Category: Financial

Buying a Home When Interest Rates are High

August 1, 2026

If you’ve been waiting for mortgage rates to fall before buying a home, you’re not alone. Experts say the decision isn’t as simple as waiting for lower rates. The better question is whether buying makes sense for your finances today.

According to a recent Rocket Mortgage survey, nearly 60% of Americans said that they would not start looking for a house now. The top three reasons for staying out of the market are high home prices, insufficient savings, and high mortgage rates. In the last five years:

- Home prices increased from $368,000 to $411,000;

- Mortgage rates increased from under 3% to over 6%; and

- Household debt increased from $96,000 to $105,000, while average wages adjusted for inflation remained flat.

Evaluate Your Situation

Mortgage rates generally move with the yield on 10-year U.S. Treasury notes, which are influenced by investor expectations and Federal Reserve policy. As of June 2026, an average 30-year fixed-rate mortgage rate stood at 6.58%. The Fed lowered the rate three times in 2025, but has kept the rate stable so far this year. “It’s not just about rates for homebuyers, but rather the full financial picture of buying,” said Lisa Sturtevant, chief economist at Bright MLS. “Home prices hit record highs this summer in many markets across the U.S. while higher gas prices and concerns about overall inflation rising have created more financial strain for would-be buyers.”

Here are some factors to consider when deciding whether to buy:

- Stability: Do your job and your paycheck seem secure? Do you intend to stay in one place for several years?

- Lifestyle: Can you afford the inevitable maintenance, repair, and insurance costs that come with owning a home?

- Savings: Do you have enough for the down payment, closing costs, moving expenses, and other expenses (e.g., title searches, home inspections, attorney fees)?

- Debt: How much debt (student loans, car payments, credit cards, medical bills) are you carrying?

- Credit: Is your credit score in the neighborhood of 740 or above?

“If your finances feel shaky — for example, you’re worried about job security or paying bills — it’s wise to hold off,” advises Abby Badach Doyle of NerdWallet. “If your income is steady and your budget says the numbers work, don’t let scary ‘what if’ headlines throw you off track.”

Know What You Can Buy

Before you set your sights on your dream home, do some research to answer the following questions:

- Can you increase your income, or reduce your expenses, or both?

- How much can you pay toward a down payment?

- Would you consider buying in a lesser-known area or an area further from your job?

- Are you looking for a fixer-upper, an older home, or new construction?

- Would you consider a condo or a townhome, rather than a single-family home? If so, don’t forget to factor in the HOA fees.

- Are you a veteran? If so, you might qualify for a VA loan, which has some advantages over a regular bank loan.

- Would a 15-year mortgage be more suitable than a 30-year mortgage for your situation?

- Would you consider an adjustable-rate mortgage, as opposed to the standard fixed-rate mortgage (with the commitment to refinance when the rate goes down)?

- Is a rate buydown — in which you pay up front to lower the interest rate — within your budget?

Seek Professional Help

The U.S. Department of Housing and Urban Development (HUD) works with non-profit organizations that counsel homebuyers. Check with the Consumer Financial Protection Bureau for guidance. Licensed real estate agents have expertise in local markets. Loan officers at banks and credit unions can help, as can real estate brokers licensed through the Nationwide Multistate Licensing System.

Prepare for a Worst-Case Scenario

A survey by Clever Real Estate found that nearly half of new homeowners struggled to make mortgage payments and took on additional debt because they:

- Purchased a home over their budget;

- Accepted a higher interest rate than planned;

- Compromised on their priorities, especially home prices; and

- Confronted excessive maintenance costs.

Although your basic mortgage payment will be locked in for the life of the loan, all other costs associated with buying and owning a home will increase over time. The best scenario for a homebuyer is for both interest rates and home prices to drop, but it is hard to predict when (or whether) those two factors will coincide. Experts can calculate potential trends based on past and current data, but you can’t plan to buy a house based on what the mortgage rate might be in three years.

“The truth is, the right time to buy is when it makes sense for you,” says Doyle.

Renting Your First Apartment? The Rent Isn’t the Biggest Expense

July 15, 2026

Nobody warns you that the most expensive part of renting your first apartment happens before you move in. The monthly rent may fit your budget, but that’s only the beginning. By the time you’ve paid the application fee, security deposit, utility fees, renters insurance, bought a few pieces of furniture, and stocked your kitchen and bathroom, your “affordable” apartment may have already cost several thousand dollars.

It’s no surprise that in many college communities, students now spend more on housing than on tuition. Renting your first apartment is an exciting milestone, but it’s also one of the biggest financial commitments you’ll make during college. With the median asking rent for an apartment in the United States hovering around $1,667 a month, understanding the true cost of renting can help you avoid expensive surprises and find a place that fits both your lifestyle and your budget.

Look Beyond the Monthly Rent

When comparing apartments, don’t stop at the advertised rent. Ask for a complete breakdown of what you’ll pay before move-in and every month afterward. Most first-time renters should budget for:

- Application fee

- Security deposit

- First month’s rent

- Utility or community fees

- Renters insurance

- Parking fees, if applicable

- Furniture and household essentials

- Pet fees and deposits

- Moving expenses

According to a budgeting guide from The Student Sublet, many first-time renters underestimate the cost of everyday items like cookware, shower curtains, cleaning supplies, lamps, trash cans, and basic kitchen utensils. Individually, they don’t seem expensive. Together, they can easily add hundreds—or even thousands—of dollars to your move-in costs. Monthly expenses can also be higher than expected. While many student apartment communities include internet, they often charge utility or community fees that cover other services and common-area maintenance. Before signing a lease, ask exactly what’s included in your rent and what you’ll be expected to pay separately. Some costs to watch out for include:

- Electricity: Budget $30–$80 per month

- Gas and Heating: Budget $20–$60 per month

- Water and Trash: Budget $15–$30 per month

- Parking: Budget $80-$300 per month

Build Your Budget Before You Apartment Shop

It’s easy to fall in love with an apartment that’s just a little nicer than the one you planned to rent. Instead, decide what you can comfortably afford before you begin touring properties. Rent is only one part of your monthly budget. You’ll also need money for groceries, transportation, textbooks, laundry, entertainment, and the occasional unexpected expense. According to Bola Sokunbi, founder and CEO of Clever Girl Finance, budgeting isn’t about limiting yourself—it’s about making intentional decisions. “A budget gives you permission to spend because you’ve already made a plan for your money,” says Sokunbi.

Compare the Total Cost of Living

The apartment with the lowest rent isn’t always the least expensive place to live. For example, an apartment that costs $75 more each month may actually save you money if it includes parking, in-unit laundry, or is close enough to campus that you don’t need to pay for parking permits or as much gas. On the other hand, a cheaper apartment may require a longer commute, separate utility payments, laundry fees, or higher transportation costs that quickly erase the savings. Think about your total monthly cost, not just your monthly rent.

