Rehabilitation usually involves agreeing to make nine on-time payments over a 10-month window to get the loan back on track.

Another route involves submitting a formal financial hardship appeal. Winning this appeal means legally proving that a 15% pay cut makes buying basic survival items impossible. The government looks at documented living expenses and compares them against very strict IRS Allowable Living Expense guidelines. If a family spends more on food or housing than the IRS thinks is necessary for that specific family size, the extra amount gets totally ignored. Proving hardship is notoriously difficult. Using these rights is never a walk in the park. It requires gathering highly specific legal and financial records immediately. In these types of administrative hearings, the burden of proof lands squarely on the borrower.

The Critical Role of Organized Financial Documents

Sloppy paperwork turns a bad money situation into an absolute nightmare. When the garnishment letter shows up, the clock ticks fast. Spending hours digging through cluttered email inboxes for old messages from loan servicers wastes valuable time. Tearing up the living room looking for utility bills to prove basic living expenses just fuels the anxiety. If a borrower fails to hand over the correct evidence within 30 days, their employer receives the order. The garnishment starts.

This explains exactly why relying on a secure, independent electronic safe deposit box changes the playing field. Keeping a dedicated digital vault for vital life information ensures nobody gets blindsided by aggressive debt collectors. Storing all important financial, legal, and contractual documents in one simple location gives borrowers a huge advantage. They can instantly grab the exact proof they need to protect their paychecks and negotiate with default resolution teams.

Essential Documents to Secure in a Digital Vault

To build a strong defense against a default warning, individuals should make sure the following documents are digitized, safely uploaded, and ready for action:

- Original Loan Agreements and Master Promissory Notes: Finding original contracts immediately helps verify the true debt amount. It also spots accounting errors and confirms which company actually owns the loan today.

- Complete Tax Returns: Proving financial hardship or enrolling in an income-driven repayment plan means submitting paperwork. The Department of Education demands recent federal and state tax returns before they even start talking.

- Official Pay Stubs: Current pay stubs are absolutely required to figure out actual disposable income. They also help verify that any proposed wage garnishment does not illegally drop below the minimum wage protection limit.

- Household Expense Records: Tracking basic living costs is a strict requirement for hardship appeals. Think about rent agreements, mortgage papers, utility bills, health insurance premiums, and pharmacy receipts. These papers help prove that living expenses are reasonable and fit within tight IRS standards.

- Correspondence with Loan Servicers: A strong paper trail of older payments, approved forbearances, and emails with the loan servicers can literally save the day. This proof is extremely important if someone needs to show a loan was wrongfully thrown into default in the first place.

The Absolute Security of Zero-Knowledge Storage

Privacy is absolutely non-negotiable when dealing with highly sensitive financial details. Relying on physical metal filing cabinets leaves people wide open to lost papers, house fires, or basic theft. Depending on regular, unencrypted email folders or a messy computer desktop basically hands sensitive financial data directly to hackers. Cybercriminals routinely target email servers specifically to find W-2 forms and tax returns. Once they grab those files, identity theft is pretty much guaranteed.

Using a specialized platform built with heavy-duty cloud encryption makes sure financial data stays completely private. The absolute best platforms run on Amazon cloud encryption mixed with a “zero-knowledge” setup. In a zero-knowledge system, only the actual account owner knows the password. The site administrators never get to see it. That means absolutely nobody else can ever gain access, view the files, or mine the stored documents to sell the data.

Strategic Document Sharing with Trusted Partners

Fixing a defaulted student loan is almost never a solo job. Borrowers usually need to bring in certified financial planners, tax accountants, or specialized student loan lawyers to help decode the messy federal rules.

Advanced secure portals allow individuals to selectively share specific document folders with these exact trusted partners. Sending unencrypted PDFs of tax returns and pay stubs back and forth through regular email is a massive cybersecurity hazard. Instead, account holders can simply give a legal advisor temporary, secure access to the required files right inside the encrypted vault. This targeted sharing feature speeds up the whole default resolution process, keeps communication secure, and leaves the rest of the vault totally locked down. Setting up automatic monthly reminders inside the portal also helps users routinely update their financial snapshots, keeping their defense strategy completely fresh.

