2026 Student Loan Defaults: Secure Your Financial Records

March 6, 2026

A massive financial wall hit millions of Americans earlier this year. Pandemic payment pauses are officially ancient history. The temporary relief programs dried up entirely. After months of messy court battles regarding income-driven repayment plans, the federal government decided to bring back its heaviest collection tools. Starting in early 2026, the U.S. Department of Education began sending administrative wage garnishment letters to defaulted borrowers. The numbers from major credit bureaus, like Experian, look pretty grim. The entire country is watching a massive wave of loan delinquencies happen in real time. People are suddenly staring down severe financial penalties. Getting through this economic squeeze requires a lot more than just reading news updates. It demands immediate, highly organized access to specific financial paperwork.

The 2026 Student Loan Landscape: A Shocking New Data Trend

So, who is actually defaulting right now? Historically, student loan defaults mostly hammered sub-prime borrowers. That whole narrative flipped completely upside down in 2026. Recent reports from credit bureaus reveal something entirely unexpected. Nearly a quarter of newly defaulted borrowers belong in the “prime” credit tier or even higher. These are the exact demographics the financial industry usually views as incredibly stable.

With over 5 million borrowers currently sitting in default status, and millions more falling behind every month, the economic pain is obvious. Borrowers are stuck navigating a bizarre maze of constantly changing payment plans. Making things worse, millions of accounts got bounced around between different private servicing companies over the last two years. Monthly payments got lost in the mail. Crucial paperwork simply vanished. Hold times to speak with basic customer service stretched into hours. Once a federal student loan reaches 270 days past due, it hits official default status. At that specific moment, the government gets to use an administrative superpower that regular credit card companies cannot even touch. They can literally take wages without ever stepping foot inside a courtroom.

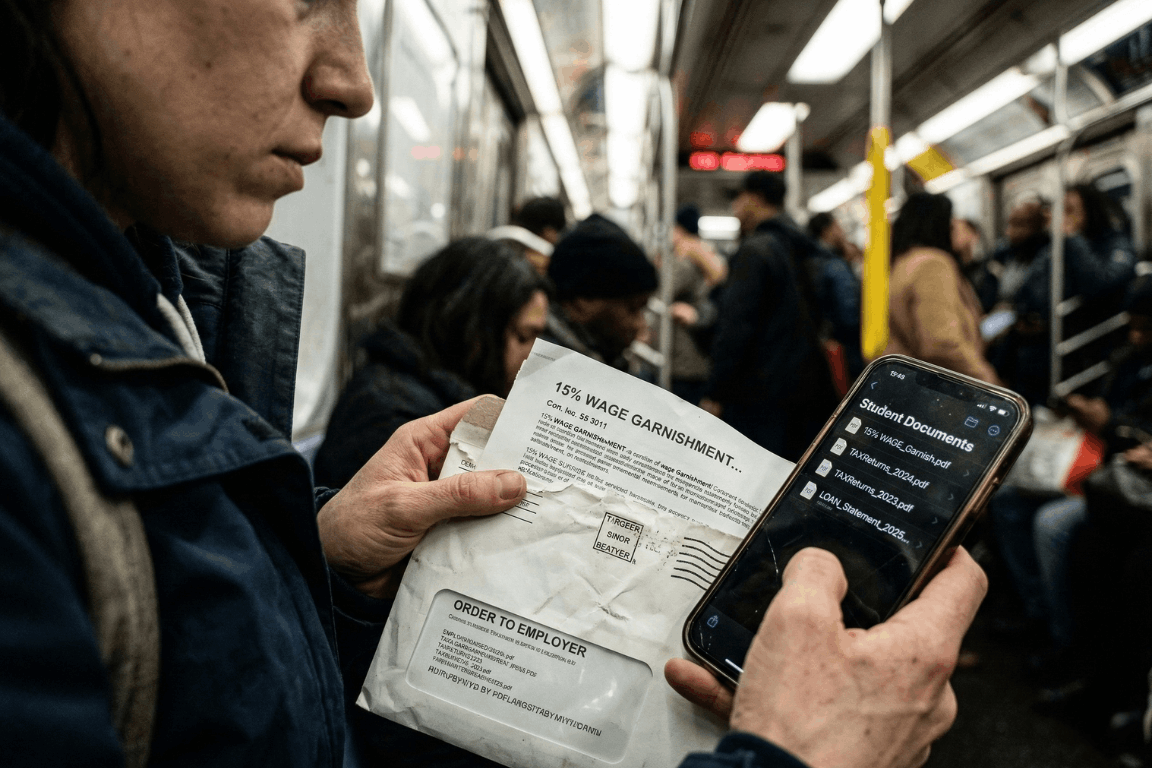

Understanding Administrative Wage Garnishment: The 15% Reality

The fallout from a federal default happens fast. Through a process called Administrative Wage Garnishment (AWG), the Department of Education can legally force an employer to pull up to 15% of a borrower’s disposable pay. Disposable pay simply means the cash remaining after legally required deductions, like federal and state taxes, come out of the check.