Roommates Can Save More Than Rent

For many students, living with roommates is one of the smartest financial decisions they can make. Lauren Sonnenberg, a writer for Forbes, estimates that students who share an apartment rather than live alone can save more than $15,000 over four years. Those savings come from more than splitting the rent. Roommates often divide utility costs, household supplies, streaming services, and other shared expenses, which can quickly add up.

Sharing an apartment, however, requires more than finding someone to split the bills. Before signing a lease together, talk about expectations.

- How will bills be divided?

- Will groceries be shared?

- Who buys household supplies?

- Are overnight guests okay?

- What are the expectations for cleaning?

- What happens if someone wants to move out before the lease ends

Don’t Pay for Amenities You Won’t Use

Apartment tours are designed to impress prospective renters. Resort-style pools, rooftop lounges, game rooms, golf simulators, coffee bars, and fitness centers all look appealing. But ask yourself one simple question: Will I actually use them? If you’re spending most of your day in class, studying, or working, those amenities may not justify the higher rent. Instead, prioritize the features that will make your daily life easier:

- A safe neighborhood

- Reliable maintenance

- Laundry facilities

- Good lighting and secure entry

- A reasonable commute to campus

- Space to study without distraction

Read the Lease Carefully

Most students spend more time touring an apartment than reading the lease. Before signing, understand when rent is due, how maintenance requests are handled, whether parking is included, who pays for repairs, what happens if you break the lease early, and whether subletting is allowed. If something doesn’t make sense, ask questions before signing. A five-minute conversation today can prevent months of frustration later.

Furnish Slowly

Your first apartment doesn’t need to be fully furnished on move-in day. Start with the essentials: a bed, a desk, basic cookware, towels, cleaning supplies, and a few kitchen items. Shop at thrift stores, estate sales, or on Facebook Marketplace, or ask family members if they have furniture they’re no longer using. You can always add decorative items, additional furniture, and small conveniences over time. Buying everything at once often leads to unnecessary spending—and unnecessary debt.

Protect Yourself from Day One

Before moving in, photograph every room and document any existing damage. Keep copies of your lease, receipts, and maintenance requests. Renters insurance is one of the least expensive ways to protect your belongings if they are damaged or stolen.

Plan a Memorable Vacation Without Breaking the Bank

July 1, 2026

Most vacations end twice. The first time is when you unpack your suitcase. The second is when the credit card bill arrives. That second ending has become increasingly familiar to American families. Nearly eight in 10 Americans plan to take at least one vacation each year, yet the average one-week vacation for a family of four costs about $8,000. For many households, the desire to get away competes with rising prices, making travel feel more like a financial burden than a chance to recharge.

Fortunately, a memorable vacation doesn’t have to come with a luxury price tag. With thoughtful planning and making a few strategic choices, you can enjoy travel without spending more than you can afford.

Start with Your Budget, Not Your Destination

It’s easy to fall in love with a destination before looking at the price tag. Instead, determine how much you can comfortably spend before browsing flights or hotels. Include transportation, lodging, meals, activities, parking, souvenirs, and a small emergency cushion.

Planning ahead is one of the simplest ways to save money. According to Sally French, a travel expert at NerdWallet, travelers often underestimate everyday expenses. “People often underestimate what they spend while traveling because they only think about airfare and hotels,” says French. “Planning for meals, transportation, and unexpected expenses makes vacations far less stressful.”

Consider one of these budget-friendly destinations:

- Greenville, South Carolina

- Chattanooga, Tennessee

- Rapid City, South Dakota

- Gettysburg, Pennsylvania

- Cincinnati, Ohio

- San Antonio, Texas

- Bentonville, Arkansas

- Clearwater, Florida

MoneyLion has a list of 20 of the cheapest places to travel in the U.S. in 2026.

Be Flexible

Travel during the shoulder season when hotel rates and airfare are often lower. Flying midweek, considering nearby airports, and comparing similar destinations can all stretch your budget.

Save on the Big Expenses

Transportation and lodging usually consume the largest share of a vacation budget, but they also offer the biggest opportunities to save. Choose accommodations with a kitchenette so you can prepare breakfast or pack lunches. Compare the total cost of a hotel—including parking, resort fees, and taxes—not just the nightly rate. Eat where the locals eat instead of near major attractions, and leave a little room in your budget for unexpected experiences that often become the most memorable parts of a trip.

Look for Free Experiences

It’s easy to assume the best experiences come with the highest admission prices. Some of the best vacation memories are free. Walk through a historic downtown, visit a farmers market, hike a scenic trail, or attend a community festival. According to Pauline Frommer, editorial director of Frommer’s Travel Guides, meaningful travel isn’t defined by luxury. “Travel doesn’t have to be expensive to be meaningful. The best trips are often those that allow you to connect with a place and its people rather than simply check attractions off a list,” says Frommer.

Travel writer Rick Steves shares a similar philosophy. “The most memorable travel experiences often happen when you slow down and connect with everyday life,” says Steves.

Don’t Overlook the Staycation

If travel isn’t in the budget this year, consider taking a staycation instead. Reserve a nearby hotel, explore museums you’ve never visited, spend the day at a local park, or try restaurants that have always been on your list. The key is to treat the time as a real vacation. Put away your work email, silence notifications, and resist the temptation to catch up on household chores. Even a weekend spent exploring your own community can provide the change of pace many families need.

With a little planning, you can make your vacation memorable without making it expensive.

Planning for Yourself and Loved Ones After a Cancer Diagnosis

June 15, 2026

The National Center for Health Statistics estimates that approximately 2,114,850 new cancer cases will occur in the United States in 2026. Hearing the words, “You have cancer,” is a moment that is often met with a rush of emotions, ranging from fear to confusion.

“The beginning is the worst because you want all of the answers. You don’t know your staging and your mind goes to a scary place,” says Emily Cheshire, a nursing professor in Colorado diagnosed with breast cancer last year.

While no one wants to think about worst-case scenarios after receiving a cancer diagnosis, taking time to plan ahead can provide peace of mind for both you and your loved ones.

Processing the Diagnosis

You may experience denial as you grasp the reality of your diagnosis. This can give some people the time they need to accept it, but if denial persists, that can stop someone from confronting the condition, delaying potentially life-saving treatments.

By keeping a notebook to write down questions, take appointment notes, and to store all of your medical records, you can begin to feel like you’re staying on top of your health. This level of organization can also help you and your loved ones see the full picture of your care plan.

Take an Account of Your Financials

One practical step is to organize important documents, including insurance policies, treatment options, medical records, medication lists, financial account information, and legal documents. The National Cancer Institute recommends discussing advance directives early and keeping important healthcare documents accessible in case you become unable to communicate your wishes.