Facing economic uncertainty requires a solid game plan. The return of federal student loan wage garnishments in 2026 creates a massive hurdle. Credit bureau data clearly shows that financial distress is hitting borrowers across every single demographic right now. Surviving this wave of defaults demands aggressive, proactive money management and flawless record-keeping. Centralizing vital financial documents into a secure, encrypted digital safe deposit box lets individuals tackle economic chaos with total confidence. Being prepared is simply the ultimate defense. It ensures that when critical financial information is needed the most, it stays protected, perfectly private, and instantly ready to use.

AI and Data Privacy in 2026: Securing Vital Information

February 19, 2026

Forget the old sci-fi movies. Today, artificial intelligence practically runs the show. It handles everything from spotting diseases to balancing checkbooks. Every major industry uses these tools to save time and cut corners. But there is a massive catch. This entire system runs on one specific fuel. That fuel is personal information.

Understanding how these powerful computer networks handle private details matters more today than ever before. The tech moves incredibly fast. The ways companies grab and store digital footprints change right along with it.

The AI Data Appetite: How Information is Used

Machine learning models are hungry. These systems require an unbelievable amount of raw material to actually function. Sometimes, a program chews through billions of data points just to learn a single, simple pattern. A fast screen swipe, a late-night online purchase, or a routine doctor’s chart update, they all leave a permanent mark.

Code then sifts through this massive pile of details to customize what people see online. Sure, that makes picking a streaming movie or getting a quick cash loan way easier. But it comes at a cost. Big corporations constantly harvest and tag private details. These software tools connect the dots between things that seem totally unrelated. Next thing you know, a retailer is predicting what a customer will buy next Tuesday, or even guessing their secret health conditions.

Emerging Privacy Risks in the AI Era

This massive leap in technology brings a totally new set of privacy headaches. People have to deal with these threats every single day.

- Sophisticated Cyber Threats: Hackers rarely waste time guessing passwords anymore. Why bother? They use generative code to craft perfect phishing emails and hyper-realistic deepfakes instead. These modern scams blow right past old-school security filters. Because of this, bank records and identities sit directly in the firing line.

- The Rise of “Agentic” AI and Shadow Apps: Smart software agents operate on their own now. They move files and make choices at crazy speeds. When employees or everyday folks rely on unregulated “shadow” tech tools, highly sensitive documents often bleed right into public training models. The worst part? Nobody usually notices until the damage is fully done.

- Algorithmic Bias and Automated Decisions: As computers take over boring office work, invisible biases easily sneak into the mix. A broken piece of code might quietly trash a mortgage application or throw away a great resume. It bases the choice on a hidden profile. The person gets a rejection letter, usually with absolutely zero explanation.

The 2026 Regulatory Landscape

Lawmakers worldwide are finally pushing back hard. This year marks a massive turning point for digital rules and corporate behavior.

Huge rulebooks like the European Union’s AI Act are fully active right now. They slap heavy limits on dangerous technology. Meanwhile, dozens of US states rolled out tough privacy laws that demand total honesty from tech companies. Businesses face strict legal orders to tell the public whenever a machine makes a major choice about a human life. Consumers actually hold real power again. They can demand a look at their files, force fixes, or completely scrub their names from corporate servers.

AI as a Digital Defender

Strangely enough, the exact same tech causing these nightmares also acts as the ultimate shield. Artificial intelligence is completely rewriting the cybersecurity rulebook.

Modern data defense relies heavily on smart threat detection. Clever networks watch internet traffic around the clock. They spot weird behavior and shut down hacks long before human security guards even finish their morning coffee. It also drives better ways to hide identities. Companies can track big shopping trends without ever seeing a specific name or street address.

Strategies for Protecting Vital Information

With the internet getting messier by the minute, folks need solid plans to lock down their critical records. Tossing important papers into a messy email folder or a dusty metal filing cabinet is just asking for trouble. Those old methods simply cannot survive modern cyber attacks. They also fail completely during sudden physical emergencies.