Federal law does leave a very small safety net in place. Borrowers get to keep a weekly take-home amount equal to at least 30 times the federal minimum wage. But for anyone living from one paycheck to the next, suddenly losing 15% of their income is pure disaster. It usually means missing the rent, skipping the grocery store, or defaulting on other credit cards. Before the garnishment actually kicks in, the government must send a 30-day advance written warning. That specific 30-day window is basically everything. It acts as the only real timeframe a borrower gets to object or set up a different payment plan before their paycheck actually shrinks.

How to Stop Garnishment: The Heavy Burden of Proof

Borrowers holding a garnishment notice still carry some legal rights. During those 30 days, individuals can officially demand a hearing to stop the withholding order. They might attempt to prove extreme financial hardship. Or, they could try applying for federal loan rehabilitation. Rehabilitation usually involves agreeing to make nine on-time payments over a 10-month window to get the loan back on track.

Another route involves submitting a formal financial hardship appeal. Winning this appeal means legally proving that a 15% pay cut makes buying basic survival items impossible. The government looks at documented living expenses and compares them against very strict IRS Allowable Living Expense guidelines. If a family spends more on food or housing than the IRS thinks is necessary for that specific family size, the extra amount gets totally ignored. Proving hardship is notoriously difficult. Using these rights is never a walk in the park. It requires gathering highly specific legal and financial records immediately. In these types of administrative hearings, the burden of proof lands squarely on the borrower.

The Critical Role of Organized Financial Documents

Sloppy paperwork turns a bad money situation into an absolute nightmare. When the garnishment letter shows up, the clock ticks fast. Spending hours digging through cluttered email inboxes for old messages from loan servicers wastes valuable time. Tearing up the living room looking for utility bills to prove basic living expenses just fuels the anxiety. If a borrower fails to hand over the correct evidence within 30 days, their employer receives the order. The garnishment starts.

This explains exactly why relying on a secure, independent electronic safe deposit box changes the playing field. Keeping a dedicated digital vault for vital life information ensures nobody gets blindsided by aggressive debt collectors. Storing all important financial, legal, and contractual documents in one simple location gives borrowers a huge advantage. They can instantly grab the exact proof they need to protect their paychecks and negotiate with default resolution teams.

Essential Documents to Secure in a Digital Vault

To build a strong defense against a default warning, individuals should make sure the following documents are digitized, safely uploaded, and ready for action:

- Original Loan Agreements and Master Promissory Notes: Finding original contracts immediately helps verify the true debt amount. It also spots accounting errors and confirms which company actually owns the loan today.

- Complete Tax Returns: Proving financial hardship or enrolling in an income-driven repayment plan means submitting paperwork. The Department of Education demands recent federal and state tax returns before they even start talking.

- Official Pay Stubs: Current pay stubs are absolutely required to figure out actual disposable income. They also help verify that any proposed wage garnishment does not illegally drop below the minimum wage protection limit.

- Household Expense Records: Tracking basic living costs is a strict requirement for hardship appeals. Think about rent agreements, mortgage papers, utility bills, health insurance premiums, and pharmacy receipts. These papers help prove that living expenses are reasonable and fit within tight IRS standards.

- Correspondence with Loan Servicers: A strong paper trail of older payments, approved forbearances, and emails with the loan servicers can literally save the day. This proof is extremely important if someone needs to show a loan was wrongfully thrown into default in the first place.

The Absolute Security of Zero-Knowledge Storage

Privacy is absolutely non-negotiable when dealing with highly sensitive financial details. Relying on physical metal filing cabinets leaves people wide open to lost papers, house fires, or basic theft. Depending on regular, unencrypted email folders or a messy computer desktop basically hands sensitive financial data directly to hackers. Cybercriminals routinely target email servers specifically to find W-2 forms and tax returns. Once they grab those files, identity theft is pretty much guaranteed.

Using a specialized platform built with heavy-duty cloud encryption makes sure financial data stays completely private. The absolute best platforms run on Amazon cloud encryption mixed with a “zero-knowledge” setup. In a zero-knowledge system, only the actual account owner knows the password. The site administrators never get to see it. That means absolutely nobody else can ever gain access, view the files, or mine the stored documents to sell the data.

Strategic Document Sharing with Trusted Partners

Fixing a defaulted student loan is almost never a solo job. Borrowers usually need to bring in certified financial planners, tax accountants, or specialized student loan lawyers to help decode the messy federal rules.

Advanced secure portals allow individuals to selectively share specific document folders with these exact trusted partners. Sending unencrypted PDFs of tax returns and pay stubs back and forth through regular email is a massive cybersecurity hazard. Instead, account holders can simply give a legal advisor temporary, secure access to the required files right inside the encrypted vault. This targeted sharing feature speeds up the whole default resolution process, keeps communication secure, and leaves the rest of the vault totally locked down. Setting up automatic monthly reminders inside the portal also helps users routinely update their financial snapshots, keeping their defense strategy completely fresh.

Facing economic uncertainty requires a solid game plan. The return of federal student loan wage garnishments in 2026 creates a massive hurdle. Credit bureau data clearly shows that financial distress is hitting borrowers across every single demographic right now. Surviving this wave of defaults demands aggressive, proactive money management and flawless record-keeping. Centralizing vital financial documents into a secure, encrypted digital safe deposit box lets individuals tackle economic chaos with total confidence. Being prepared is simply the ultimate defense. It ensures that when critical financial information is needed the most, it stays protected, perfectly private, and instantly ready to use.