Cancer treatment can also create financial challenges. Beyond medical bills, families may face costs related to travel, lodging, lost wages, and caregiving. Ask your healthcare team whether your cancer center offers financial counselors, patient navigators, or assistance programs that can help you understand costs and identify available resources.

Planning ahead also means having honest conversations with family members. Consider discussing who may help manage appointments, make healthcare decisions on your behalf if needed, and store important documents. Advance directives commonly include a living will, trust, and a healthcare power of attorney (also known as medical power of attorney or MPOA), which allows you to designate someone to make medical decisions if you cannot do so yourself.

These conversations can be difficult, but they can also reduce uncertainty and stress for families during a challenging time. Planning ahead does not mean giving up hope. Instead, it helps ensure that your wishes are understood and allows everyone to focus more fully on treatment, quality of life, and time together.

Emotional Toll

Just as cancer takes a toll on your physical health, the mental toll can be just as difficult. Many people experience emotions they’ve never had to deal with, which can intensify them. Feelings may also fluctuate frequently, but all of this is normal.

Some people feel that they have to be strong to protect their loved ones, but seeking support from them or other cancer survivors can be helpful. Others feel more comfortable speaking with a professional counselor or turning to their faith. “I’ve felt a lot of prayers from people, so I feel lifted and supported with that,” says Cheshire. “I don’t know if that’s what helps me have a positive attitude or if it’s the other things I do, but this is about finding beauty and something you’re grateful for while living in uncertainty.”

For many, expressing strong emotions like anger or sadness helps them let go. And even if you prefer not to share what you’re feeling, writing down your feelings can be just as effective. It’s just important to figure out what’s going to be the right outlet for you. By focusing on what you control, you can feel more empowered. Simply staying on top of doctors’ appointments and treatment schedules helps you and your family feel like you’re doing everything in your power to heal.

Turn your focus to strengthening your coping abilities, such as finding your support system of friends and family, and prioritizing what matters most to you. Cultivate a sense of hope by taking part in activities that bring you joy or allowing yourself to be comforted by your spiritual beliefs.

Caring for Your Family

Give those closest to you the space to process what they’re feeling. Let them know that you want them to speak honestly with you about what they’re feeling, when they’re ready to. Open discussions will allow everyone to connect and process the information together.

When you’re ready, ask them for the help you need, including going to doctors’ appointments and sitting through treatments with you. “My wife has been exceptional in taking on a majority of the family responsibilities,” says Kyle Stanfield, an Oregonian dad who has been battling cancer for seven years. “Knowing that you have that support at home is priceless.”

For those who want to help out caregivers but don’t know how, just act. “Check in on them, give them a call, invite them out for a meal or to a movie to take their mind off being a caregiver,” says Stanfield.

With Insureyouknow.org, you can store all of your notes, medical records, and care plans in one place, making it simple for you to stay organized. By periodically reviewing your care plan and then mentally setting it aside, you can free up your mind for everything else you want to focus on right now.

Myths vs. Reality: What a Trust Actually Does

May 1, 2026

A survey by SmartAsset shows that over 60% of Americans with estates exceeding $500,000 opt for a living trust instead of a will. A key reason is that trusts avoid probate, which can reduce delays and eliminate fees that typically range from 3% to 7% of an estate’s value.

Simply put, an estate planning trust is a structure that holds assets, such as property, cash, and investments, in the care of a trustee and directs how they are managed and distributed. A trustee oversees those assets on behalf of beneficiaries, following the terms set by the person who created the trust. “People think trusts are about wealth,” said Terry Ruhe, senior vice president at U.S. Bank. “They’re really about control—who gets what, when, and under what conditions.”

Myth: All trusts are the same

Reality: The structure determines how assets are treated, taxed, and distributed.

Trusts can vary, so choose one that best suits your beneficiaries’ needs and assets.

The revocable living trust is the most common selection because it is flexible and administratively efficient. Such trusts allow changes at any time, and you retain full control. Because you retain control over a revocable trust, the IRS treats its assets as if you still own them. Income is reported on your personal return, and assets remain part of your taxable estate. If you are looking for tax advantages, this type of trust does not offer any.

Irrevocable trusts are used for specific outcomes such as estate tax reduction or asset protection. Irrevocable trusts require giving up control of the assets placed into them. In return, they may reduce estate taxes and provide a level of protection from creditors. Irrevocable trusts can reduce estate taxes, but only when structured correctly and used in the right context. For many estates, the federal estate tax is not triggered, which makes this benefit irrelevant. “Trusts don’t eliminate taxes by default,” Ruhe said. “They have to be designed with that objective in mind.” Changing the terms of this trust at any time is a complex legal process.

A special needs trust allows a beneficiary to receive support without losing eligibility for public benefits. Charitable trusts direct assets for philanthropic purposes. Generation-skipping trusts are used to transfer wealth across multiple generations with tax considerations. “The structure should match the objective,” Ruhe said. “Not the other way around.”

Myth: Trusts are only for the wealthy

Reality: The most common trust is used for administrative efficiency rather than wealth preservation.

Even a modest estate that includes a home, a few accounts, or dependents can benefit from avoiding probate. “Trusts are not just for large estates,” Ruhe said. “They are often used to simplify administration and provide continuity.”

If you have minor children, a trust allows you to control when and how assets are distributed instead of transferring them outright at age 18. If you want someone to step in and manage finances in case of incapacity, a trust allows that transition without court involvement. If you own property in more than one state, your estate may be subject to multiple probate proceedings.

Myth: A will does the same thing

Reality: A will directs assets after death. A trust governs assets before and after.

A will must go through probate, while a trust does not. A trust can manage assets during incapacity and control how distributions are made over time. A will cannot do either without court involvement. Most plans include both documents. The trust handles the assets. The will addresses anything left outside it.

Myth: Trusts are too expensive

Reality: Costs are tied to complexity, and the alternative has its own costs.

A basic revocable trust often costs between $1,000-$4,000. More complex trusts can exceed $10,000, particularly when tax planning is involved. The comparison most people overlook is probate. Court costs, attorney fees, and delays can be significant, especially when real estate is involved. Even in simpler jurisdictions, probate still requires time and administration.

Myth: Creating trust is complicated

Reality: The process is structured. The follow-through is where problems occur.

A trust is created through drafting and signing. After that, assets must be transferred into it. This includes retitling accounts and updating property ownership. Assets left outside the trust may still go through probate, even when a trust exists. Download a checklist to see what is involved in setting up a trust.

“On its most basic level, estate planning allows anyone to have the ability to determine and communicate to the rest of the world how they want their assets to be handled upon their passing,” says Christina Rosas, a member of Bond, Schoeneck & King in Melville.

Myth: Trusts only matter after death

Reality: Much of their value shows up during life.

A trust allows for immediate management of assets if the grantor becomes incapacitated. This avoids court-appointed guardianship and allows for continuity in financial decisions.

Myth: Once it’s set up, it runs itself

Reality: A trust still requires administration.