Switching to secure, encrypted digital storage offers a much stronger defense. Platforms offering independent, password-protected electronic safe deposit boxes keep life insurance policies, legal contracts, and medical histories totally out of reach from snooping data scrapers. Putting this vital information inside a heavily locked cloud vault guarantees families can grab exactly what they need during a crisis. At the exact same time, the data stays totally hidden from digital thieves.

The Future of Digital Privacy

The collision between smart machines and data privacy stands as the defining tech battle of 2026. The everyday perks are super obvious. But the background risks demand real attention. Staying updated on legal rights gives regular people a fighting chance. Plus, leaning on heavily encrypted storage for major documents lets individuals walk through this new era safely. Taking a few smart steps right now protects immediate privacy while securing a solid, long-term digital legacy.

Public WiFi vs. Your Data: Why You Need a Secure Vault

January 28, 2026

The Open Window

A traveler sits at a crowded airport gate. The flight is delayed. Boredom sets in. The phone comes out, and there it is: “Free Airport WiFi.”

Click. Connected.

It feels like a small victory. A chance to check a bank balance, pay a credit card bill, or look up a policy number.

But that click? It is the digital equivalent of leaving a house key under the doormat and hoping no one looks.

In 2026, we treat our phones like fortresses. We lock them with faces and fingerprints. Yet, the moment we connect to an open network, we lower the drawbridge. We invite the world in. And the world is watching.

The Invisible Eavesdropper

Here is the ugly truth about public internet: it is loud.

When data leaves a phone on a secure home network, it whispers. On public WiFi, it screams.

The danger isn’t usually some master criminal in a hoodie. It is often just software. Simple, cheap scripts running on a laptop three seats away. These programs are like digital vacuums. They suck up everything floating through the air.

- The Man-in-the-Middle: A hacker cuts in line. The user sends a password to the bank. The hacker catches it, copies it, and then passes it to the bank. The login works. The user has no idea they just handed over their keys.

- The Fake Twin: You see a network called “Coffee_Shop_Free.” It looks real. It isn’t. A scammer set it up five minutes ago. Connect to it, and the device effectively belongs to them until you disconnect.

The “Inbox” Mistake

Fear makes people do silly things. When travelers get nervous about logging in, they turn to an old, bad habit: The Email Search.

“I won’t log in,” they think. “I’ll just find that PDF I emailed myself.”

This is a disaster.

An email inbox is not a safe. It is a glass box. Email accounts are the most hacked targets on the planet. If a thief gets into an email account, they don’t just read letters. They find the tax returns from 2024. They find the scan of the child’s birth certificate. They find the list of “backup codes.”

Using an inbox to store life’s vital documents is like hiding jewelry in a clear plastic bag. It doesn’t work.

The Real Fix: A Digital Vault

So, what is the answer? Carry a filing cabinet? Never go online?

No. The answer is a Secure Digital Vault.

This is where platforms like InsureYouKnow.org step in. They aren’t storage bins. They are armored trucks.

1. It Shreds the Data A real vault uses encryption that mimics the banking world, like Amazon Cloud security. If a hacker snatches a file from the air, they don’t get a readable document. They get noise. A jumbled mess of code that means nothing. The thief gets the envelope, but they can never read the letter.

2. Nobody Knows the Code Privacy matters. The best systems run on “zero-knowledge” rules. That means the company holding the data doesn’t have the password. Even if they wanted to look, they couldn’t. The user holds the only key.

3. Get In, Get Out With a vault, the data lives in the cloud, not on the device. A user can log in on a hotel computer, check a passport number, and vanish. No files left in the “Downloads” folder. No trail for the next guest to find.

Peace of Mind

Security usually feels like a headache. Extra steps. More passwords.

But actually? It is freedom.

It is the ability to lose a wallet in Paris and not fall apart. Why? Because the backup copies of every card and ID are sitting behind an iron door in the cloud. Accessible. Safe. Ready.

Public WiFi is fine for reading gossip columns or checking the weather. But for the heavy stuff like the money, the legacy, and the identity, stay off the open road. Put the valuables in a vault. Lock it up. Then go enjoy the coffee.

Why Freelancers Need Vault for Business, Insurance and Personal Docs

December 3, 2025

Running a small business or working independently as a freelancer can be incredibly rewarding, but it also comes with a unique kind of pressure. There is no support team to handle accounts, filing, legal paperwork or insurance policies. Everything falls on one person. And when documents get scattered across laptops, email inboxes, envelopes, and drawers, that pressure doubles.