The trustee is responsible for gathering and safeguarding assets, paying expenses, maintaining records, and making distributions in accordance with the document. They may need to oversee investments, document distributions, and, in the case of irrevocable trusts, file separate tax returns. Trusts should be reviewed every 3–5 years, or sooner if there is a major life change such as a marriage, divorce, birth, death, relocation to another state, or a significant change in assets. Laws change as well, which can affect how a trust functions. Annual check-ins include confirming that assets remain properly titled in the trust, beneficiary designations remain aligned, and the named trustee remains appropriate.

Myth: Setting up a trust is enough

Reality: A trust works only if assets are aligned with it and kept current.

If accounts, property, or beneficiary designations are not coordinated with the trust, those assets may bypass it entirely. This is one of the most common issues. Many trusts are only partially funded, which results in a mix of probate and non-probate administration.

Over time, trusts should be reviewed as assets and circumstances change. The document can be updated, but only if someone revisits it. What matters is not whether a trust exists, but whether it is aligned with the assets, structured for the right purpose, and carried through in practice.

Keep your records safe

InsureYouKnow.org is a safe place to store all the information in case you need to access it remotely – or from the comforts of your own home. The documents are password-protected and use Amazon Cloud encryption to secure each password-protected account. Your password is not known to the site. Only you or someone you share the password with can access your account.

What to Know Before Investing in a Rental Property

April 15, 2026

Even amid inflation and interest rates higher than historical norms, real estate remains a sure investment. “The Wall Street Journal recently reported that in this booming housing market, many homeowners earned more last year from home appreciation than from their jobs,” says Philip White, CEO of Sotheby’s International Realty.

Purchasing an investment property and then renting it out often provides you with more than enough money to pay the property’s mortgage.

If you’re unsure of where to start, here’s everything you need to consider before buying a rental property.

Determine Affordability First

Before you purchase an investment home, you need to be honest about whether you have the finances to do so and the time to commit to property management.

The first thing you’ll need to determine before investing is how much potential income it could provide. There’s a widely-accepted guideline known as the 1% Rule: the monthly rent should be 1% of the purchase price. If a home costs $200,000, then rent should be $2,000 per month.

“Run the numbers like a business. Higher prices are here to stay, so instead of waiting for prices to drop, find the properties that have cash flow,” says Nicole Rueth, founder of The Rueth Team, a mortgage lender. “They’re out there; I know because I’m helping investors find them. If it doesn’t have cash flow on paper, don’t buy it.”

Since your property may not always have renters, it’s important to make sure you can still pay that mortgage and all of your other expenses without relying on monthly rent payments. To avoid financial strain during vacancies, it’s best to have at least two months’ worth of expenses saved.

Work With a Professional

Realtors and professional property managers can help you with the ins and outs of investing in a specific market. “They can help connect you with an expert who can advise on local tax laws and, especially if you’re looking to invest internationally, visa programs that might be available to you,” says White.

Even if you decide to work with a real estate agent, familiarize yourself with the neighborhood you’re buying in. Drive around yourself and look for sales signs, as well as check real estate listings online. Assess proximity to good schools, review nearby commercial and recreational areas, and evaluate the area’s overall aesthetic appeal and safety.

Learn the Rules

No matter where you decide to purchase property, it’s crucial to look into the various regulations and laws that exist in each state or country. “In the city of Naples, you can rent your property for a minimum of 30 days, three times a year,” says Belz. “But if you get just outside the city of Naples, we have a number of neighborhoods without rental restrictions.” An experienced agent will know about these restrictions and can help steer you in the right direction.

To reduce regulations and costs, look for desirable neighborhoods and homes without Homeowners Association (HOA) fees. If you have the time and resources, don’t be afraid of choosing a fixer-upper either. While a fixer-upper will have renovation costs, it can be worth it if you negotiate and save on the asking price.

Manage Your Investment Personally

To eliminate costs on your end, you may opt to manage the property yourself. This is convenient if you live in the area and can stop by the home quickly if needed. But if you don’t live nearby or care to manage your property and tenants personally, then a property management company can help provide the services necessary to keep your investment profitable.

Property managers can also draw on years of experience, such as recommending higher security deposits, pet deposits, and thorough background checks. “Don’t just assume self-managing saves you money,” Ruth says. “If managing tenants stresses you out, costs you time, or makes you hate investing, you’re paying a price either way.”

Find the Right Tenants

Even if they look good on paper, screening tenants thoroughly upfront can save you time and money later. You’ll want to verify their current employer and income, contact previous landlords, and run a criminal background check. If anything concerning arises or doesn’t feel right, move on to the next applicant. Ultimately, it’s your decision who you rent to, but a bad experience with tenants can significantly damage your property and diminish your return on investment.

Even if you choose to manage your property personally, a property management company can still help with drafting rental agreements. It’s well worth the cost to have a professional make sure the lease includes everything it should. The more you establish upfront in your lease, the better experience you’ll have with your tenants in the long run.

Presentation and Upkeep

Properties that generate the most revenue are usually those that have been recently updated. “By far the best way to maximize your return is having a really well-kept property,” Belz says. “It sounds obvious, but it’s critical.” Hiring a professional photographer for listing photos is also highly recommended.

Investors often put little work into a property after purchase, but when tenants move out, upkeep is just as important. Between renters is the best time to plan deep cleaning, new paint, pest control, addressing deferred repairs, and other design considerations, such as bathroom remodels.

Even with the best tenants, wear and tear will occur over time. Investors need to prepare for these in-between tenant costs, which can range from appliance upgrades to a new roof.

Managing just one property can quickly become a part-time job. You can utilize Insureyouknow.org to keep track of expenses, tenant leases, maintenance schedules, and any other documents involving property management. By treating your investment like a business, property management will become second-nature, making it possible for you to invest in even more over time.

How to Tell Your Beneficiaries About Life Insurance Without Stress

March 19, 2026

Billions of dollars in life insurance death benefits sit unclaimed across the United States annually. Families often desperately need these funds, and the policies themselves remain completely valid. The problem usually stems from a simple communication gap where the named individuals had no idea the coverage even existed.

Industry investigations revealed major insurers releasing over $7 billion in previously forgotten benefits between 2006 and 2016, but only after regulators forced them to cross-reference death records. Experts strongly believe the actual amount of missing money is substantially higher. Current data points to roughly $6 billion in unpaid benefits sitting in limbo, largely caused by outdated contact details and uninformed relatives.

This situation is entirely preventable. Fixing the issue does not demand expensive attorneys, formal family meetings, or highly uncomfortable discussions. Policyholders just need to share the right details clearly and proactively so the information actually sticks.

Why Beneficiaries Remain in the Dark

Policyholders avoid talking about their coverage for several reasons. Some individuals harbor superstitions regarding death. Others fear the topic might sound morbid or cause unnecessary distress among relatives. A large portion of people simply assume loved ones will figure everything out when the moment arrives.

Insurance providers lack automatic alert systems to notify anyone when a policyholder passes away. No alarm sounds and no automatic check gets mailed. Companies usually only discover a death has occurred when a relative reaches out directly. That requires the family to actually know about the coverage beforehand.

The most frequently forgotten accounts include decades-old plans, employer-sponsored group coverage from previous jobs, and small whole-life policies intended for final expenses. Important paperwork easily gets lost during house moves. Premium drafts might quietly exit a bank account for years without a surviving spouse noticing. Lacking a clear handover of documents leaves surviving relatives guessing and frequently finding nothing.

Starting the Conversation Without Uncomfortable Feelings

Discussing these financial safeguards never has to sound like a grim announcement. Financial planners frequently suggest centering the talk on care and future preparation instead of loss. A simple mindset shift changes everything. The focus moves away from passing away and toward actively protecting important family members.

Several approaches help these talks feel completely natural:

- Tie it to a life event: Welcoming a new grandchild, navigating a health scare, or updating a will provides an easy opening. Someone might say, “While getting these organizational tasks done, it is important to share the details of this life insurance coverage.”

- Frame it as a gift: Informing dependents about their financial protection acts as a generous gesture. Policyholders can position the talk as offering clarity. A good phrase to use is, “To prevent any future scrambling, here are the essential details needed for the records.”

- Use a document review as the opener: Checking financial records every year builds excellent habits. Inviting an adult child or spouse to observe the review creates a low-pressure environment to share policy specifics naturally.

Essential Information for Beneficiaries to Know

Mentioning the mere existence of a policy falls short of being helpful. Grieving relatives require highly specific data to process claims quickly. Handing over this data early minimizes delays, lowers stress levels, and guarantees the funds reach the intended destinations promptly.

The National Association of Insurance Commissioners recommends granting access to the following specific details:

- The exact name of the provider and the full name of the insured person as listed on the contract

- The specific policy number and the exact type of coverage selected

- The total death benefit value alongside any attached riders

- Direct contact details for the provider or the managing agent

- The exact physical or digital location of the official documents

- Clear distinctions between primary and contingent individuals along with the designated percentage splits

Any individual holding multiple plans through an employer, private company, or professional group must document and share every single one. Relatives frequently uncover hidden coverage months or years after a funeral, making thorough documentation crucial.

Explaining Primary and Contingent Beneficiaries Clearly

The difference between primary and contingent designations frequently causes confusion. A primary designation puts a person or entity first in line for the funds. A contingent designation acts as a backup, stepping up only if the primary individual cannot collect the funds due to passing away themselves.

Everyone named on the contract must understand their exact role. Splitting funds requires each party to know their specific percentage share. Transparent communication stops arguments and blocks potential legal headaches later on. It helps to remind everyone that designated beneficiaries on a contract will overrule any instructions written into a standard estate plan.

Keeping Documents Accessible During Critical Moments

Spoken words offer a solid starting point but fall short long-term. People forget things quickly while grieving. Physical papers easily succumb to fires, floods, or misplacement during a move. The safest strategy pairs direct communication with a highly secure, centralized storage spot for all vital records.

Tucking the contract next to estate papers represents the traditional route, yet it carries flaws. Locking physical copies inside a bank safe deposit box often requires the policyholder to be present for access. This creates massive roadblocks for relatives at the worst possible time.

Digital platforms solve this accessibility problem beautifully. Encrypted online vaults allow users to stash life insurance details, medical coverage, banking numbers, and legal files in a single hub. Trusted contacts receive access to designated files, guaranteeing the correct people find the right information instantly from any location.

Updating Beneficiary Designations and Communicating Changes

Designations must evolve alongside major life shifts. Marriages, divorces, new babies, or the loss of a designated relative demand an immediate contract review. Neglected updates stand out as a top reason for delayed payouts and legal disputes. Industry research shows roughly 8% of claims hit roadblocks specifically due to obsolete contact data.

Updating a file means everyone involved needs a notification. Swapping out a former spouse for a new partner means both sides require an update, when appropriate. These chats might feel slightly awkward, but leaving a grieving family to fight over uncertain terms causes much deeper pain.

Creating an annual calendar alert to verify these designations builds a highly effective habit. Digital platforms often send automated monthly nudges to check for necessary updates. This turns file maintenance into a seamless part of standard financial upkeep.

Early Conversations Protect Loved Ones Tomorrow

Sharing policy details ranks among the most impactful financial steps a person can take. The process requires zero legal background and avoids feeling overly morbid. It just takes a willingness to speak directly and the discipline to organize the supporting paperwork.

Relatives who understand the coverage, know the storage location, and possess the correct contact numbers can actually focus on healing instead of hunting down forms. Providing that exact peace of mind remains the core purpose of buying coverage. The product only works if the protected individuals know it exists.

Utilizing an encrypted digital vault to hold these financial and legal records proves incredibly practical. This ensures the preparation goes far beyond spoken words. It builds an adaptable record that follows a family through every life stage, waiting quietly until the exact moment it becomes necessary.

Property Tax Exemptions for Seniors: What Every Homeowner Needs to Know

March 15, 2026

For local governments in the United States, property taxes are the primary source of revenue. However, property tax has historically been among the most unpopular taxes. In November 2025, the City of Atlanta and Fulton County, Georgia, overwhelmingly approved new homestead tax exemptions for seniors, with 73% of 91,169 Atlanta voters supporting the measure.

As home values rise, property taxes have become a growing burden for homeowners nationwide, particularly for older Americans on fixed incomes. Many of them worry that the property taxes alone will eventually price them out of their homes.

To mitigate this, nearly every state offers a homestead exemption for residential property. However, few seniors realize they may qualify for additional exemptions. “These are very big exemptions,” says Colton Pace, property tax expert and CEO of Ownwell. “It’s an aggressive way to keep seniors in their homes.”

Here’s everything you need to know about state property tax relief for seniors and whether or not you qualify.

How Exemptions Work for Seniors

To ease the financial strain of property taxes, 16 states and the District of Columbia offer exemptions for qualifying seniors. Senior property tax exemptions lower your tax bill by reducing the taxable value of your home.

Alaska, for instance, waives the first $150,000 of the assessed home value for homeowners aged 65 and over, while the District of Columbia cuts property taxes in half for all qualifying seniors.

Most states have a government website dedicated to taxes that lists local rules for senior property tax exemptions. A Google search for “senior property tax exemptions + your state” should find yours.

Don’t Forget Freezes, Credits, and Deferrals

In addition to property tax exemptions, many states also offer:

- Property tax freezes, which lock in your current tax amount, prevent increases down the line if your home’s value rises. Both Arizona and Arkansas freeze the property value of a primary residence for qualifying seniors, preventing increases in assessed value.