Many professionals don’t realise the value of having one organised vault for business, insurance, and even personal documents until something goes wrong like a tax review, a lost invoice, a sudden medical emergency or an unexpected client dispute. Situations like these can turn a normal week into chaos if the necessary files aren’t available when they’re needed.

The Hidden Risk Behind Scattered Paperwork

Almost every freelancer or business owner ends up collecting a long list of important documents over time:

- Contracts and NDAs

- Tax records and GST filings

- Business registration and licenses

- Insurance policies

- Personal documents like PAN / Aadhaar / passport copies

- Client invoices and payment proofs

When these are stored in different places some printed, some emailed, some saved on a mobile phone, some forgotten on a hard drive it becomes hard to track what exists and what is missing. Searching for one paper in the middle of work is stressful and wastes valuable time that could be spent earning money.

It is not just about convenience scattered documents increase the chances of financial loss, missed tax claims, denied insurance claims and even legal trouble.

Why a Single Vault Makes Life Easier

Keeping all important documents in one vault (preferably digital) can completely transform the way a business operates. A well-organised vault helps in:

Faster Access When Needed

Instead of digging through old emails or piles of files, documents are found in seconds. During tax season, project negotiations, audits or emergencies, this makes an unbelievable difference.

Confidence with Clients and Authorities

Being able to quickly retrieve contracts, invoices or payment receipts shows professionalism. It also protects the business during disputes or late payments.

No More Panic During Emergencies

If a device breaks, a document goes missing or an accident occurs, a vault ensures that everything is backed up and safely stored.

Clear Separation of Personal and Business Finances

Many freelancers mix personal and business papers by accident. Keeping them in labelled folders inside one vault keeps everything organised without confusion.

Which Documents Should Be Included?

A good vault should include every document that is hard to replace, legally important or financially relevant. For example:

Business-related documents

- Licenses and registrations

- Client contracts and project agreements

- Invoices sent and payment receipts

- Expense proofs bills, subscriptions, travel, utilities

- Bank statements and annual reports

Insurance-related documents

- Health insurance policies

- Life insurance details

- Business and asset insurance

- Renewal receipts and claim history

Personal documents

- Identity proofs such as Aadhaar, PAN, Passport

- Important legal documents

- Nominee details

Keeping everything in one vault does not mix the documents it simply allows them to be stored together but categorised, making access extremely efficient.

Digital Vault vs Physical Storage Which Is Better?

Some business owners still rely on physical files, and while that is familiar, it has limitations. Paper can be misplaced, damaged by water or fire and is hard to access when travelling or working remotely.

A digital vault has several advantages:

- Documents can be accessed anytime, even while travelling or from another device

- Multiple categories and labels reduce confusion

- Search options make it easy to locate files quickly

- Backup storage ensures documents are not lost

- Sensitive information can be password protected

For professionals who work across locations or serve international clients, digital access becomes even more valuable.

Real-World Scenarios Where a Vault Saves the Day

A secure, organised vault may feel like an optional system until the moment it becomes essential:

- A client wants to verify payment for an old invoice

- A large company payroll team requests old tax receipts for onboarding

- A medical emergency requires quick access to insurance details

- A visa form needs a scanned copy of passport and financial proof

- A GST or income tax review asks for expense records from previous years

Having everything stored neatly in one place turns stressful events into simple tasks.

A Small Habit That Leads to Big Stability

Building a vault doesn’t require complicated software or a huge investment. It only needs a habit: every time an important document arrives, store it in the vault immediately. Small, consistent organisation protects both personal and professional life in the long run.

For freelancers and small business owners, a vault is not just storage. It is preparation. It is peace of mind. It is a safety net during the uncertain moments that every business eventually faces.

Final Thought

Success in business isn’t only about skills or marketing. It is also about stability and preparedness. Keeping business, insurance and personal documents in one secure vault gives a professional the confidence to grow without fear of losing control over paperwork. With organised records, business becomes smoother, income becomes predictable and stressful situations become manageable.