- Tax credits provide a direct reduction in your tax bill. Instead of adjusting your home’s value to your tax benefit, credits subtract a set amount from the total you owe. New Jersey’s Stay NJ program, for example, reimburses 50% of property tax bills, with a limit of $6,500, and in Wisconsin, eligible seniors receive both homestead and school property tax credits.

- Deferrals allow seniors to delay paying their taxes, sometimes in exchange for a lien against their home. When the owner dies or decides to sell their home, the state collects the tax debt, often with interest. In Maine, eligible seniors may defer their taxes until after sale or death, and in Vermont, they may also defer their taxes until sale or death, with a 0% interest rate.

Legislation is Ongoing

Many states continue to introduce legislation to expand senior tax benefits. Local governments in both Maine and Ohio are trying to eliminate property taxes for qualifying seniors altogether.

In December 2025, Rensselaer County, in Troy, New York, proposed a law to provide disabled seniors with additional tax benefits. “This law delivers real relief for Troy’s seniors and residents living with disabilities who have been struggling with rising costs,” says Mayor Carmella Mantello. “We are making sure our most vulnerable neighbors can stay in their homes and maintain their quality of life.”

Know if You Qualify

In addition to meeting an age requirement, states also require income brackets to fall within and proof of residence in the home for a certain amount of time. Qualifications vary from state to state and sometimes yearly, so it’s essential to meet with a county assessor at your local clerk of courts or a financial advisor who specializes in retirement.

Putting in the time to know whether or not you qualify for any property tax exemptions can be time-consuming, but well worth the chore. According to a recent report by Realtor.com, as many as 40.5% of homeowners could be overpaying on their property taxes.

Saving Home

Ultimately, these senior property tax exemptions are intended to ease the burden of rising costs during retirement and help keep seniors in their longtime homes and communities. Most seniors live on a fixed income, so when taxes become too difficult to pay due to rising home values, even seniors with moderate incomes can find themselves struggling to remain in the home they’ve spent most of their adult life in.

With Insureyouknow.org, seniors can keep all of their tax research, financial records, and other proof of residential requirements in one organized place. Remember that while it may feel like a lot of work in the beginning to gather this information, you are likely going to save yourself enough money on those pesky property taxes to make it well worth it.

2026 Student Loan Defaults: Secure Your Financial Records

March 6, 2026

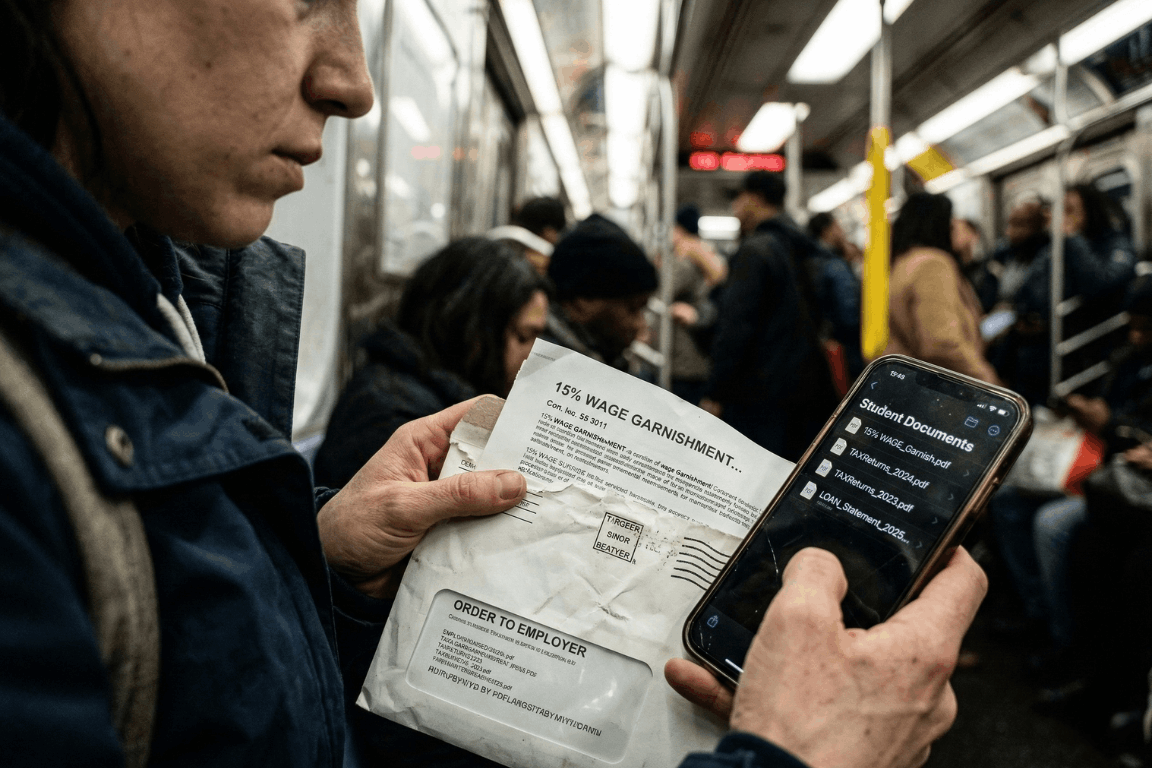

A massive financial wall hit millions of Americans earlier this year. Pandemic payment pauses are officially ancient history. The temporary relief programs dried up entirely. After months of messy court battles regarding income-driven repayment plans, the federal government decided to bring back its heaviest collection tools. Starting in early 2026, the U.S. Department of Education began sending administrative wage garnishment letters to defaulted borrowers. The numbers from major credit bureaus, like Experian, look pretty grim. The entire country is watching a massive wave of loan delinquencies happen in real time. People are suddenly staring down severe financial penalties. Getting through this economic squeeze requires a lot more than just reading news updates. It demands immediate, highly organized access to specific financial paperwork.

The 2026 Student Loan Landscape: A Shocking New Data Trend

So, who is actually defaulting right now? Historically, student loan defaults mostly hammered sub-prime borrowers. That whole narrative flipped completely upside down in 2026. Recent reports from credit bureaus reveal something entirely unexpected. Nearly a quarter of newly defaulted borrowers belong in the “prime” credit tier or even higher. These are the exact demographics the financial industry usually views as incredibly stable.

With over 5 million borrowers currently sitting in default status, and millions more falling behind every month, the economic pain is obvious. Borrowers are stuck navigating a bizarre maze of constantly changing payment plans. Making things worse, millions of accounts got bounced around between different private servicing companies over the last two years. Monthly payments got lost in the mail. Crucial paperwork simply vanished. Hold times to speak with basic customer service stretched into hours. Once a federal student loan reaches 270 days past due, it hits official default status. At that specific moment, the government gets to use an administrative superpower that regular credit card companies cannot even touch. They can literally take wages without ever stepping foot inside a courtroom.

Understanding Administrative Wage Garnishment: The 15% Reality

The fallout from a federal default happens fast. Through a process called Administrative Wage Garnishment (AWG), the Department of Education can legally force an employer to pull up to 15% of a borrower’s disposable pay. Disposable pay simply means the cash remaining after legally required deductions, like federal and state taxes, come out of the check.

Federal law does leave a very small safety net in place. Borrowers get to keep a weekly take-home amount equal to at least 30 times the federal minimum wage. But for anyone living from one paycheck to the next, suddenly losing 15% of their income is pure disaster. It usually means missing the rent, skipping the grocery store, or defaulting on other credit cards. Before the garnishment actually kicks in, the government must send a 30-day advance written warning. That specific 30-day window is basically everything. It acts as the only real timeframe a borrower gets to object or set up a different payment plan before their paycheck actually shrinks.

How to Stop Garnishment: The Heavy Burden of Proof

Borrowers holding a garnishment notice still carry some legal rights. During those 30 days, individuals can officially demand a hearing to stop the withholding order. They might attempt to prove extreme financial hardship. Or, they could try applying for federal loan rehabilitation. Rehabilitation usually involves agreeing to make nine on-time payments over a 10-month window to get the loan back on track.

Another route involves submitting a formal financial hardship appeal. Winning this appeal means legally proving that a 15% pay cut makes buying basic survival items impossible. The government looks at documented living expenses and compares them against very strict IRS Allowable Living Expense guidelines. If a family spends more on food or housing than the IRS thinks is necessary for that specific family size, the extra amount gets totally ignored. Proving hardship is notoriously difficult. Using these rights is never a walk in the park. It requires gathering highly specific legal and financial records immediately. In these types of administrative hearings, the burden of proof lands squarely on the borrower.

The Critical Role of Organized Financial Documents

Sloppy paperwork turns a bad money situation into an absolute nightmare. When the garnishment letter shows up, the clock ticks fast. Spending hours digging through cluttered email inboxes for old messages from loan servicers wastes valuable time. Tearing up the living room looking for utility bills to prove basic living expenses just fuels the anxiety. If a borrower fails to hand over the correct evidence within 30 days, their employer receives the order. The garnishment starts.

This explains exactly why relying on a secure, independent electronic safe deposit box changes the playing field. Keeping a dedicated digital vault for vital life information ensures nobody gets blindsided by aggressive debt collectors. Storing all important financial, legal, and contractual documents in one simple location gives borrowers a huge advantage. They can instantly grab the exact proof they need to protect their paychecks and negotiate with default resolution teams.

Essential Documents to Secure in a Digital Vault

To build a strong defense against a default warning, individuals should make sure the following documents are digitized, safely uploaded, and ready for action:

- Original Loan Agreements and Master Promissory Notes: Finding original contracts immediately helps verify the true debt amount. It also spots accounting errors and confirms which company actually owns the loan today.

- Complete Tax Returns: Proving financial hardship or enrolling in an income-driven repayment plan means submitting paperwork. The Department of Education demands recent federal and state tax returns before they even start talking.

- Official Pay Stubs: Current pay stubs are absolutely required to figure out actual disposable income. They also help verify that any proposed wage garnishment does not illegally drop below the minimum wage protection limit.

- Household Expense Records: Tracking basic living costs is a strict requirement for hardship appeals. Think about rent agreements, mortgage papers, utility bills, health insurance premiums, and pharmacy receipts. These papers help prove that living expenses are reasonable and fit within tight IRS standards.

- Correspondence with Loan Servicers: A strong paper trail of older payments, approved forbearances, and emails with the loan servicers can literally save the day. This proof is extremely important if someone needs to show a loan was wrongfully thrown into default in the first place.

The Absolute Security of Zero-Knowledge Storage

Privacy is absolutely non-negotiable when dealing with highly sensitive financial details. Relying on physical metal filing cabinets leaves people wide open to lost papers, house fires, or basic theft. Depending on regular, unencrypted email folders or a messy computer desktop basically hands sensitive financial data directly to hackers. Cybercriminals routinely target email servers specifically to find W-2 forms and tax returns. Once they grab those files, identity theft is pretty much guaranteed.

Using a specialized platform built with heavy-duty cloud encryption makes sure financial data stays completely private. The absolute best platforms run on Amazon cloud encryption mixed with a “zero-knowledge” setup. In a zero-knowledge system, only the actual account owner knows the password. The site administrators never get to see it. That means absolutely nobody else can ever gain access, view the files, or mine the stored documents to sell the data.

Strategic Document Sharing with Trusted Partners

Fixing a defaulted student loan is almost never a solo job. Borrowers usually need to bring in certified financial planners, tax accountants, or specialized student loan lawyers to help decode the messy federal rules.

Advanced secure portals allow individuals to selectively share specific document folders with these exact trusted partners. Sending unencrypted PDFs of tax returns and pay stubs back and forth through regular email is a massive cybersecurity hazard. Instead, account holders can simply give a legal advisor temporary, secure access to the required files right inside the encrypted vault. This targeted sharing feature speeds up the whole default resolution process, keeps communication secure, and leaves the rest of the vault totally locked down. Setting up automatic monthly reminders inside the portal also helps users routinely update their financial snapshots, keeping their defense strategy completely fresh.

Facing economic uncertainty requires a solid game plan. The return of federal student loan wage garnishments in 2026 creates a massive hurdle. Credit bureau data clearly shows that financial distress is hitting borrowers across every single demographic right now. Surviving this wave of defaults demands aggressive, proactive money management and flawless record-keeping. Centralizing vital financial documents into a secure, encrypted digital safe deposit box lets individuals tackle economic chaos with total confidence. Being prepared is simply the ultimate defense. It ensures that when critical financial information is needed the most, it stays protected, perfectly private, and instantly ready to use.

Passkeys vs. Passwords: Why It’s Time to Switch Now

February 26, 2026

We all do it. Every morning. You grab your coffee, sit down, and try to log into your bank. Or maybe your insurance portal. You type in a password. Maybe it’s a strong one. Maybe it’s… well, let’s be real. It’s probably the same one you use for Netflix. But here is the hard truth: relying on a secret code just doesn’t cut it anymore. Not when your entire financial life is sitting behind it. Fast forward to 2026, and there is finally a better option that people are actually using: the passkey.

If you are the one stuck managing the heavy stuff for your family – wills, health records, the “in case of emergency” file – knowing the difference between a passkey and a password isn’t just tech trivia. It is a survival skill. It’s about keeping the wolves at the door away from the things that actually matter.

This guide breaks down exactly what passkeys are, how they smash the old-school password system, and why making the switch is probably the smartest move you can make right now.

What Is a Password – And Why Is It No Longer Enough?

Think about it. A password is just a string of letters you made up. It’s a secret handshake between you and a computer. And for a long time? That was fine.

But here is the snag: humans are involved. And humans? We are messy. The stats are pretty rough – something like 70% of hacks start because of a weak or stolen login. We reuse passwords because we’re lazy. We pick easy ones because we’re forgetful. Or we get tricked by a fake email and hand them over on a silver platter.

Common password headaches include:

- Brute-force attacks: Hackers have computers that can guess billions of passwords a second. If yours is simple, it’s gone before you can blink.

- The Dark Web: If one random site you use gets breached, your password ends up for sale. Suddenly, the bad guys have the keys to your whole life.

- Phishing: It is terrifyingly easy to get fooled by a fake email or website that looks real. You type it in, and poof – they have it.

- Fatigue: You have dozens of accounts. Remembering unique codes for all of them? Impossible. So we reuse them. And that is dangerous.

- SMS flaws: Even those text message codes aren’t bulletproof. Hackers can swap SIM cards and steal those codes right out of the air.

There is a saying in the security world that haunts me: Hackers don’t break in – they log in. If they have your password, they are you.

What Is a Passkey – And How Does It Work?

Passkeys are a total rewrite of the rules. Forget typing. A passkey uses public-key cryptography. Imagine a digital key that is split in two. One half sits on the website. The other half stays locked inside your phone or laptop.

When you want to log in, your phone and the website have a quick, silent chat. You prove it’s you by just unlocking your screen – Face ID, fingerprint, whatever. You don’t type a single letter. Nothing gets sent over the internet for a hacker to steal.

Think of it like a puzzle. The website has a piece. Your phone has a piece. They only fit together when you – the real you – are holding the device.

Key facts about passkeys:

- They run on the FIDO2 standard. Basically, the big tech companies all agreed on a better way to do things.

- Everyone is jumping on board: Google, Apple, Amazon, Chase Bank. They all support it.

- Millions of people are already using them without even realizing it.

- You can’t phish them. You can’t guess them.

- If you have a smartphone from the last few years, you are already ready to go.

Passkeys vs. Passwords: A Side-by-Side Comparison

Why is everyone making such a big deal about this? You have to look at the differences side-by-side to really get it.

1. Security

- Passwords: Weak. They can be stolen, guessed, or fished out of you with a fake email.

- Passkeys: Rock solid. The private key never leaves your phone. Even if a hacker breaks into the bank’s server, they can’t steal your key because it isn’t there.

2. Ease of Use

- Passwords: A pain. You forget them. You reset them. You type them wrong.

- Passkeys: Easy. You look at your phone, or touch the sensor. Done. It works 98% of the time and it’s way faster.

3. Phishing Resistance

- Passwords: Terrible. If a fake site looks real, you’ll probably type your password in.

- Passkeys: Perfect. A passkey is tied to the real website. If you land on a fake site, your phone knows. It simply won’t let you log in.

4. Device Dependency and Flexibility

- Passwords: You can use them anywhere, but that’s also why they are risky.

- Passkeys: They live on your device. But don’t worry – Apple and Google sync them to the cloud. So your passkeys are on your phone, your tablet, and your laptop automatically.

5. Risk in a Data Breach

- Passwords: If a company gets hacked, your password is leaked.

- Passkeys: If a company gets hacked, the hackers get… nothing useful. They just get a public key that can’t unlock anything without your phone.

Why This Matters for Protecting Vital Life Records

We usually don’t think about this stuff until it’s too late. You get hacked, or a family member passes away and nobody can get into their accounts. That is a nightmare scenario.

The accounts that hold your life’s work – insurance, savings, wills – need better protection than “123456.” If these get breached, it’s not just annoying. It’s identity theft. It’s losing money.

The banks know this. That’s why Chase and Wells Fargo are pushing passkeys. They want you safe.

If you are using a digital vault to keep your family’s info organized, turning on passkeys is the single best thing you can do today.

How to Set Up a Passkey (It Is Simpler Than It Sounds)

You don’t need to be a tech wizard. It takes two minutes.

Step 1: Go to your account settings (Google, Amazon, whatever).

Step 2: Look for “Passkeys” or “Security.”

Step 3: Click “Create Passkey.” Your phone will ask for your face or fingerprint. Do it.

Step 4: You’re done. Next time, just click “Use Passkey.”

Step 5: If you want to be extra safe, use a password manager like 1Password to keep them all organized.

Expert Tip: Start with the big ones. Email. Bank. Insurance. Get those locked down first.

Should Passwords Be Abandoned Entirely?

Not yet. We’re in a transition phase. Lots of old websites still need passwords. So here is the game plan:

- Switch to passkeys for anything important.

- Use a password manager to generate crazy long passwords for the junk sites that don’t support passkeys yet.

- Stop using SMS codes if you can help it. Use an app instead.

- Get a hardware key (like a YubiKey) if you are really paranoid about your email security.

- Check back often. More sites are adding this every month.

Microsoft went passkey-first last year and it’s been huge. By the end of 2026, typing passwords will feel like using a flip phone.

What Happens If a Device Is Lost?

Everyone asks this. “If I lose my phone, am I locked out forever?”

No. You’re fine.

- Cloud Sync: If you use an iPhone, your keys are in iCloud. Get a new phone, sign in, and they are back. Same for Android.

- Backup: You can still use other ways to get into your account if you absolutely have to.

- Thieves can’t use them: Even if someone steals your phone, they don’t have your face or fingerprint. They can’t use your passkeys.

Passkeys and the Future of Secure Document Storage

For families storing wills and financial docs online, security is everything. A digital vault is pointless if the key is under the mat.

Passkeys fix the human error part. You can’t accidentally give away your passkey. It solves the biggest problem in security: us.

Experts at Gartner and big tech firms are calling this the biggest shift in security in decades. The password era is ending. Finally.

Key Takeaways

- Passwords are weak. They are too easy to steal or guess.

- Passkeys are strong. They use heavy-duty encryption and your own biometrics.

- It’s happening now. Major banks and tech giants are already using them.

- Mix it up. Use passkeys where you can, strong passwords where you must.

- Don’t worry about lost phones. Cloud sync has your back.

- Protect your legacy. If you store vital records, this is a must-have upgrade.

Conclusion: The Lock Is Getting an Upgrade

Switching to passkeys isn’t just about cool new tech. It’s about peace of mind. Passwords put all the pressure on you to be perfect. Passkeys let your device handle the security so you don’t have to.

If you are serious about keeping your family’s future safe, stop waiting. Passkeys are here. They work. And they are way better than what you’re using now.

The best time to switch was yesterday. The second best time is today.

Protect What Matters Most

InsureYouKnow.org provides a secure, encrypted electronic safe deposit box for life’s most important information – insurance policies, financial records, healthcare documents, and more. Storing vital records in one organized, protected location means families are never left searching when they need information most. Start protecting what matters today at InsureYouKnow.org.